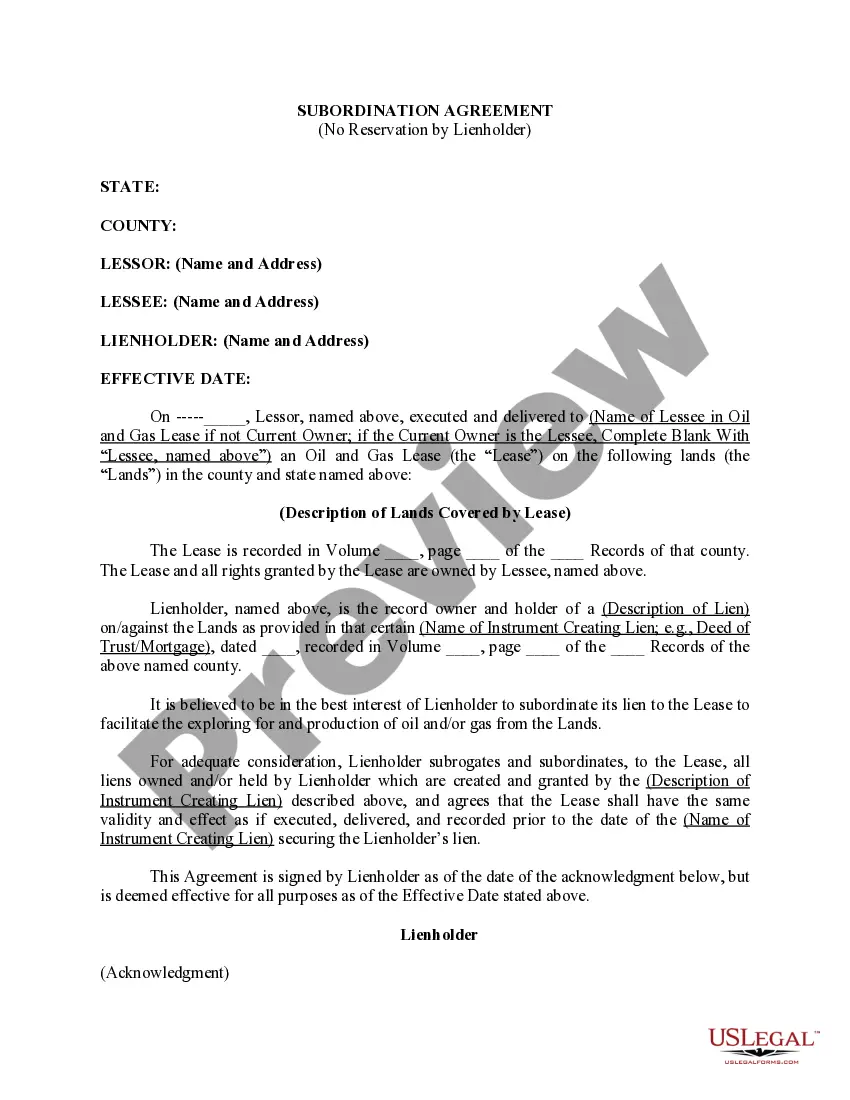

Montana Subordination Agreement with no Reservation by Lien holder: A Comprehensive Guide Introduction: In the state of Montana, a Subordination Agreement with no Reservation by Lien holder is a legally binding document that allows a lien holder to agree to subordinate their lien position in favor of another creditor, without reserving any rights or claims. This agreement is often used in real estate transactions when one party wants to obtain a new loan or refinancing that requires a first lien position. By subordinating their lien, the original lien holder agrees to let the new lender take priority over their claim in case of default or foreclosure. This detailed description will provide key insights into the different types of Montana Subordination Agreement with no Reservation by Lien holder, serving as a useful resource for lenders, borrowers, and legal professionals. 1. General Features: — A Montana Subordination Agreement with no Reservation by Lien holder is a voluntary agreement between a lien holder and a new lender. Th lienen holderer agrees to subordinate their lien position to the new lender, relinquishing their right to be paid before the new lender in case of default or foreclosure. — This agreement is typically used when the borrower wants to refinance their existing loan or secure additional financing. — It is essential for all parties involved to fully understand the terms and consequences of the subordination agreement before signing. 2. Types of Montana Subordination Agreement with no Reservation by Lien holder: While there are no specific subtypes of this agreement in Montana, it is crucial to consider the context in which the subordination takes place. Here are some common scenarios where this agreement is employed: a) Real Estate Transactions: In real estate deals, a Montana Subordination Agreement with no Reservation by Lien holder might be used when a borrower wants to obtain a new loan secured by the property. The original lien holder, often a mortgage lender, agrees to subordinate their lien to the new lender, effectively giving the new lender priority over the property in case of default or foreclosure. b) Business Loan Refinancing: In business financing, a company might seek refinancing with a different lender while having existing liens on its assets. The existing lender(s) can choose to sign a Montana Subordination Agreement with no Reservation by Lien holder to allow the new lender to take priority over their liens. c) Personal Loan Consolidation: For individuals with multiple outstanding loans, securing a consolidation loan can simplify debt management. In such cases, liens from the original lenders can be subordinated through a Montana Subordination Agreement with no Reservation by Lien holder, enabling the new lender to have a superior lien position. Conclusion: A Montana Subordination Agreement with no Reservation by Lien holder plays a significant role in various financial transactions, particularly in real estate and lending contexts. Whether it pertains to real estate transactions, business loan refinancing, or personal loan consolidation, understanding the implications and intricacies of this agreement is essential for all parties involved. It is strongly advised to consult with legal professionals before executing any subordination agreements to ensure compliance with Montana laws and protect the respective interests of all parties.

Montana Subordination Agreement with no Reservation by Lienholder

Description

How to fill out Montana Subordination Agreement With No Reservation By Lienholder?

US Legal Forms - one of many most significant libraries of lawful varieties in America - gives a wide array of lawful file layouts you are able to download or print. While using web site, you may get a huge number of varieties for organization and personal functions, categorized by types, says, or keywords.You can get the newest types of varieties like the Montana Subordination Agreement with no Reservation by Lienholder within minutes.

If you have a subscription, log in and download Montana Subordination Agreement with no Reservation by Lienholder in the US Legal Forms catalogue. The Down load button can look on every kind you view. You have accessibility to all in the past delivered electronically varieties within the My Forms tab of your own bank account.

If you wish to use US Legal Forms the first time, allow me to share simple guidelines to get you began:

- Be sure you have chosen the proper kind to your town/state. Click on the Review button to review the form`s articles. Browse the kind information to actually have selected the right kind.

- In case the kind does not fit your demands, make use of the Research area towards the top of the display screen to obtain the one which does.

- If you are pleased with the form, confirm your selection by clicking on the Acquire now button. Then, opt for the pricing strategy you prefer and provide your qualifications to register to have an bank account.

- Process the deal. Use your credit card or PayPal bank account to accomplish the deal.

- Choose the structure and download the form on the system.

- Make alterations. Complete, modify and print and indicator the delivered electronically Montana Subordination Agreement with no Reservation by Lienholder.

Each template you added to your account does not have an expiration date which is your own forever. So, if you would like download or print an additional version, just check out the My Forms portion and then click around the kind you will need.

Get access to the Montana Subordination Agreement with no Reservation by Lienholder with US Legal Forms, by far the most extensive catalogue of lawful file layouts. Use a huge number of professional and express-certain layouts that fulfill your organization or personal demands and demands.