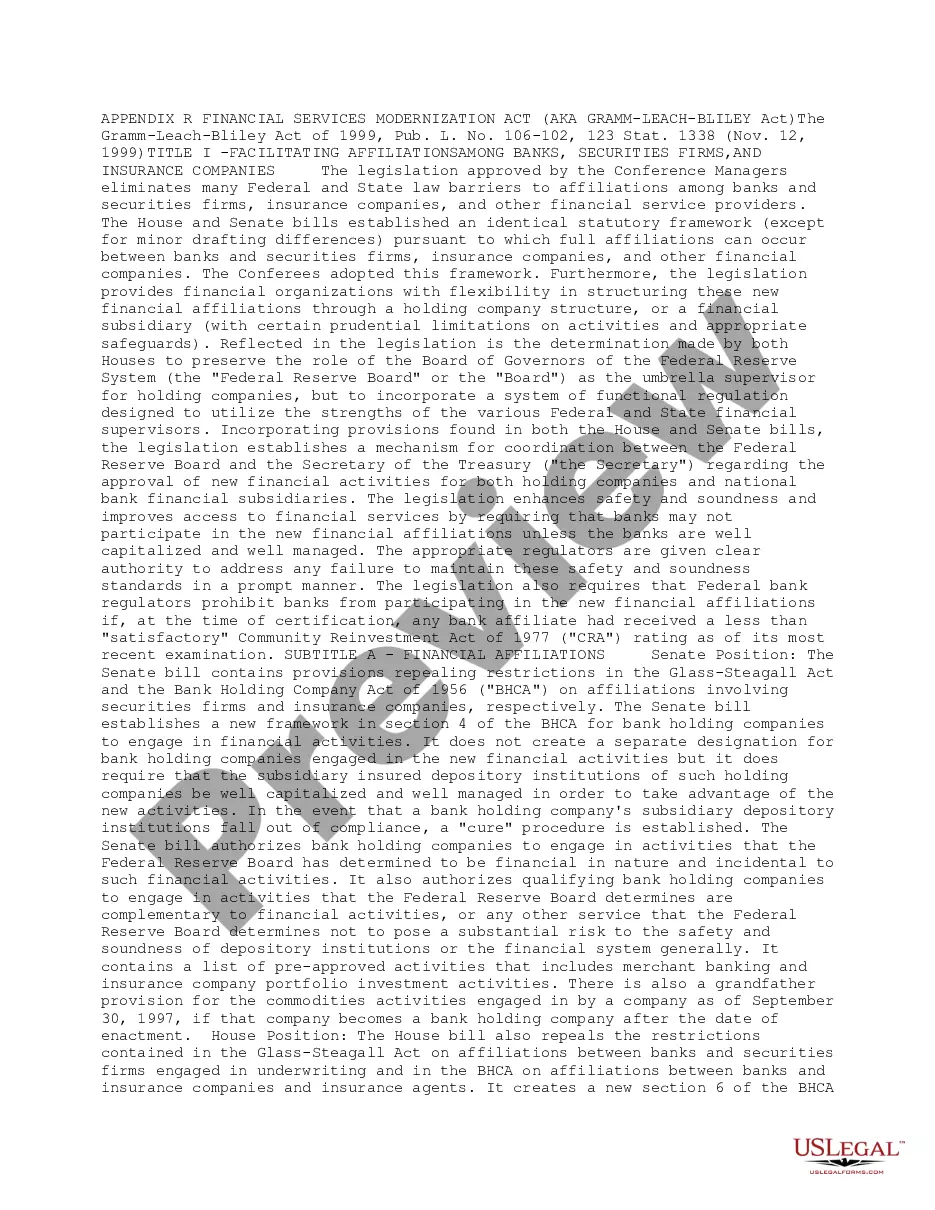

Full text and statutory guidelines for the Financial Services Modernization Act (Gramm-Leach-Bliley Act)

The Montana Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant piece of legislation that had a significant impact on the financial industry in the United States. Enacted in 1999, the ALBA aimed to modernize and streamline financial services while also addressing the potential risks to consumer privacy and the economy. Under the ALBA, several key provisions were set forth to protect consumer data and enhance the competitiveness of financial institutions. One of the primary objectives was to break down the barriers between different types of financial entities, allowing for consolidation and integration of services across the industry. The ALBA established three major types of financial services companies: 1. Banks: The act allowed commercial banks to merge with investment banks and securities firms, enabling a more comprehensive range of financial services under one roof. This integration of services aimed to promote competition and foster innovation in the financial sector. 2. Insurance companies: The ALBA permitted the affiliation of insurance providers with banks or investment firms, promoting diversification within the industry. This consolidation allowed for the offering of combined banking and insurance products to customers. 3. Securities firms: The act also facilitated the integration of securities firms with banks, encouraging the provision of investment services by traditional banking institutions. This change resulted in the formation of financial conglomerates offering a wide array of financial products, such as loans, insurance, and investment services. The ALBA also provided provisions to safeguard consumer privacy and protect sensitive financial information. Financial institutions were required to provide clear and transparent disclosure of their privacy policies and practices to customers. Additionally, customers were given the right to opt-out of the sharing of their personal information with non-affiliated third parties, thereby allowing them to maintain control over their data. The act established the Financial Privacy Rule and the Safeguards Rule to ensure the protection of customer information. The Financial Privacy Rule requires financial institutions to inform customers of their privacy policies and provide opt-out options. On the other hand, the Safeguards Rule mandates the implementation of security measures to protect customer data from unauthorized access. In summary, the Montana Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act, revolutionized the financial services landscape by allowing consolidation and integration of banking, insurance, and securities firms. It aimed to enhance competition, promote innovation, and protect consumer privacy. Through its various provisions, the Act sought to strike a balance between modernizing the financial industry and ensuring the security and privacy of customer data.The Montana Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act (ALBA), is a significant piece of legislation that had a significant impact on the financial industry in the United States. Enacted in 1999, the ALBA aimed to modernize and streamline financial services while also addressing the potential risks to consumer privacy and the economy. Under the ALBA, several key provisions were set forth to protect consumer data and enhance the competitiveness of financial institutions. One of the primary objectives was to break down the barriers between different types of financial entities, allowing for consolidation and integration of services across the industry. The ALBA established three major types of financial services companies: 1. Banks: The act allowed commercial banks to merge with investment banks and securities firms, enabling a more comprehensive range of financial services under one roof. This integration of services aimed to promote competition and foster innovation in the financial sector. 2. Insurance companies: The ALBA permitted the affiliation of insurance providers with banks or investment firms, promoting diversification within the industry. This consolidation allowed for the offering of combined banking and insurance products to customers. 3. Securities firms: The act also facilitated the integration of securities firms with banks, encouraging the provision of investment services by traditional banking institutions. This change resulted in the formation of financial conglomerates offering a wide array of financial products, such as loans, insurance, and investment services. The ALBA also provided provisions to safeguard consumer privacy and protect sensitive financial information. Financial institutions were required to provide clear and transparent disclosure of their privacy policies and practices to customers. Additionally, customers were given the right to opt-out of the sharing of their personal information with non-affiliated third parties, thereby allowing them to maintain control over their data. The act established the Financial Privacy Rule and the Safeguards Rule to ensure the protection of customer information. The Financial Privacy Rule requires financial institutions to inform customers of their privacy policies and provide opt-out options. On the other hand, the Safeguards Rule mandates the implementation of security measures to protect customer data from unauthorized access. In summary, the Montana Financial Services Modernization Act, also known as the Gramm-Leach-Bliley Act, revolutionized the financial services landscape by allowing consolidation and integration of banking, insurance, and securities firms. It aimed to enhance competition, promote innovation, and protect consumer privacy. Through its various provisions, the Act sought to strike a balance between modernizing the financial industry and ensuring the security and privacy of customer data.