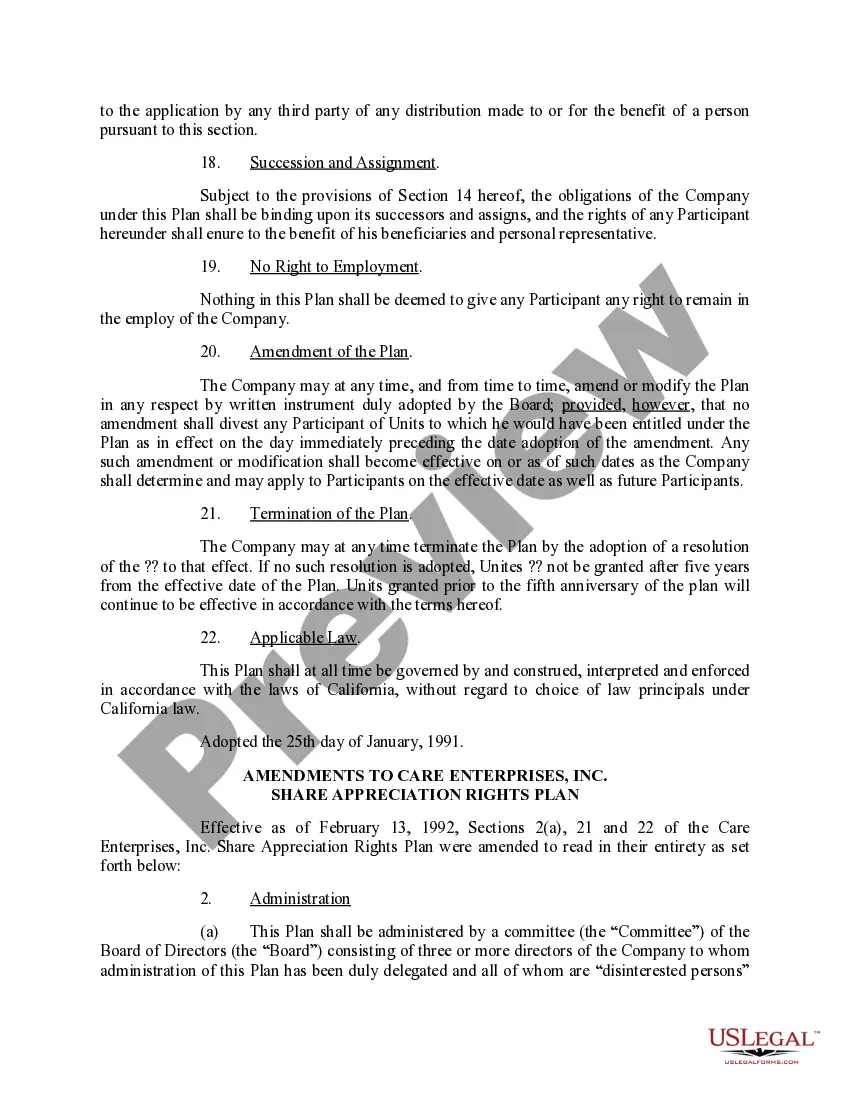

Montana Share Appreciation Rights Plan, also known as Montana SARS Plan, is a type of equity-based compensation plan designed to provide financial incentives to employees or executives of a company. This plan is usually implemented as an amendment to an existing employee stock option plan or long-term incentive plan. Under the Montana SARS Plan, employees are granted the right to receive cash or stock value appreciation of a specific number of company shares over a predetermined period. These grants are typically awarded to incentivize and retain key employees by linking their compensation directly to the company's performance. One of the variations of the Montana SARS Plan is the Performance-Based SARS. This type of plan ties the SARS' grant and payout to specific performance goals or metrics, such as the company's financial targets, revenue growth, or stock price appreciation. Performance-based SARS provide a powerful tool to align employee interests with the company's objectives while rewarding exceptional performance. Another type is the Restricted Stock Appreciation Rights (SARS) Plan. This plan grants SARS that are contingent on certain conditions or time-based vesting schedules. SARS typically have a longer vesting period, ensuring the employees' continued commitment and service to the company over the long term. Once fully vested, employees can exercise their SARS and receive the appreciation in stock value. The Montana SARS Plan with amendment may also include features such as performance periods, exercise periods, eligibility criteria, and payment terms. These features vary depending on the company's goals, industry, and structure. Additionally, the plan may specify how the SARS' value will be calculated, whether it is based on the difference between the stock price at the grant date and the exercise date or another predetermined formula. It is important to note that the Montana SARS Plan with amendment must comply with relevant securities laws, tax regulations, and accounting standards. Therefore, it is advisable for companies to consult legal, tax, and financial professionals when designing and implementing such plans to ensure compliance and optimize the benefits for both the company and its employees.

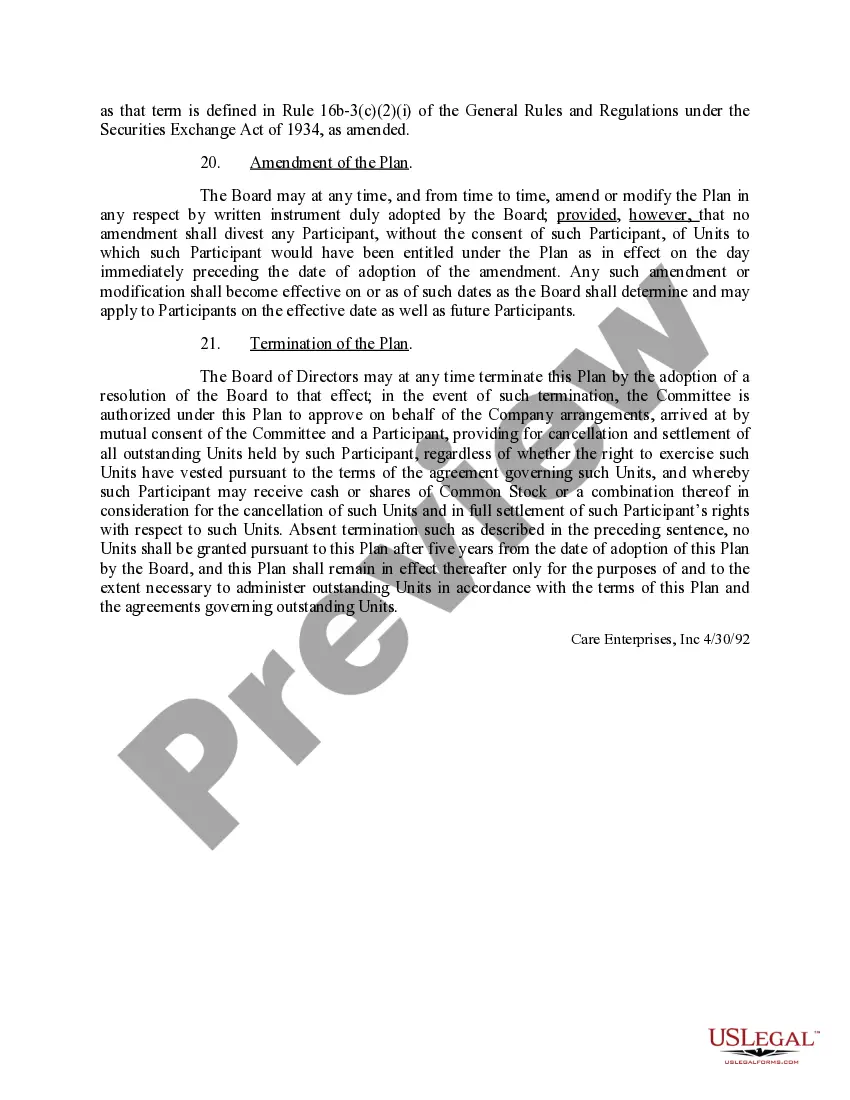

Montana Share Appreciation Rights Plan, also known as Montana SARS Plan, is a type of equity-based compensation plan designed to provide financial incentives to employees or executives of a company. This plan is usually implemented as an amendment to an existing employee stock option plan or long-term incentive plan. Under the Montana SARS Plan, employees are granted the right to receive cash or stock value appreciation of a specific number of company shares over a predetermined period. These grants are typically awarded to incentivize and retain key employees by linking their compensation directly to the company's performance. One of the variations of the Montana SARS Plan is the Performance-Based SARS. This type of plan ties the SARS' grant and payout to specific performance goals or metrics, such as the company's financial targets, revenue growth, or stock price appreciation. Performance-based SARS provide a powerful tool to align employee interests with the company's objectives while rewarding exceptional performance. Another type is the Restricted Stock Appreciation Rights (SARS) Plan. This plan grants SARS that are contingent on certain conditions or time-based vesting schedules. SARS typically have a longer vesting period, ensuring the employees' continued commitment and service to the company over the long term. Once fully vested, employees can exercise their SARS and receive the appreciation in stock value. The Montana SARS Plan with amendment may also include features such as performance periods, exercise periods, eligibility criteria, and payment terms. These features vary depending on the company's goals, industry, and structure. Additionally, the plan may specify how the SARS' value will be calculated, whether it is based on the difference between the stock price at the grant date and the exercise date or another predetermined formula. It is important to note that the Montana SARS Plan with amendment must comply with relevant securities laws, tax regulations, and accounting standards. Therefore, it is advisable for companies to consult legal, tax, and financial professionals when designing and implementing such plans to ensure compliance and optimize the benefits for both the company and its employees.