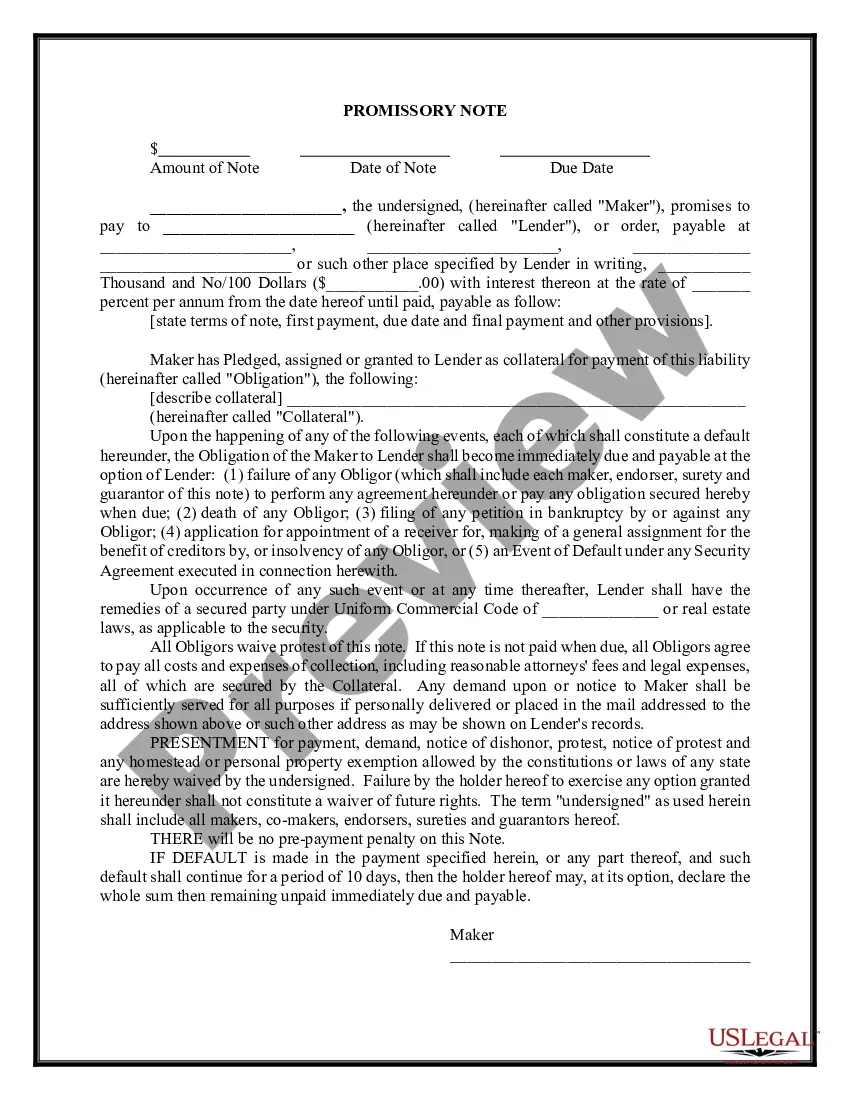

A secured promissory note is a legal document used in North Carolina as a means of borrowing money, where the borrower agrees to repay the lender the borrowed amount, including any interest, in regular installments over a specified period. The primary characteristic of a secured promissory note is that the borrower pledges collateral, such as real estate, personal property, or other valuable assets, to protect the lender's interests in case of default. The North Carolina Secured Promissory Note includes essential details, such as the names and addresses of the parties involved (lender and borrower), the principal amount borrowed, the interest rate, the repayment terms (including the number and frequency of payments), and any late payment fees or penalties. Additionally, it specifies the collateral provided by the borrower and the rights and remedies of the lender in case of default. North Carolina recognizes various types of secured promissory notes, including: 1. Real Estate Secured Promissory Note: This type of note involves using real estate as collateral to secure the loan. The borrower pledges a property they own or are purchasing as security for the debt. 2. Vehicle Secured Promissory Note: In this case, a vehicle, such as a car or motorcycle, is pledged as collateral for the loan. The borrower agrees that if they fail to repay the loan as agreed, the lender can take possession of the vehicle to recover their investment. 3. Personal Property Secured Promissory Note: This type of note involves using personal property, such as jewelry, electronics, or valuable assets, as collateral to secure the loan. The borrower agrees to surrender the pledged property in the event of non-payment. 4. Business Secured Promissory Note: This note is utilized when a business borrows money, and its assets or accounts receivable are pledged as collateral. It provides the lender with a means of recourse if the business fails to meet its repayment obligations. North Carolina requires the secured promissory note to be properly executed and notarized to be legally binding. It is recommended that both parties seek legal advice to ensure compliance with all applicable laws and regulations. Remember, the information provided here is for informational purposes only and should not be considered legal advice. It is always advisable to consult an attorney familiar with North Carolina laws and regulations before entering any legal agreement.

North Carolina Secured Promissory Note

Description

How to fill out North Carolina Secured Promissory Note?

US Legal Forms - among the greatest libraries of authorized types in the States - offers a wide range of authorized document web templates you are able to download or print out. Making use of the web site, you may get a huge number of types for company and person functions, sorted by classes, suggests, or keywords and phrases.You can find the latest versions of types just like the North Carolina Secured Promissory Note in seconds.

If you currently have a monthly subscription, log in and download North Carolina Secured Promissory Note through the US Legal Forms local library. The Download key will appear on every single type you see. You gain access to all earlier saved types inside the My Forms tab of your respective bank account.

If you would like use US Legal Forms initially, here are easy recommendations to help you started out:

- Ensure you have picked out the proper type for the town/area. Select the Preview key to examine the form`s information. Look at the type outline to actually have chosen the right type.

- When the type doesn`t satisfy your specifications, utilize the Look for industry at the top of the monitor to obtain the the one that does.

- In case you are content with the shape, affirm your selection by clicking on the Purchase now key. Then, pick the pricing strategy you favor and offer your credentials to sign up to have an bank account.

- Method the financial transaction. Make use of credit card or PayPal bank account to perform the financial transaction.

- Pick the format and download the shape on the gadget.

- Make modifications. Complete, modify and print out and sign the saved North Carolina Secured Promissory Note.

Every single web template you put into your bank account lacks an expiry day which is the one you have for a long time. So, in order to download or print out an additional duplicate, just proceed to the My Forms segment and click in the type you require.

Obtain access to the North Carolina Secured Promissory Note with US Legal Forms, by far the most considerable local library of authorized document web templates. Use a huge number of professional and express-specific web templates that meet your organization or person requirements and specifications.