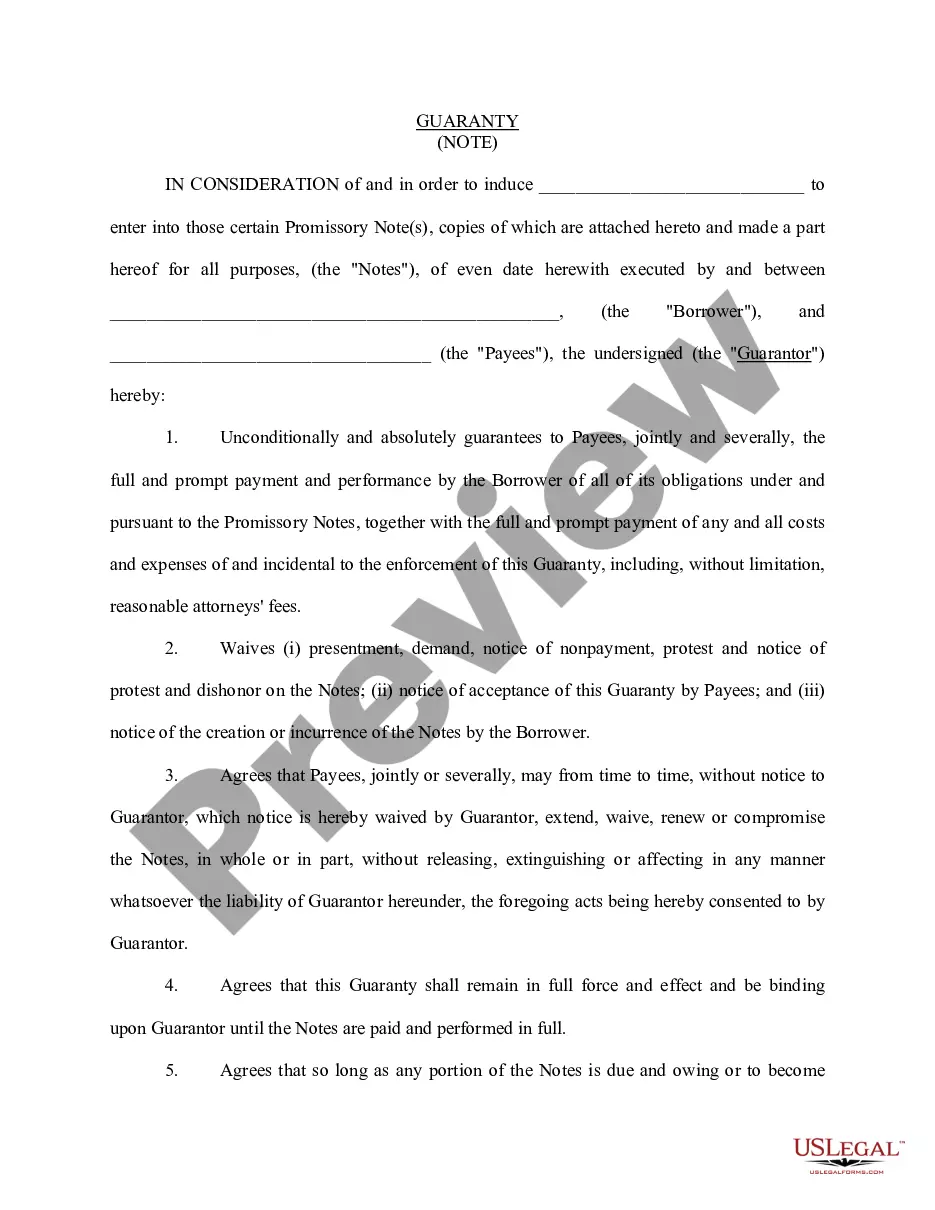

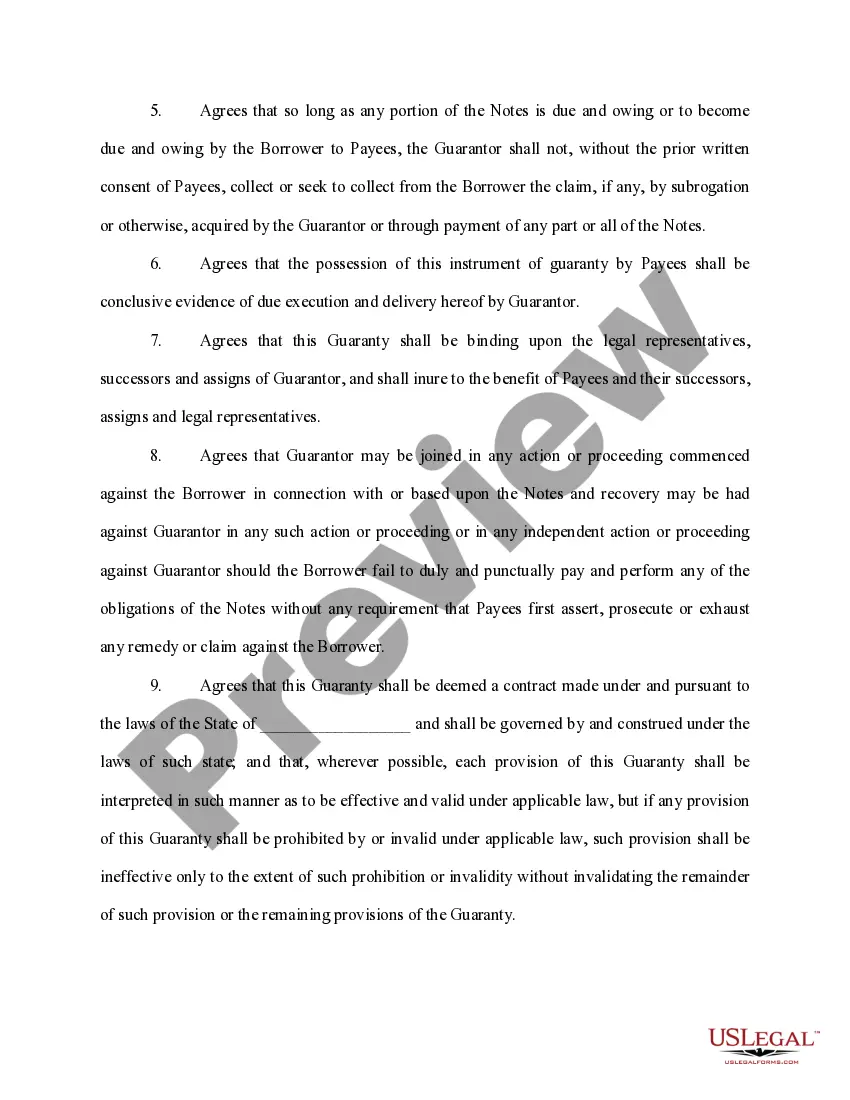

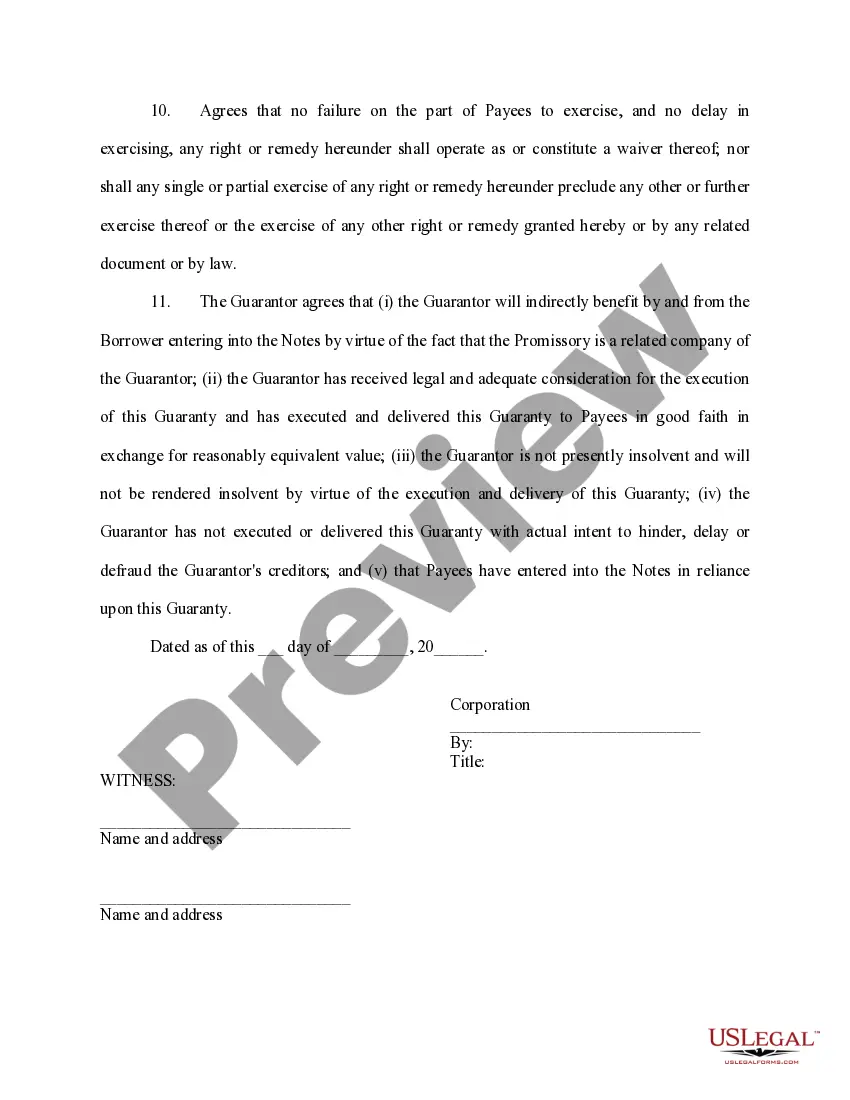

The North Carolina Guaranty of Promissory Note by Corporation — Individual Borrower is a legally binding document that serves as a guarantee by a corporation for the repayment of a promissory note obtained by an individual borrower. This agreement acts as a form of security for the lender, ensuring that the borrower's obligations will be fulfilled even if they default on the loan. In this context, the term "guaranty" refers to an agreement made by a third party, which in this case is the corporation, to assume responsibility for the debt incurred by the borrower. The individual borrower remains primarily liable for the repayment of the promissory note, but in the event of default or non-payment, the corporation steps in to fulfill the obligations according to the terms of this guaranty. The guaranty document outlines various important components, including: 1. Parties involved: It identifies the corporation, individual borrower, and the lender involved in the loan agreement. All entities must be clearly stated, with their legal names. 2. Obligations of the borrower: The guaranty details the terms of the promissory note, including the loan amount, interest rate, repayment schedule, late payment penalties, and any other relevant conditions that the borrower must comply with. 3. Guarantor's obligations: The document clearly states the corporation's agreement to guarantee the repayment of the promissory note. It may cover the primary debt as well as any future modifications or extensions of the loan agreement. The guarantor is obligated to pay for any outstanding principal, interest, fees, or costs associated with the loan. 4. Waivers and consents: The parties involved may waive certain rights, such as the right to a jury trial in case of a dispute arising from this guaranty. Additionally, the guaranty may require individual borrower consent for the corporation's involvement in guaranteeing the promissory note. 5. Event of default and remedies: The guaranty outlines specific events that would be considered as default, such as late payments, breach of terms, or bankruptcy. It also establishes the lender's rights and remedies to seek payment from both the individual borrower and the corporation in case of default. 6. Governing law: The document specifies that the agreement is governed by the laws of the state of North Carolina, ensuring compliance with local regulations. Different types or variations of the North Carolina Guaranty of Promissory Note by Corporation — Individual Borrower may exist depending on the specific requirements of the lender or borrower. These variations could include additional clauses related to lateralization, personal guarantees by individuals within the corporation, or specific limitations on the corporation's liability. It is essential to consult with legal professionals experienced in North Carolina corporate and lending laws to ensure the accuracy and adequacy of the Guaranty of Promissory Note by Corporation — Individual Borrower for a particular situation.

North Carolina Guaranty of Promissory Note by Corporation - Individual Borrower

Description

How to fill out North Carolina Guaranty Of Promissory Note By Corporation - Individual Borrower?

It is possible to devote time on-line looking for the legitimate file format that meets the federal and state requirements you require. US Legal Forms offers a large number of legitimate forms which are evaluated by professionals. You can actually download or print out the North Carolina Guaranty of Promissory Note by Corporation - Individual Borrower from our assistance.

If you currently have a US Legal Forms profile, you may log in and click the Obtain button. After that, you may complete, modify, print out, or sign the North Carolina Guaranty of Promissory Note by Corporation - Individual Borrower. Each and every legitimate file format you get is your own property forever. To obtain yet another version for any acquired form, proceed to the My Forms tab and click the corresponding button.

If you use the US Legal Forms site the very first time, follow the easy guidelines beneath:

- First, be sure that you have chosen the best file format for the state/metropolis that you pick. Browse the form description to make sure you have chosen the correct form. If readily available, take advantage of the Review button to look throughout the file format at the same time.

- If you wish to find yet another version of your form, take advantage of the Search industry to find the format that meets your requirements and requirements.

- When you have found the format you want, simply click Acquire now to continue.

- Find the prices prepare you want, type your accreditations, and register for an account on US Legal Forms.

- Complete the transaction. You can use your charge card or PayPal profile to purchase the legitimate form.

- Find the structure of your file and download it to the gadget.

- Make adjustments to the file if required. It is possible to complete, modify and sign and print out North Carolina Guaranty of Promissory Note by Corporation - Individual Borrower.

Obtain and print out a large number of file web templates using the US Legal Forms site, that offers the most important variety of legitimate forms. Use expert and state-particular web templates to take on your small business or specific requires.