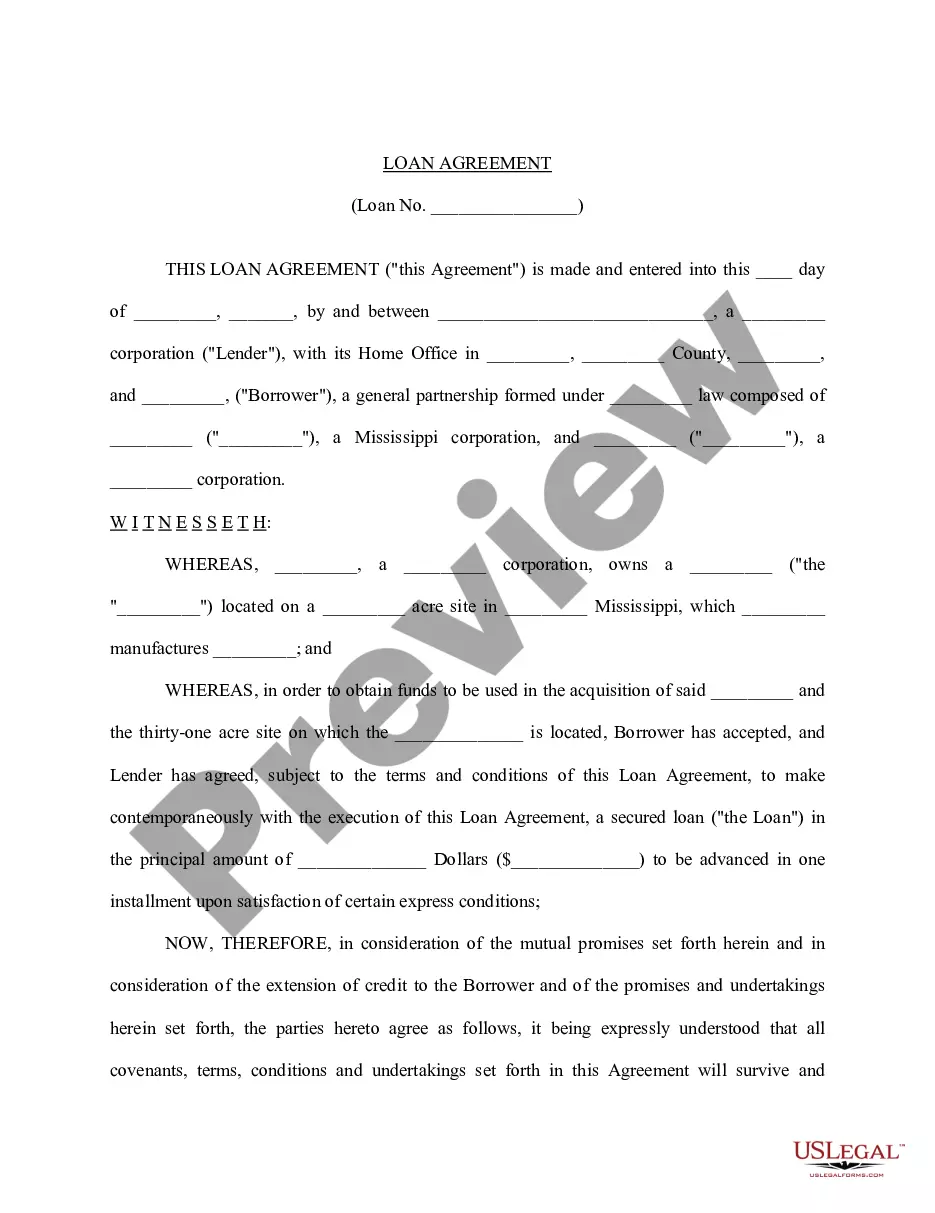

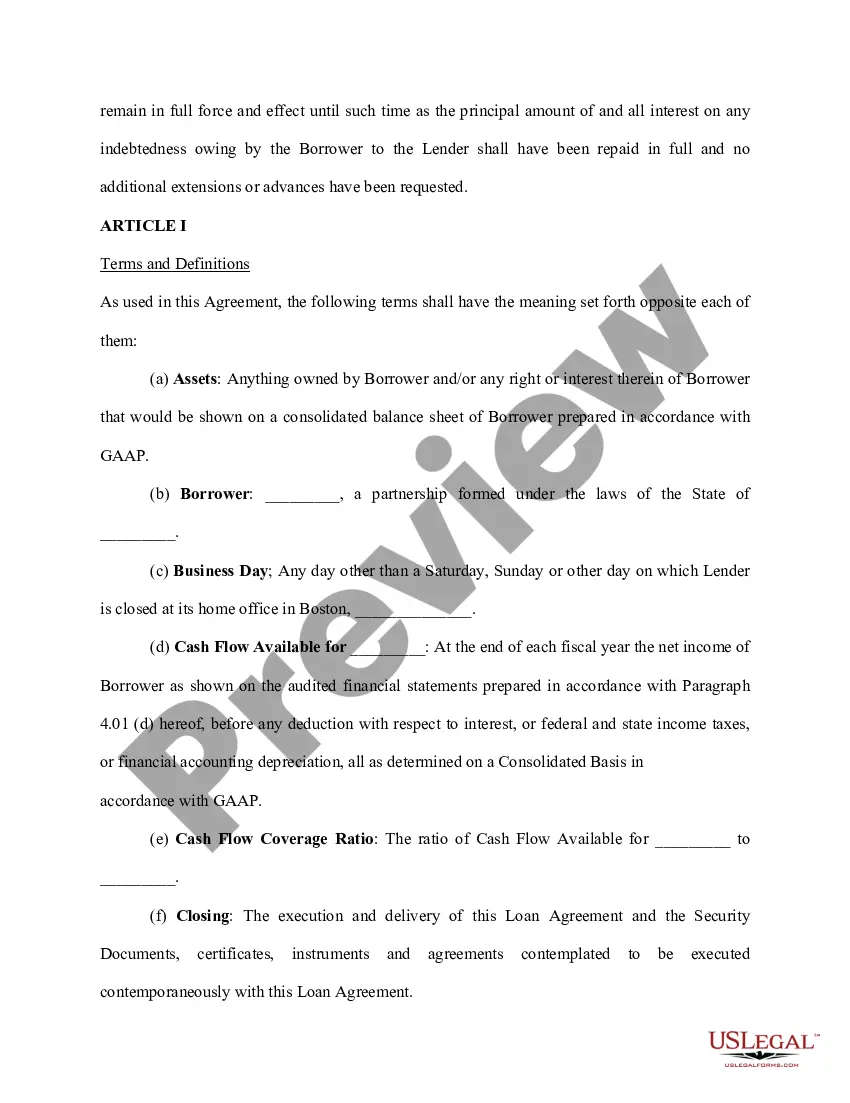

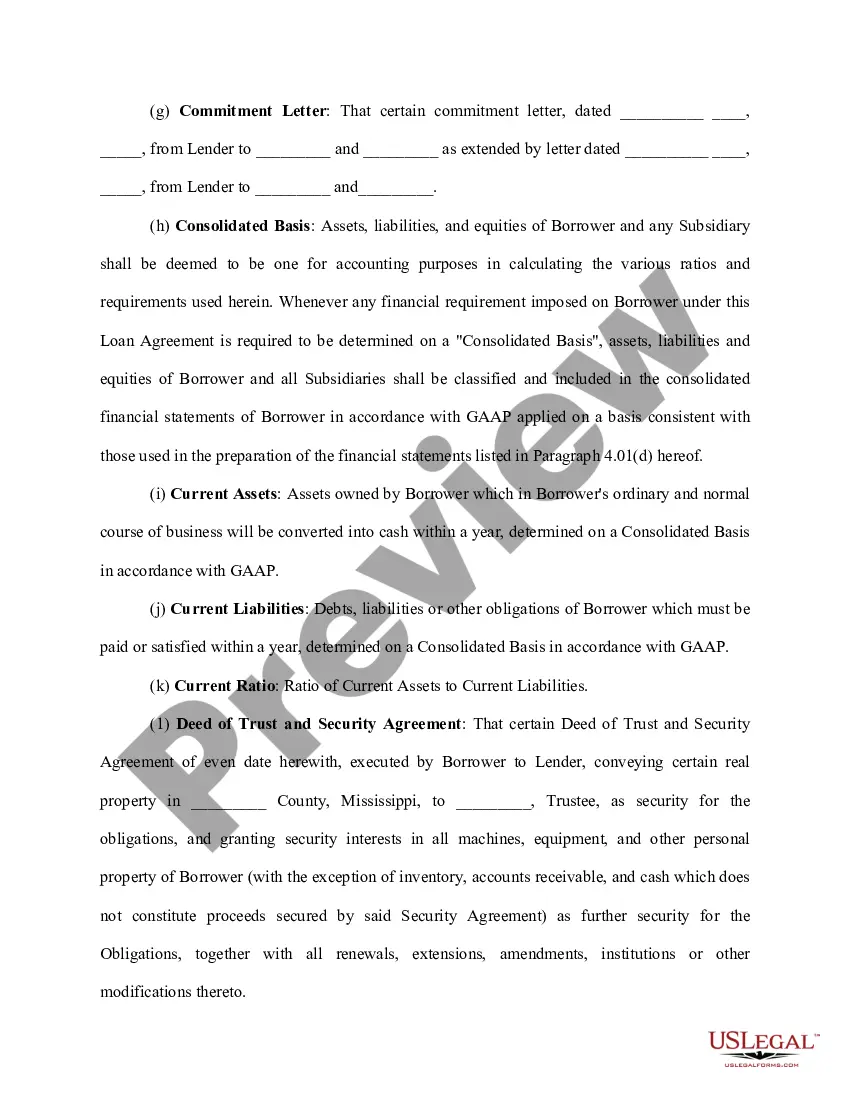

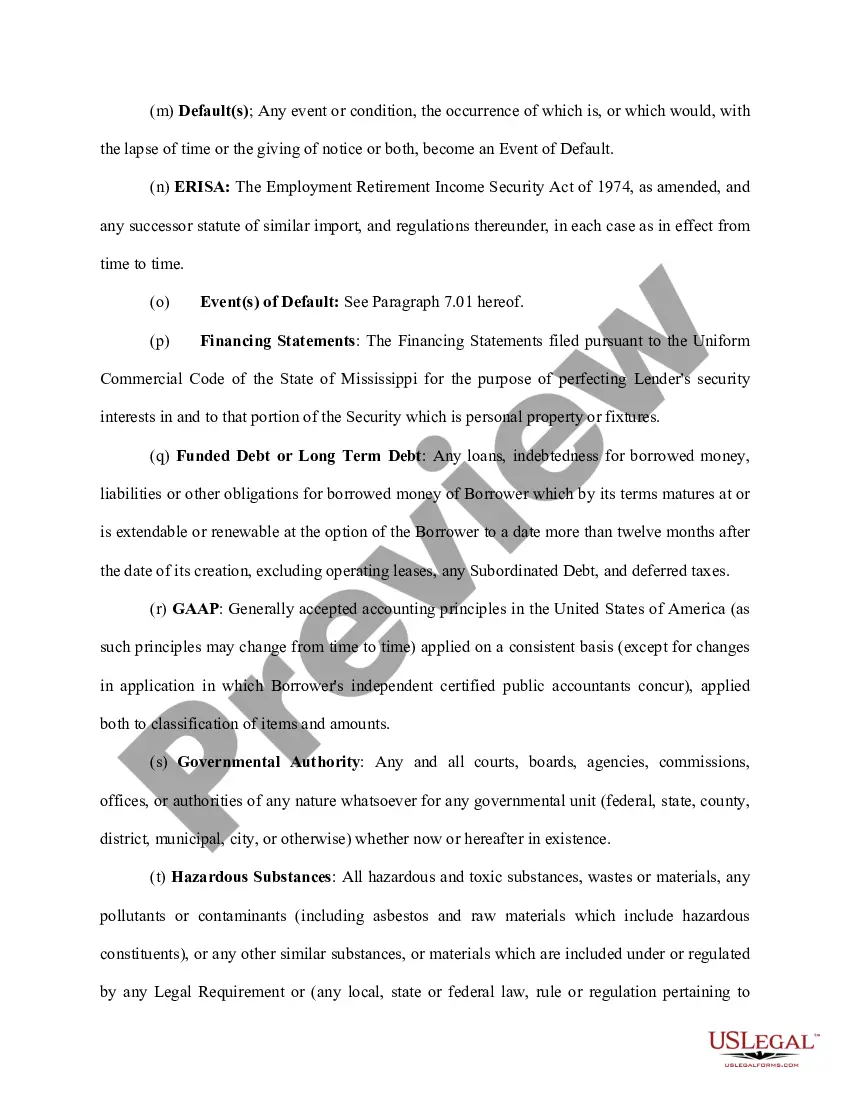

A Montana Loan Agreement for Family Member is a legally binding contract that outlines the terms and conditions under which a family member loans money to another family member in the state of Montana. This agreement ensures clarity and protects both parties involved in the loan transaction. A typical Montana Loan Agreement for Family Member includes the following key elements: 1. Parties involved: The names and contact information of both the lender (family member providing the loan) and borrower (family member receiving the loan) are clearly stated in the agreement. 2. Loan amount: The agreement specifies the exact amount of money being loaned to the borrower by the lender. 3. Terms of repayment: The agreement outlines how the loan will be repaid, such as a lump-sum payment or monthly installments. It also mentions the interest rate, if any, that will be charged on the loan. 4. Payment schedule: The agreement states the frequency and due dates for loan repayments, ensuring both parties are aware of when payments are expected. 5. Late payment penalties: If applicable, the agreement may outline the consequences of late or missed payments, including penalty fees. 6. Duration of the loan: The agreement states the length of time the borrower has to repay the loan, whether it is a short-term loan or a long-term loan. 7. Collateral and security: If the loan is secured by any assets or property, such as a vehicle or property, the agreement should specify the details of the collateral. 8. Signatures: Both parties sign the agreement, indicating their understanding and acceptance of the terms and conditions. Different types of Montana Loan Agreements for Family Members may include: 1. Personal loan agreement: This type of loan agreement is used when a family member lends money to another family member for personal use, such as covering medical expenses, education costs, or home renovations. 2. Business loan agreement: If a family member loans money to another family member for business purposes, a business loan agreement is used. This agreement outlines how the loan will be used for business activities and may include additional provisions related to the business. 3. Real estate loan agreement: When a family member provides a loan for the purchase, renovation, or improvement of real estate, a real estate loan agreement is used. This agreement typically includes details about the property, mortgage terms, and repayment schedule. It is important to note that Montana Loan Agreements for Family Members should be carefully drafted and reviewed by legal professionals to ensure compliance with state laws and to protect the interests of both parties involved.

Montana Loan Agreement for Family Member

Description

How to fill out Montana Loan Agreement For Family Member?

Discovering the right lawful document template can be quite a struggle. Naturally, there are plenty of templates accessible on the Internet, but how will you discover the lawful type you will need? Make use of the US Legal Forms web site. The assistance gives a huge number of templates, such as the Montana Loan Agreement for Family Member, that can be used for organization and private needs. All the kinds are checked out by pros and meet up with state and federal specifications.

Should you be presently signed up, log in to the accounts and click on the Obtain option to obtain the Montana Loan Agreement for Family Member. Utilize your accounts to check through the lawful kinds you have purchased previously. Go to the My Forms tab of the accounts and acquire yet another version from the document you will need.

Should you be a whole new consumer of US Legal Forms, listed below are straightforward instructions that you should stick to:

- Initial, make certain you have chosen the proper type for your personal metropolis/region. It is possible to look over the shape while using Preview option and browse the shape outline to make certain it is the right one for you.

- In case the type will not meet up with your preferences, take advantage of the Seach industry to find the correct type.

- Once you are certain that the shape is proper, click the Purchase now option to obtain the type.

- Opt for the prices strategy you would like and enter in the required info. Build your accounts and purchase an order with your PayPal accounts or charge card.

- Select the data file file format and down load the lawful document template to the device.

- Full, change and print out and indication the obtained Montana Loan Agreement for Family Member.

US Legal Forms is definitely the biggest library of lawful kinds in which you can discover different document templates. Make use of the service to down load skillfully-made files that stick to state specifications.