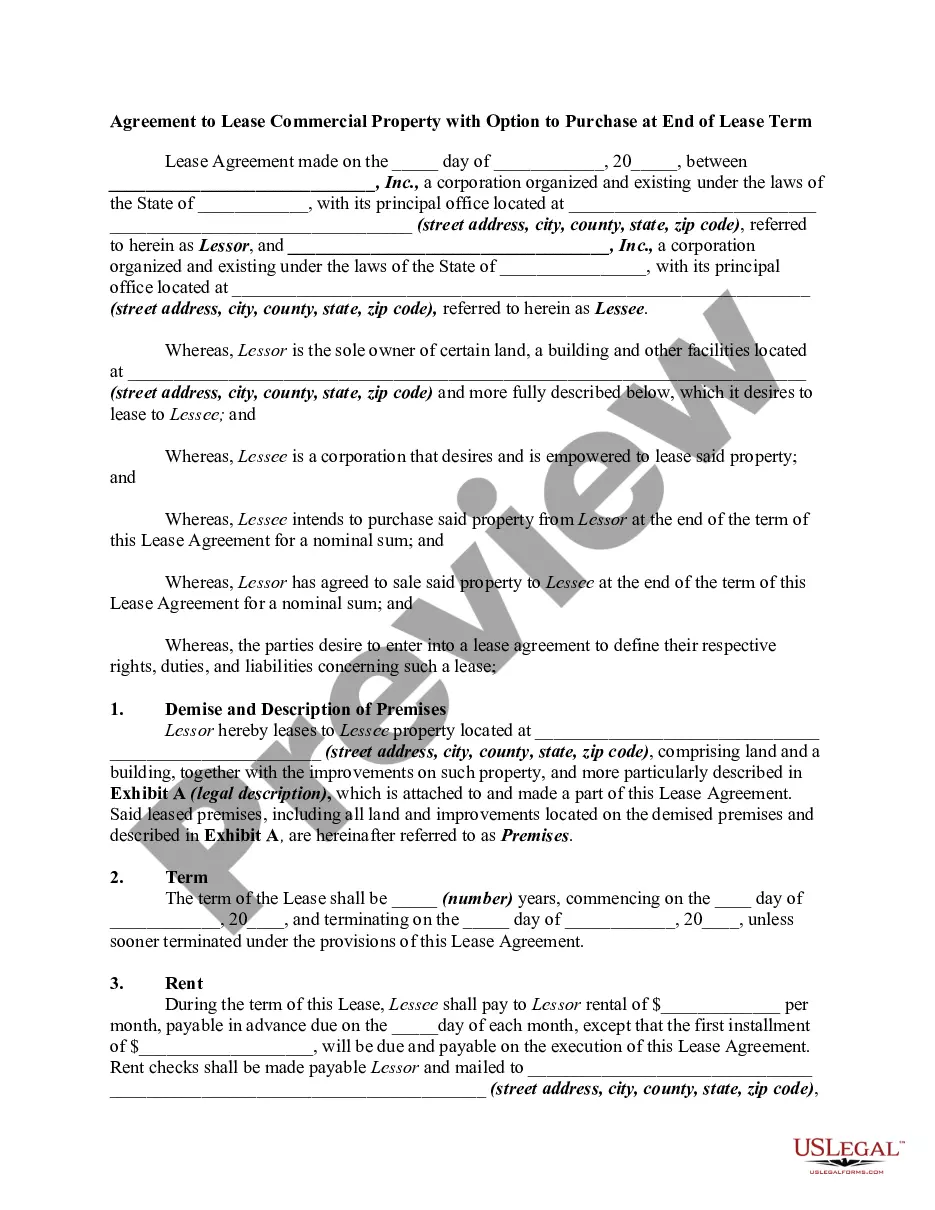

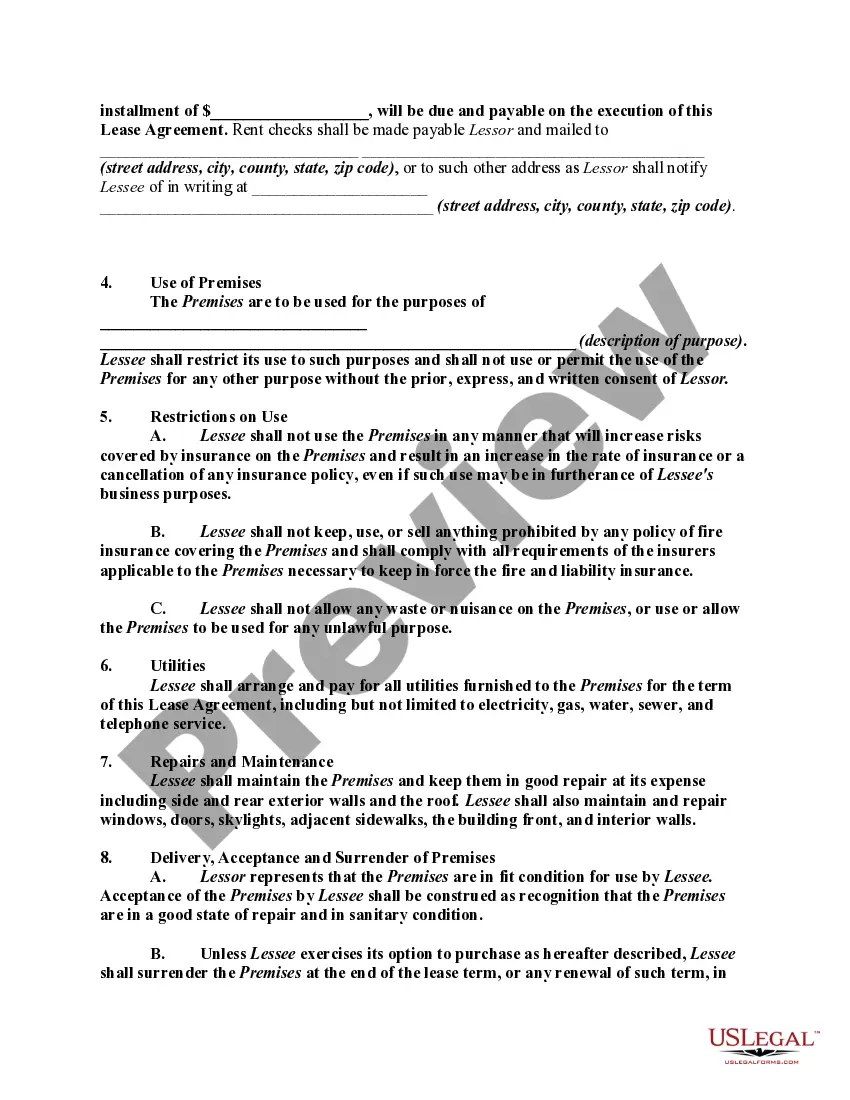

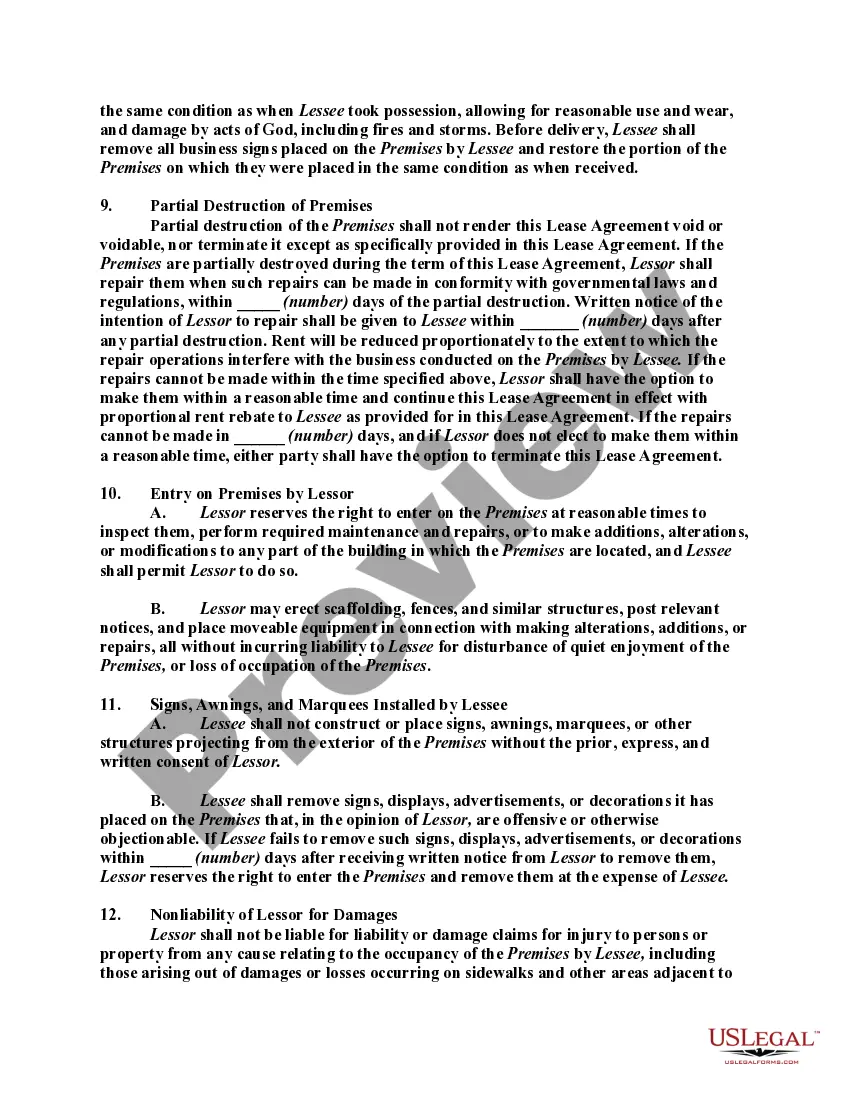

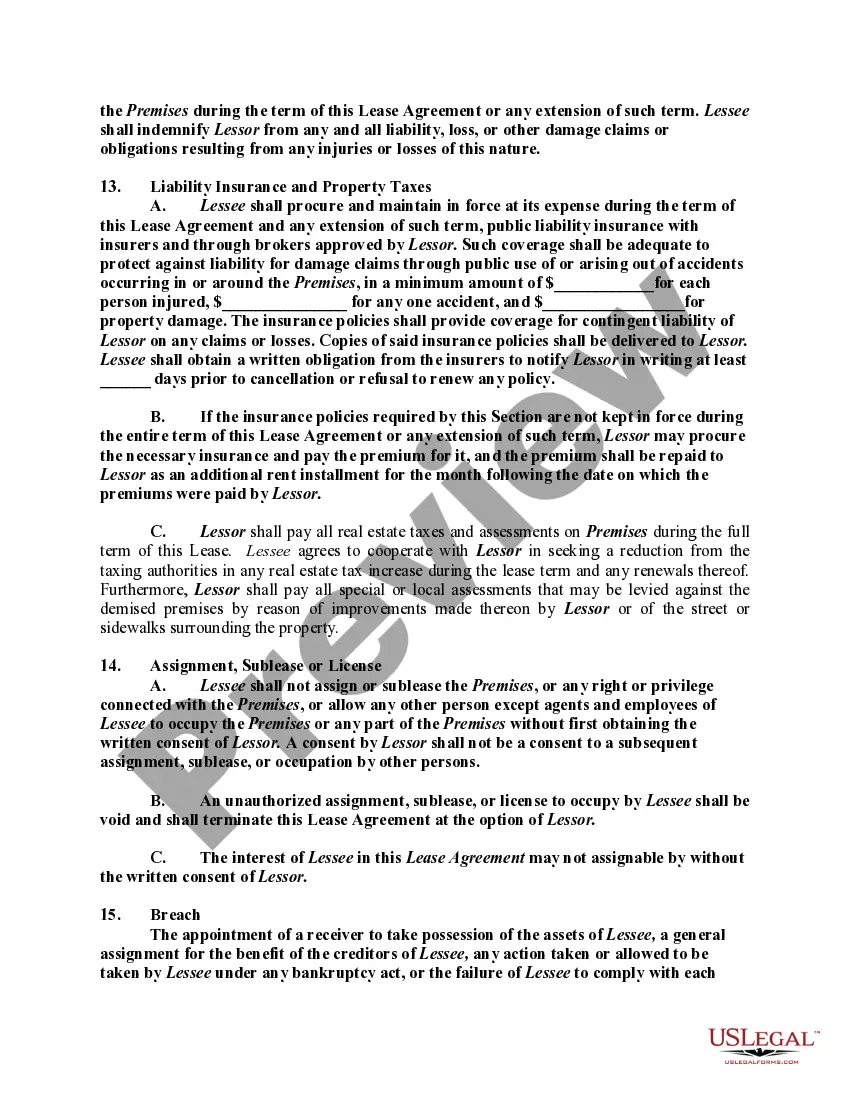

North Carolina Lease to Own for Commercial Property, also known as a lease purchase agreement, is a legal contract that allows a potential buyer, referred to as the tenant-buyer, to lease a commercial property with the option to purchase it at a later date. This option provides flexibility, allowing businesses to occupy the property and potentially become sole owners in the future. The lease to own agreement typically includes key details such as the lease term, monthly rent, purchase price, the option fee paid by the tenant-buyer, and the potential date of purchase. This arrangement permits businesses to test the location and market suitability before making a long-term commitment. In North Carolina, there are various types of lease to own options for commercial properties, including: 1. Lease with Option to Purchase: This type of agreement grants the tenant-buyer the right to purchase the property at an agreed-upon price within a specified time frame. The purchase price is usually determined at the beginning of the lease agreement. 2. Installment Sales Agreement: This variation allows the tenant-buyer to enter into an agreement where a portion of the monthly lease payment is credited towards the purchase price of the property. This allows the tenant-buyer to accumulate equity over time. 3. Lease Purchase Contract: This type of lease to own agreement commits both parties to the future purchase of the property. It legally binds the tenant-buyer to buy the property, and the property owner to sell it when specific conditions are met. Key terms and conditions that should be clearly outlined in the North Carolina lease to own agreement include the length of the lease term, monthly rent amount, security deposit, maintenance responsibilities, taxes and insurance obligations, and any other relevant provisions that protect both parties' rights during the lease period. It is essential for both parties to carefully review and negotiate the terms of the lease to own agreement before signing to ensure a mutual understanding and protection of their respective interests. Consulting with legal and real estate professionals experienced in North Carolina commercial property transactions is highly recommended ensuring compliance with state laws and regulations.

North Carolina Lease to Own for Commercial Property

Description

How to fill out North Carolina Lease To Own For Commercial Property?

If you require extensive, download, or print legal document templates, utilize US Legal Forms, the largest collection of legal documents available online.

Take advantage of the website's user-friendly and convenient search to find the documents you need.

Different templates for business and personal purposes are organized by categories and jurisdictions, or keywords.

Step 4. After locating the form you need, click the Purchase now button. Choose the payment plan you prefer and enter your details to register for an account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the purchase.

- Utilize US Legal Forms to obtain the North Carolina Lease to Own for Commercial Property in just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and select the Download button to find the North Carolina Lease to Own for Commercial Property.

- You can also access documents you previously saved in the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have selected the form for the correct area/state.

- Step 2. Use the Review option to check the form's details. Don't forget to read the description.

- Step 3. If you are dissatisfied with the form, use the Search box at the top of the page to find other versions of the legal document template.

Form popularity

FAQ

Absolutely! If you're in a position to buy property and you're eager to stay in your current home, buying from your landlord can be convenient and may also save you money given that you won't have removal fees and may also be able to complete the sale without an estate agent.

This option is called rent to buy but can also be seen as rent to own, try before you buy, and intermediate market rent. These terminologies all mean the same thing and we're about to turn the lights on by providing all the information you need to fully understand them.

The Rent to Own transaction is governed by North Carolina General Statute. No real estate broker can construct, draft or otherwise offer an Option form or any other contract requiring the drafting of provisions. This is a protection for both a Buyer and Seller.

It is not generally advisable to lease a commercial property without a written agreement. Issues typically arise when the landlord is looking to sell or take possession of the property and evict the tenant.

This lease structure makes the tenant responsible for the majority of costs. Specifically, the tenant pays the base rent, property but also taxes, insurance, utilities, and maintenance. This even includes standard property repairs associated with the commercial space being occupied.

Ok, so, generally speaking, a lease in North Carolina should be in writing and should probably be recorded.

A Triple Net Lease (NNN Lease) is the most common type of lease in commercial buildings. In a NNN lease, the rent does not include operating expenses. Operating expenses include utilities, maintenance, property taxes, insurance and property management.

Rent-to-own car financing deals can be a good way for consumers with bad or no credit histories to enter the car-buying market if the deal is fair.

How long is a typical commercial lease? Commercial leases are typically three to five years. That guarantees enough rental income for the landlords to recoup their investment.

toown or lease option agreement is a contract that states a lessee will agree to rent a home for a set period of time. Then, after living there as a renter and paying rent to the owner of the home, the occupant has an option to purchase the home when or before the lease expires.

Interesting Questions

More info

The terms and conditions herein set forth were established by and between landlord and tenant on 12/21/2003 pursuant to the provisions of California Civil Code Sections 1952 et seq. And the terms set forth in Exhibit 1 are the terms and conditions of a lease entered into by lessee and lease within the City of Los Angeles on the following terms and conditions: (1) this Lease shall be deemed to be an implied term and condition pursuant to California Civil Code Section 1952 et seq.