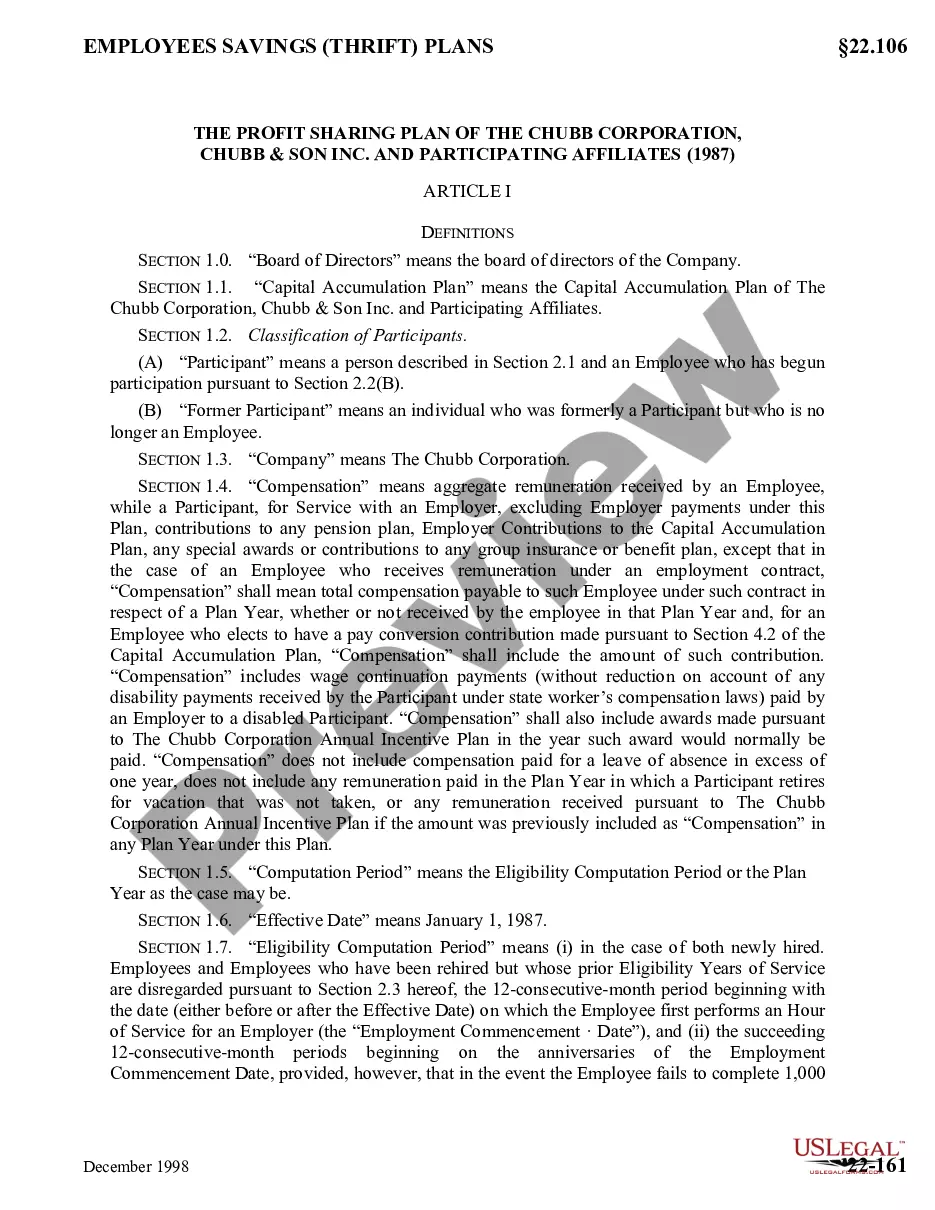

22-118E 22-118E . . . Employee Savings Thrift Plan under which three types of contributions can be made: (a) those permitted under a qualified Cash Or Deferred Arrangement ("CODA") under Section 401(k) of Internal Revenue Code, (b) those made by participating companies matching 40% of CODA contributions, and (c) additional voluntary employee contributions made by participants who elect maximum CODA contribution and wish to save additional amounts out of after-tax dollars

Montana Employees Savings Thrift Plan

Category:

State:

Multi-State

Control #:

US-CC-22-118E

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Employees Savings Thrift Plan?

US Legal Forms - among the biggest libraries of legitimate forms in the USA - offers a wide range of legitimate papers layouts you are able to download or print out. Using the website, you can find 1000s of forms for business and specific reasons, categorized by classes, claims, or key phrases.You will discover the newest variations of forms just like the Montana Employees Savings Thrift Plan within minutes.

If you already have a registration, log in and download Montana Employees Savings Thrift Plan from the US Legal Forms collection. The Download key will appear on every kind you perspective. You have access to all previously downloaded forms inside the My Forms tab of your respective bank account.

If you wish to use US Legal Forms initially, here are easy directions to help you started out:

- Be sure you have chosen the proper kind for the area/region. Select the Review key to analyze the form`s content. Look at the kind description to actually have selected the appropriate kind.

- When the kind does not suit your needs, utilize the Lookup industry at the top of the display screen to find the one who does.

- In case you are satisfied with the shape, confirm your option by clicking on the Get now key. Then, opt for the pricing plan you like and provide your references to register on an bank account.

- Method the financial transaction. Make use of your credit card or PayPal bank account to complete the financial transaction.

- Find the structure and download the shape on your own device.

- Make adjustments. Complete, modify and print out and indicator the downloaded Montana Employees Savings Thrift Plan.

Each template you added to your account does not have an expiry particular date and it is the one you have for a long time. So, if you would like download or print out an additional duplicate, just proceed to the My Forms section and click around the kind you will need.

Gain access to the Montana Employees Savings Thrift Plan with US Legal Forms, by far the most considerable collection of legitimate papers layouts. Use 1000s of skilled and condition-certain layouts that meet your business or specific requirements and needs.

Form popularity

FAQ

Best Funds for TSP Performance in 2023 So far in 2023, the C Fund is up 16.88%, the S Fund is up 12.64%, and the I Fund is up 12.16%. Over the last 12 months, the C Fund is up 19.54%, the I Fund is up 19.08%, and the S Fund is up 15.24%.

Your best bet is to stick with the C, S and I Funds. Here's the ratio we recommend for your portfolio: 80% in the C Fund, which is tied to the performance of the S&P 500. 10% in the S Fund, which includes stocks from small- to mid-sized companies that offer high risk and high return.

Regular employee contributions Each pay period, your agency or service will deduct your contributions, also known as deferrals, from your basic salary in the amount or percentage that you chose when you started contributing or were automatically enrolled.

TSP Contributions If you are covered by FERS, you may also receive matching agency contributions. All eligible employees are automatically enrolled in TSP at a five percent contribution rate.

What is the safest TSP fund? The G fund is generally the safest option as it invests in government securities. Although you won't lose money investing in this fund, your rate of return will be low.

During the setup process, you'll create a username, password, and ThriftLine PIN to access your account. You'll follow step-by-step prompts to verify your identity, update your contact information, and set up your account security. My Account setup should take 5 to 10 minutes for most TSP participants.

Regular TSP To make equal contributions over the course of the 2024 calendar year (for 26 pay periods), you should contribute $885 each pay period. You should enter your election of $885 into myPay during December 3 ? 9, 2023, and your election should be effective on December 17, 2023, the first pay period for 2024.

These rules of thumb say you should have saved ... 2 to 3 times your income by age 40. 3 to 4 times your income by age 45.