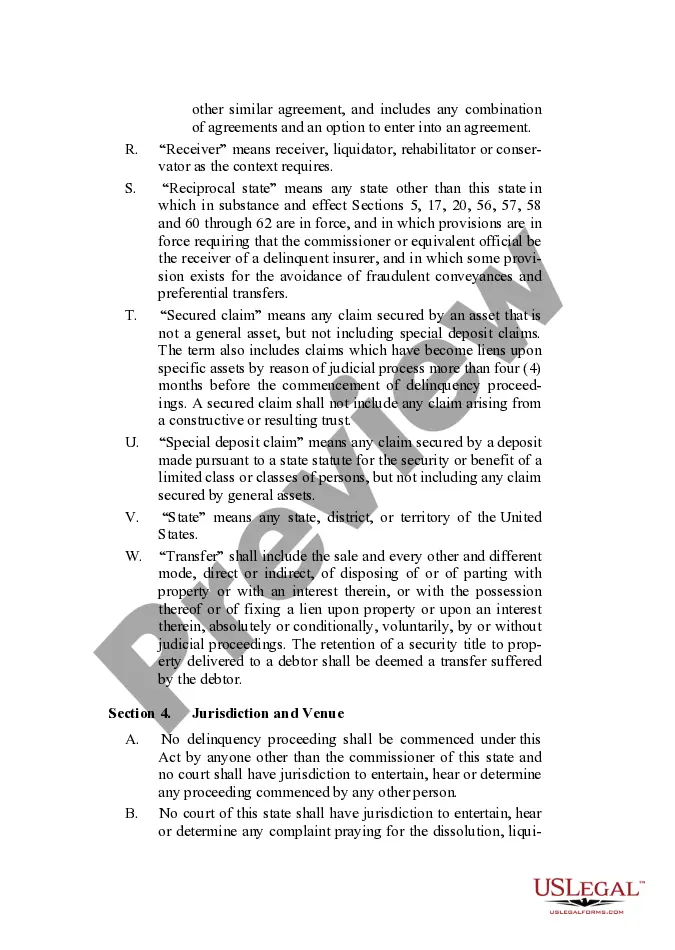

Full text and statutory guidelines for the Insurers Rehabilitation and Liquidation Model Act.

The Montana Insurers Rehabilitation and Liquidation Model Act (MIRA) is a comprehensive legislation formulated to regulate and govern the rehabilitation and liquidation processes of insurance companies in the state of Montana. MIRA provides a structured framework for the prompt and equitable resolution of insolvent insurance companies, with an aim to safeguard policyholders, claimants, and other stakeholders. Under MIRA, there are different types of proceedings defined to address specific scenarios: 1. Rehabilitation: This type of proceeding is initiated when an insurance company is deemed financially impaired but has a reasonable chance of returning to solvency. Rehabilitation involves the implementation of various measures to help the insurer overcome financial difficulties and restore its financial health. The authority responsible for rehabilitation may take control of the company's operations, restructure its management, and formulate a plan to restore solvency while ensuring policyholder protection. 2. Liquidation: When an insolvent insurer cannot be rehabilitated or its rehabilitation attempts have failed, a liquidation proceeding is initiated. Liquidation involves the orderly winding down of the insurance company's operations with the ultimate objective of distributing its assets to various claimants, including policyholders, creditors, employees, and other parties entitled to recover funds from the insurer. This proceeding ensures that the liquidation process is conducted fairly and efficiently while minimizing any potential adverse impact on policyholders and claimants. 3. Ancillary Receivership: Ancillary receivership occurs when an insurer, operating in another state, becomes insolvent and possesses assets or conducts business in Montana. In such situations, the Montana Insurance Commissioner may be designated as an ancillary receiver, working in conjunction with the primary receiver (typically in the state of domicile). The ancillary receiver ensures that Montana-based assets and interests are adequately protected and that the liquidation process adheres to Montana law. MIRA prescribes detailed procedures, requirements, and standards concerning notice of proceedings, reporting obligations, claim filing, asset distribution, reinsurance agreements, and judicial oversight. It promotes transparency, accountability, and protection of policyholders' interests throughout the rehabilitation and liquidation processes. Montana is one of the many states in the United States that has adopted its own version of the Insurers Rehabilitation and Liquidation Model Act. The act may have variations in different states, but the underlying purpose remains consistent: to ensure the efficient and equitable resolution of insolvent insurance companies while prioritizing policyholder protection.The Montana Insurers Rehabilitation and Liquidation Model Act (MIRA) is a comprehensive legislation formulated to regulate and govern the rehabilitation and liquidation processes of insurance companies in the state of Montana. MIRA provides a structured framework for the prompt and equitable resolution of insolvent insurance companies, with an aim to safeguard policyholders, claimants, and other stakeholders. Under MIRA, there are different types of proceedings defined to address specific scenarios: 1. Rehabilitation: This type of proceeding is initiated when an insurance company is deemed financially impaired but has a reasonable chance of returning to solvency. Rehabilitation involves the implementation of various measures to help the insurer overcome financial difficulties and restore its financial health. The authority responsible for rehabilitation may take control of the company's operations, restructure its management, and formulate a plan to restore solvency while ensuring policyholder protection. 2. Liquidation: When an insolvent insurer cannot be rehabilitated or its rehabilitation attempts have failed, a liquidation proceeding is initiated. Liquidation involves the orderly winding down of the insurance company's operations with the ultimate objective of distributing its assets to various claimants, including policyholders, creditors, employees, and other parties entitled to recover funds from the insurer. This proceeding ensures that the liquidation process is conducted fairly and efficiently while minimizing any potential adverse impact on policyholders and claimants. 3. Ancillary Receivership: Ancillary receivership occurs when an insurer, operating in another state, becomes insolvent and possesses assets or conducts business in Montana. In such situations, the Montana Insurance Commissioner may be designated as an ancillary receiver, working in conjunction with the primary receiver (typically in the state of domicile). The ancillary receiver ensures that Montana-based assets and interests are adequately protected and that the liquidation process adheres to Montana law. MIRA prescribes detailed procedures, requirements, and standards concerning notice of proceedings, reporting obligations, claim filing, asset distribution, reinsurance agreements, and judicial oversight. It promotes transparency, accountability, and protection of policyholders' interests throughout the rehabilitation and liquidation processes. Montana is one of the many states in the United States that has adopted its own version of the Insurers Rehabilitation and Liquidation Model Act. The act may have variations in different states, but the underlying purpose remains consistent: to ensure the efficient and equitable resolution of insolvent insurance companies while prioritizing policyholder protection.