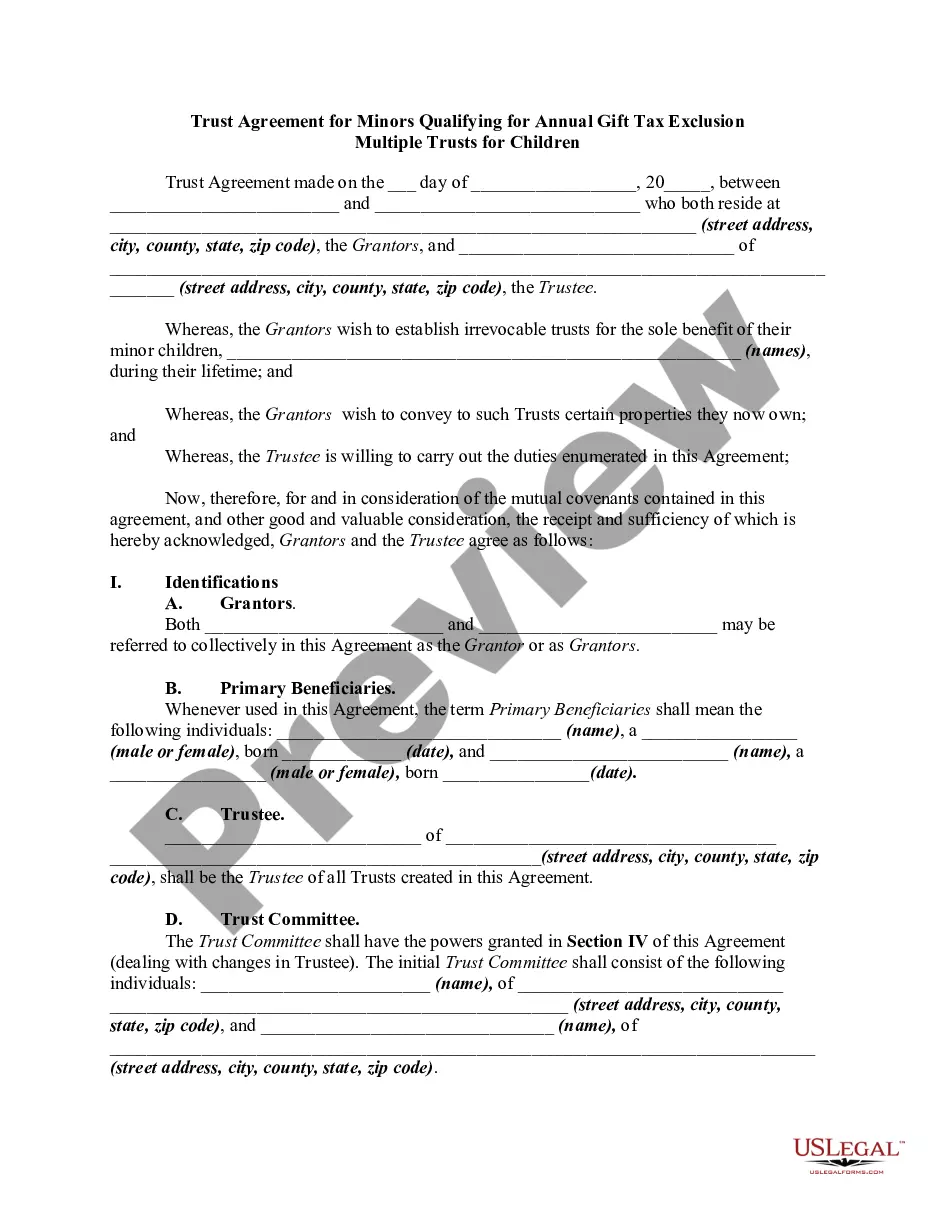

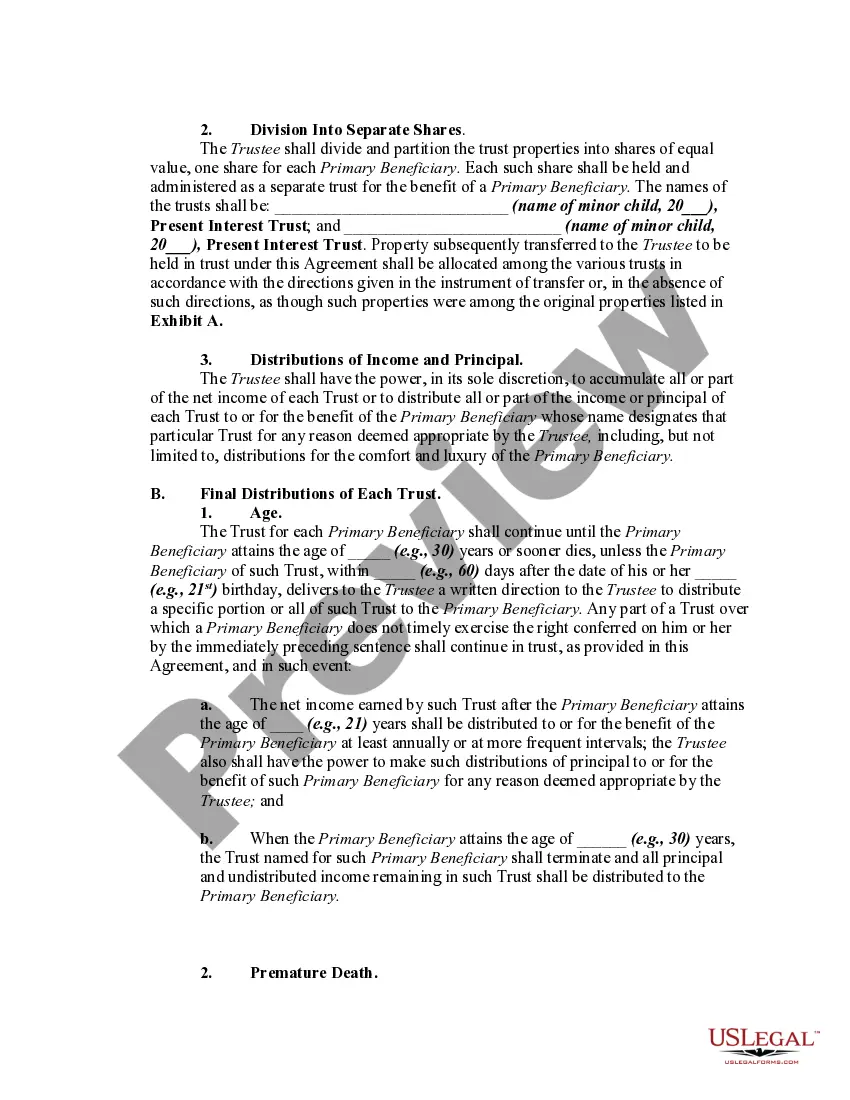

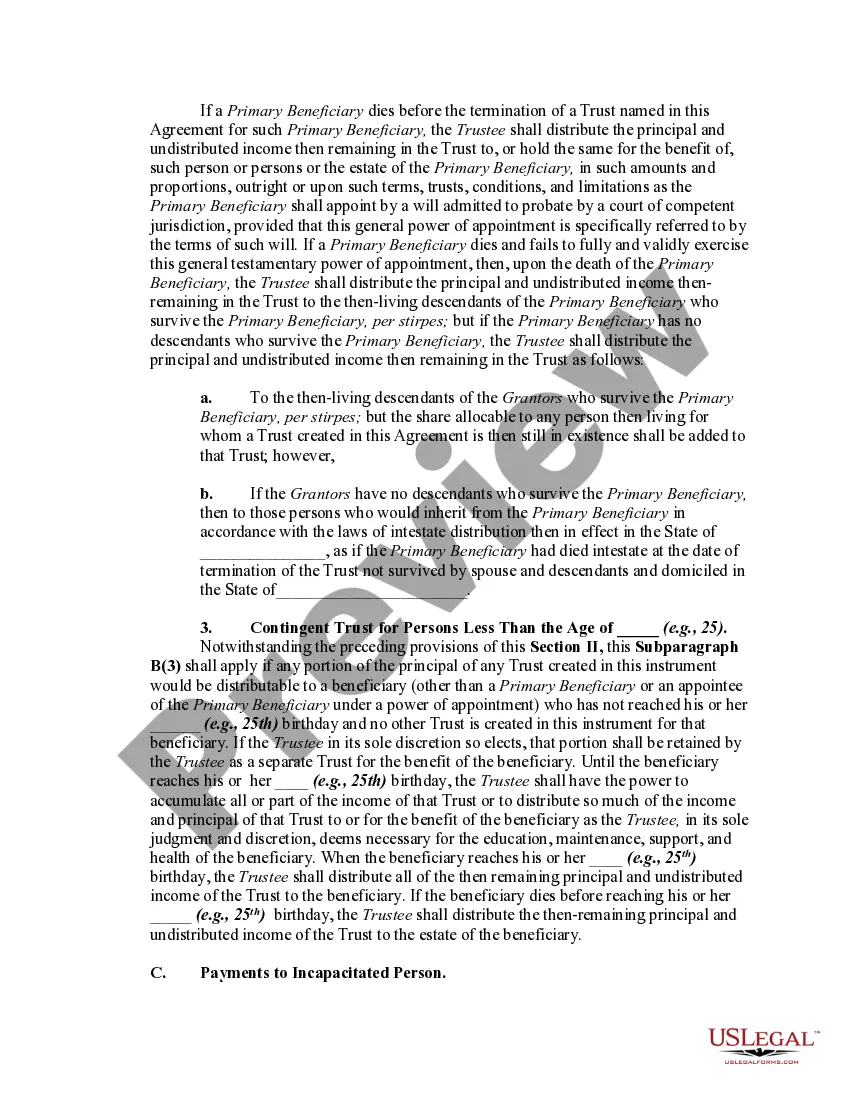

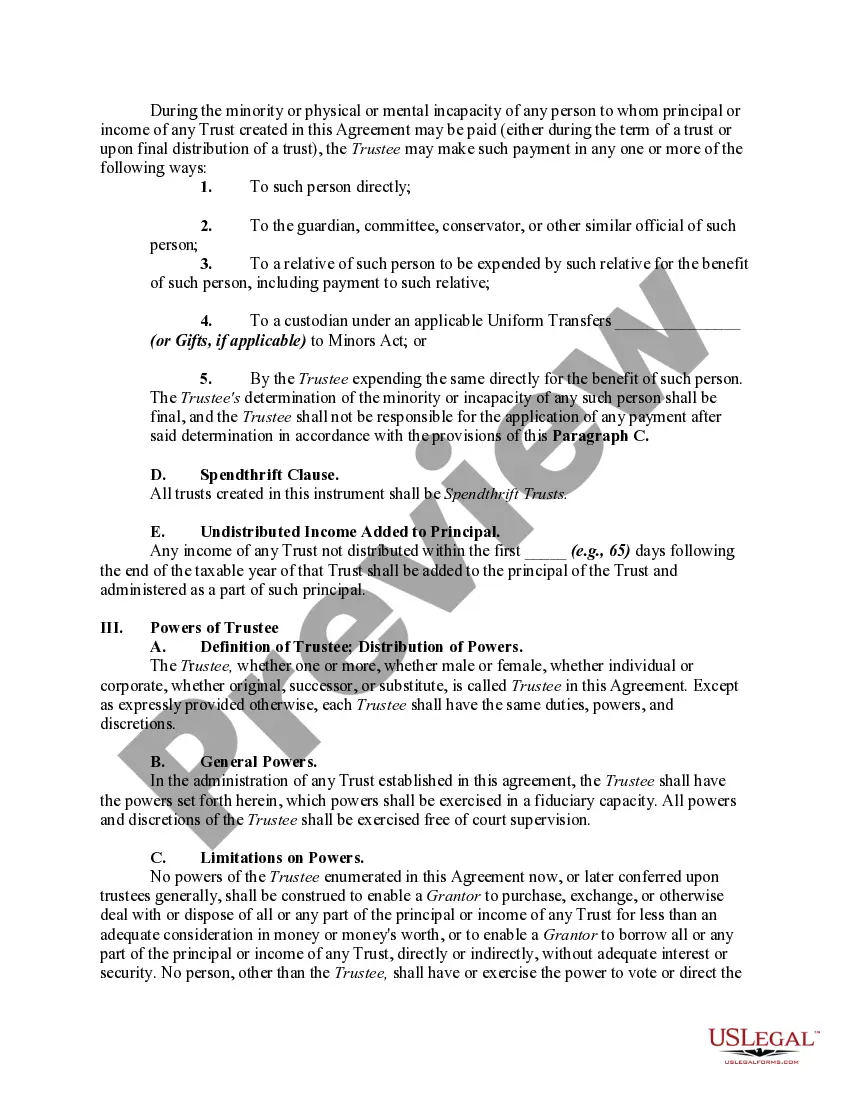

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

North Carolina Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children The North Carolina Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion is a legal document designed to establish multiple trusts for children that comply with the requirements for annual gift tax exclusion. These trusts provide an efficient and tax-advantaged method for parents or guardians to transfer wealth to their children while minimizing any potential tax burdens. In regard to different types of North Carolina Trust Agreements for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children, here are a few variations: 1. Shared Trust Agreement: In this arrangement, multiple children share a single trust under the supervision of a designated trustee. This allows for effective management of assets and enables equal disbursement of funds among the beneficiaries. 2. Individual Trust Agreement: Here, individual trusts are created for each child, ensuring independent management of assets and customization of terms based on specific needs and circumstances. 3. Graduated Trust Agreement: This type of trust agreement enables a structured distribution of assets to children over a designated period. Funds may be disbursed incrementally, for example, at specific ages or milestones, ensuring responsible financial management and gradual transfer of wealth. 4. Education Trust Agreement: This unique trust agreement focuses specifically on funding a child's education. It allows for the accumulation of funds to cover educational expenses while qualifying for the annual gift tax exclusion. 5. Special Needs Trust Agreement: In cases where a child has special needs, this trust agreement helps protect their eligibility for government benefits while providing for their financial well-being. It ensures that the child's needs are met in a way that complements and does not interfere with any government support they may receive. Regardless of the specific type of trust agreement, there are essential elements that should be included in each document. These include the identification of the granter(s) (the individual(s) establishing the trust), the trustee(s) responsible for managing the trust assets, the beneficiaries (children), and specific trust terms and conditions. These terms may include provisions for distribution of assets, investment strategies, instructions for trust termination, and the appointment of successor trustees. It is crucial to consult with a qualified attorney specializing in estate planning and trust law in North Carolina to ensure compliance with state laws and to customize the trust agreement according to individual circumstances. Creating a North Carolina Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children can provide peace of mind and financial security for both parents or guardians and their children, while effectively managing any potential tax implications.North Carolina Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children The North Carolina Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion is a legal document designed to establish multiple trusts for children that comply with the requirements for annual gift tax exclusion. These trusts provide an efficient and tax-advantaged method for parents or guardians to transfer wealth to their children while minimizing any potential tax burdens. In regard to different types of North Carolina Trust Agreements for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children, here are a few variations: 1. Shared Trust Agreement: In this arrangement, multiple children share a single trust under the supervision of a designated trustee. This allows for effective management of assets and enables equal disbursement of funds among the beneficiaries. 2. Individual Trust Agreement: Here, individual trusts are created for each child, ensuring independent management of assets and customization of terms based on specific needs and circumstances. 3. Graduated Trust Agreement: This type of trust agreement enables a structured distribution of assets to children over a designated period. Funds may be disbursed incrementally, for example, at specific ages or milestones, ensuring responsible financial management and gradual transfer of wealth. 4. Education Trust Agreement: This unique trust agreement focuses specifically on funding a child's education. It allows for the accumulation of funds to cover educational expenses while qualifying for the annual gift tax exclusion. 5. Special Needs Trust Agreement: In cases where a child has special needs, this trust agreement helps protect their eligibility for government benefits while providing for their financial well-being. It ensures that the child's needs are met in a way that complements and does not interfere with any government support they may receive. Regardless of the specific type of trust agreement, there are essential elements that should be included in each document. These include the identification of the granter(s) (the individual(s) establishing the trust), the trustee(s) responsible for managing the trust assets, the beneficiaries (children), and specific trust terms and conditions. These terms may include provisions for distribution of assets, investment strategies, instructions for trust termination, and the appointment of successor trustees. It is crucial to consult with a qualified attorney specializing in estate planning and trust law in North Carolina to ensure compliance with state laws and to customize the trust agreement according to individual circumstances. Creating a North Carolina Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children can provide peace of mind and financial security for both parents or guardians and their children, while effectively managing any potential tax implications.