Montana Clauses Relating to Preferred Returns

Description

How to fill out Clauses Relating To Preferred Returns?

Are you in a place where you will need paperwork for possibly enterprise or specific uses virtually every working day? There are plenty of lawful file templates available on the net, but finding types you can depend on isn`t straightforward. US Legal Forms provides a huge number of kind templates, just like the Montana Clauses Relating to Preferred Returns, which can be published in order to meet state and federal requirements.

In case you are presently informed about US Legal Forms web site and also have your account, merely log in. After that, you are able to down load the Montana Clauses Relating to Preferred Returns web template.

If you do not have an account and need to start using US Legal Forms, follow these steps:

- Find the kind you want and make sure it is for the right city/region.

- Use the Preview button to check the shape.

- Browse the description to ensure that you have chosen the appropriate kind.

- When the kind isn`t what you`re looking for, make use of the Research discipline to discover the kind that suits you and requirements.

- If you discover the right kind, simply click Acquire now.

- Opt for the prices program you need, complete the necessary information and facts to generate your money, and purchase your order using your PayPal or charge card.

- Select a practical document structure and down load your version.

Get each of the file templates you may have bought in the My Forms food selection. You can get a further version of Montana Clauses Relating to Preferred Returns at any time, if needed. Just select the required kind to down load or produce the file web template.

Use US Legal Forms, probably the most extensive assortment of lawful forms, in order to save time and stay away from faults. The services provides professionally produced lawful file templates that you can use for a selection of uses. Produce your account on US Legal Forms and start creating your daily life a little easier.

Form popularity

FAQ

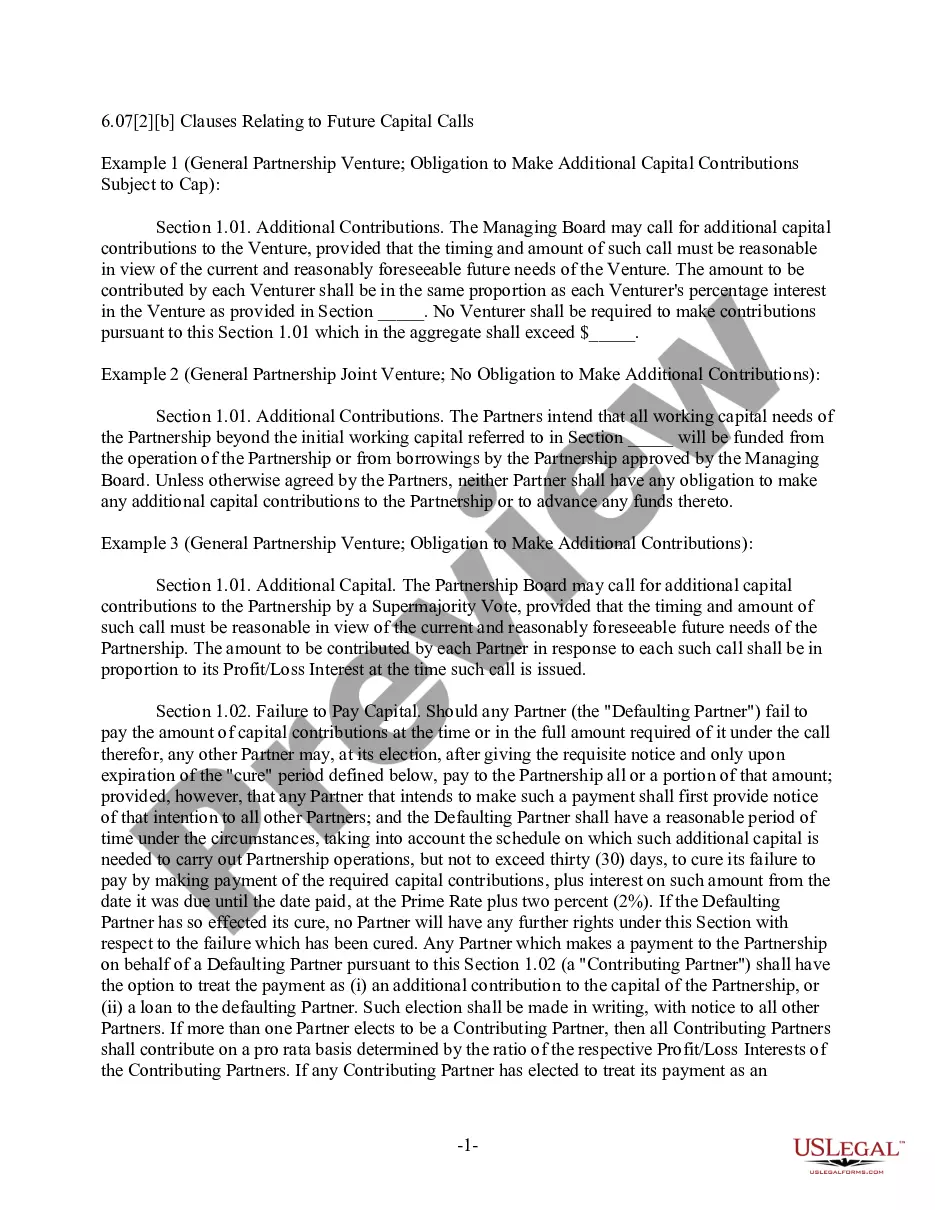

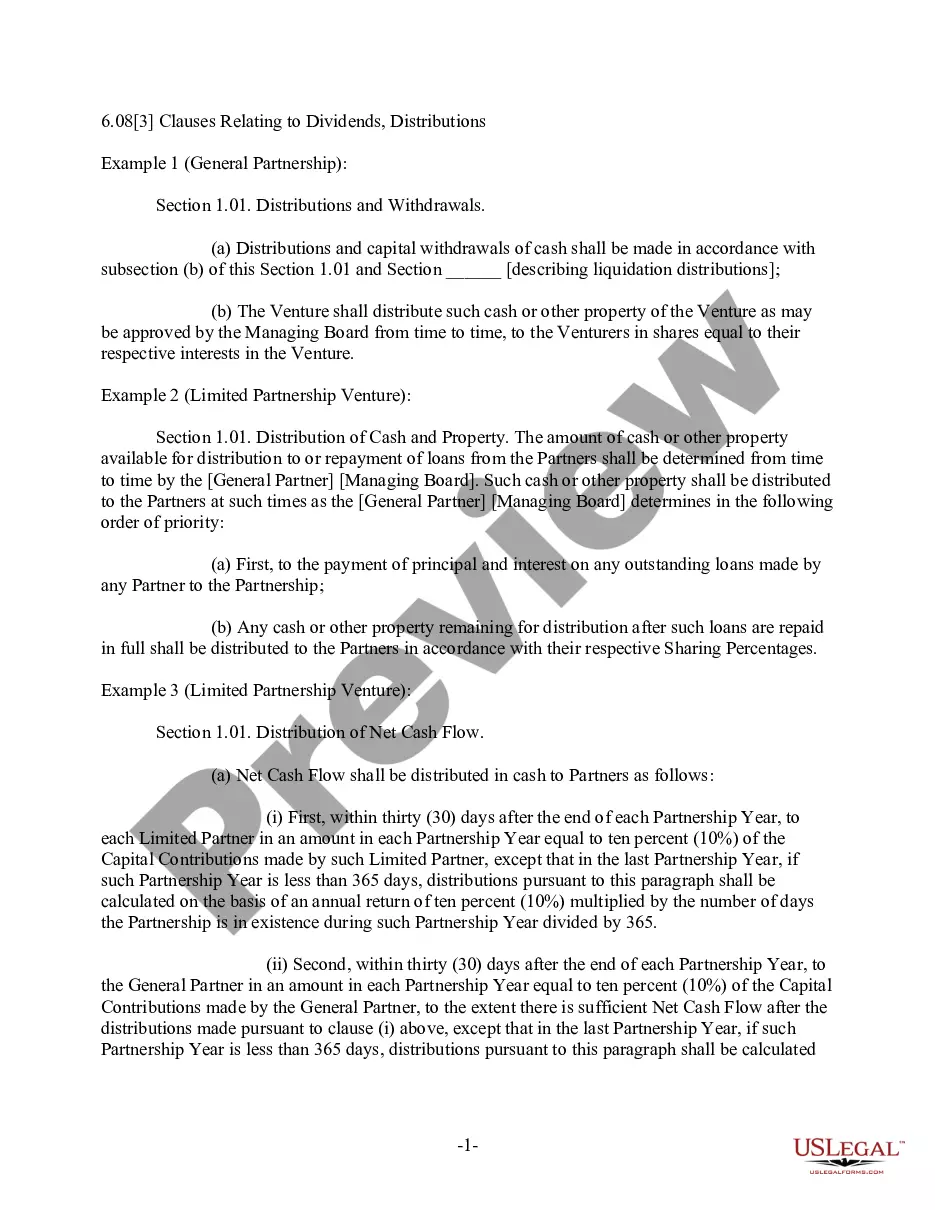

Economic accruals of preferred return are guaranteed payments as of the time of accrual. treated as distributive share rather than a guaranteed payment with any excess of accrued preferred return over gross income in the year of accrual treated as a guaranteed payment in the year of the accrual.

A preferred return is a profit distribution preference whereby profits, either from operations, sale, or refinance, are distributed to one class of equity before another until a certain rate of return on the initial investment is reached.

While a preferred return is an obligation to pay out a certain percentage of a real estate investment's initial return without fees, a guaranteed payment is what a partner collects for managing the property and investors' funds.

Preferred returns for an entire syndication can be calculated by multiplying the equity from the investor class by the preferred rate. For example, if $1 million is raised from investors to purchase a property, and the preferred rate is 6%, the annual preferred return would be $60,000.

What is a preferred return? A preferred return is a profit distribution preference whereby profits, either from operations, sale, or refinance, are distributed to one class of equity before another until a certain rate of return on the initial investment is reached.

A preferred return in real estate is a percentage of return of profits that an investor must receive before the investment management team can receive a profit. A typically preferred return in a real estate investment is generally between 6% and 9%, depending on the investment's risk.

Most preferred returns are cumulative, but non-compounding.

A preferred return in private real estate investing is the minimum return an investor must receive before an investment manager can earn a performance fee. The preferred return is typically between 6% to 9% in real estate investing, depending on the risk of the investment.