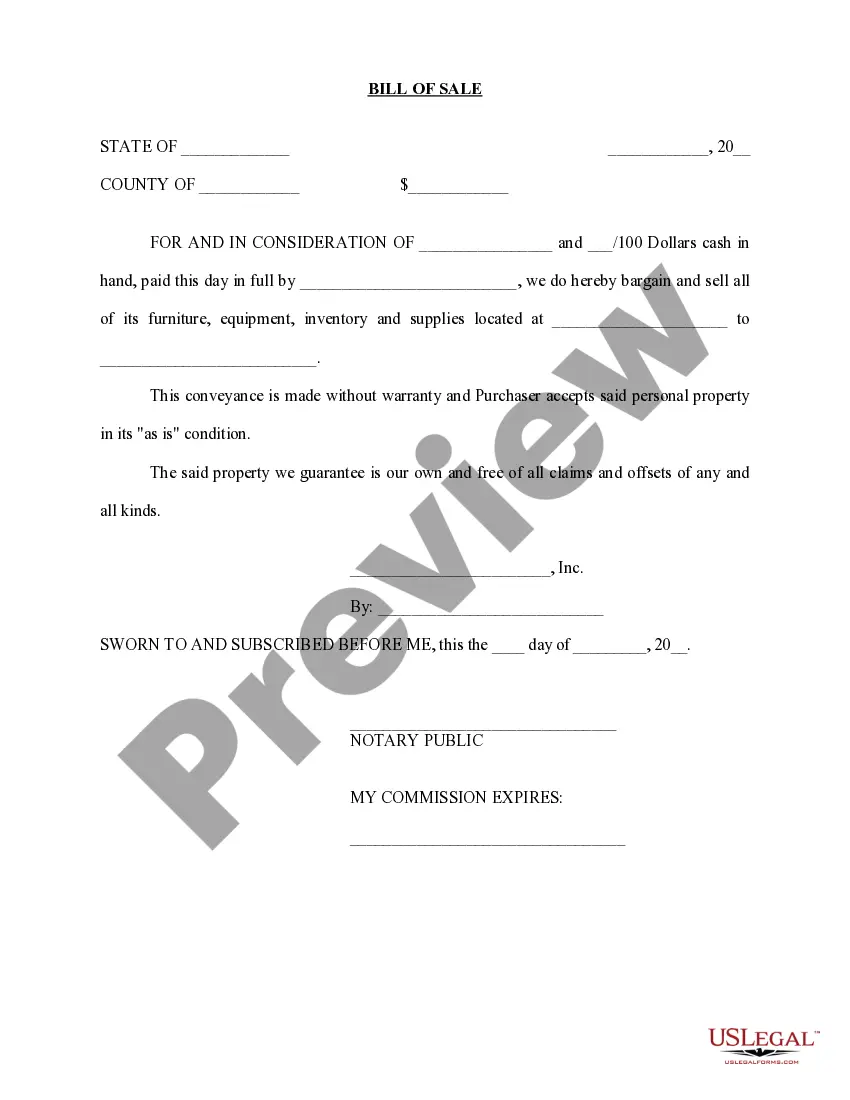

North Carolina Sale of Business — Bill of Sale for Personal Asset— - Asset Purchase Transaction is a legally binding document that outlines the transfer of personal assets from a seller to a buyer in a business sale transaction. This document ensures the smooth transfer of ownership and protects the rights and interests of both parties involved. The content of this bill of sale may vary depending on the specific assets being sold, but it typically includes the following key elements: 1. Parties Involved: The bill of sale should clearly identify the seller (current owner) and the buyer (prospective new owner) by providing their complete legal names, addresses, and contact details. 2. Description of Assets: The document should include a detailed description of the assets being sold, such as equipment, inventory, trademarks, patents, furniture, fixtures, contracts, customer lists, or any other relevant personal property. 3. Purchase Price and Payment Terms: The agreed-upon purchase price for the assets should be clearly stated, along with any specific payment terms, such as payment method, installment options, or any associated financing arrangements. 4. Representations and Warranties: The bill of sale may include representations and warranties provided by the seller regarding the assets being sold. This ensures that the seller has the legal authority to sell the assets and that they are free from any liens, claims, or encumbrances. 5. Transfer of Ownership: The document should outline the effective date of the sale and confirm that the ownership rights of the assets will be transferred from the seller to the buyer upon receipt of the agreed-upon payment. 6. Indemnification: It is common to include an indemnification clause that holds the seller harmless from any future claims, liabilities, or damages arising from the assets sold prior to the effective date of the sale. 7. Governing Law: The bill of sale should specify the governing law of the transaction, stating that it will be governed by the laws of the state of North Carolina, ensuring all legal requirements are met. Types of North Carolina Sale of Business — Bill of Sale for Personal Asset— - Asset Purchase Transaction may include: 1. Sale of Business Assets Agreement: This type of bill of sale is used when a business owner is selling all or a significant portion of their business assets, including tangible and intangible assets, like equipment, inventory, customer contracts, patents, trademarks, etc. 2. Sale of Business Real Estate and Assets Agreement: In addition to the sale of business assets, this bill of sale includes the transfer of real estate owned by the business. It covers both the real estate and personal assets involved in the transaction. In conclusion, the North Carolina Sale of Business — Bill of Sale for Personal Asset— - Asset Purchase Transaction is a crucial legal document that ensures a smooth transfer of ownership in a business sale transaction. Different types of bill of sale exist based on specific asset categories and can include a wide variety of terms and conditions specific to the assets being sold.

North Carolina Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction

Description

How to fill out North Carolina Sale Of Business - Bill Of Sale For Personal Assets - Asset Purchase Transaction?

If you want to comprehensive, download, or produce legal record layouts, use US Legal Forms, the greatest selection of legal forms, that can be found on the web. Take advantage of the site`s simple and practical research to discover the files you will need. Numerous layouts for organization and individual reasons are categorized by categories and suggests, or keywords. Use US Legal Forms to discover the North Carolina Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction within a number of click throughs.

When you are presently a US Legal Forms buyer, log in to the profile and click on the Acquire button to obtain the North Carolina Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction. You can also access forms you in the past acquired within the My Forms tab of your own profile.

If you work with US Legal Forms the first time, refer to the instructions below:

- Step 1. Ensure you have selected the shape to the proper metropolis/region.

- Step 2. Take advantage of the Review solution to look over the form`s articles. Do not forget to read through the outline.

- Step 3. When you are unsatisfied using the kind, utilize the Search area towards the top of the monitor to locate other types from the legal kind format.

- Step 4. Upon having identified the shape you will need, click on the Acquire now button. Pick the pricing prepare you choose and add your credentials to sign up to have an profile.

- Step 5. Procedure the deal. You can utilize your bank card or PayPal profile to complete the deal.

- Step 6. Choose the format from the legal kind and download it on your own system.

- Step 7. Complete, modify and produce or indication the North Carolina Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction.

Every single legal record format you purchase is yours permanently. You may have acces to each kind you acquired in your acccount. Click on the My Forms portion and select a kind to produce or download again.

Be competitive and download, and produce the North Carolina Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction with US Legal Forms. There are thousands of professional and state-certain forms you can use for your personal organization or individual needs.