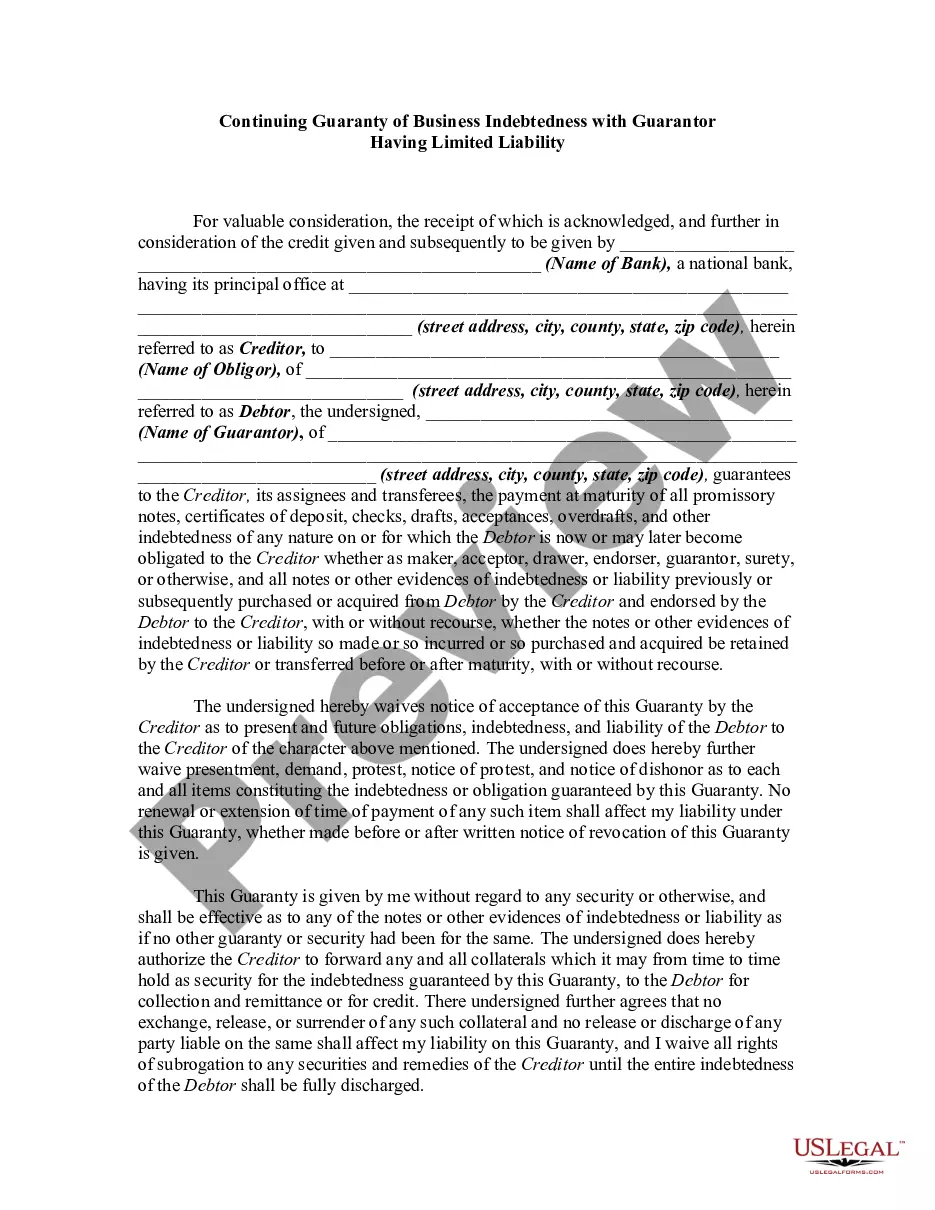

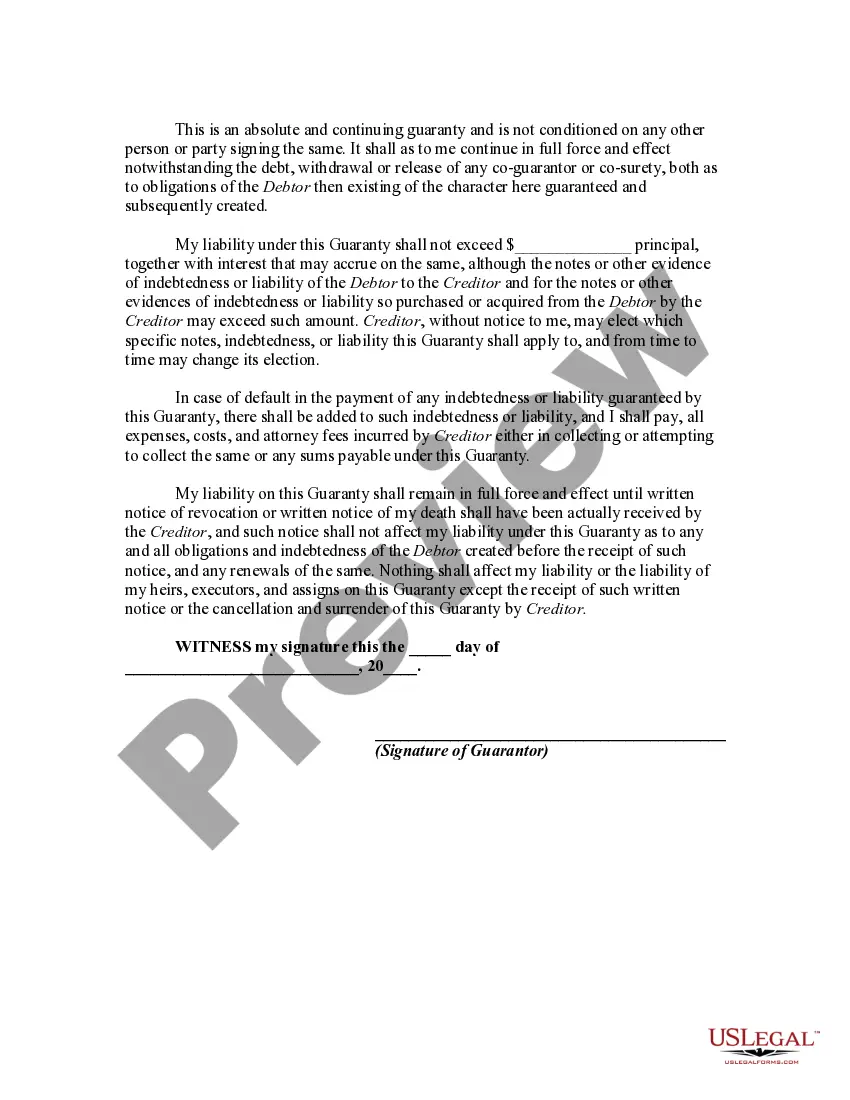

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor. A guaranty agreement is a type of contract. Thus, questions relating to such matters as validity, interpretation, and enforceability of guaranty agreements are decided in accordance with basic principles of contract law.

The North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is a legal contract that outlines the terms and conditions under which a guarantor agrees to be held responsible for the outstanding debts and obligations of a business. This type of guaranty provides some protection to the guarantor by restricting their liability to a specific amount or limiting it to certain circumstances. Keywords: North Carolina, Continuing Guaranty, Business Indebtedness, Guarantor, Limited Liability, legal contract, outstanding debts, obligations, protection. There are different types of North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability that can be tailored to meet specific needs, including: 1. Limited Liability Guaranty: This type of guaranty limits the guarantor's liability to a specific amount, typically defined in the contract. The guarantor is only responsible for the debts and obligations up to that predetermined limit, providing a level of certainty and protection. 2. Conditional Guaranty: In a conditional guaranty, the guarantor's liability is limited to certain circumstances or events specified in the contract. They are only obligated to fulfill their guarantor duties if the specified conditions are met. This type of guaranty offers more flexibility and control to the guarantor. 3. Limited Guaranty with Exceptions: This version of the continuing guaranty allows the guarantor to limit their liability while also excluding certain obligations from their responsibility. The contract explicitly enumerates the specific debts or categories of debts that are exempt from the guarantor's obligations. 4. Partial Limited Guaranty: In this type of agreement, the guarantor's liability is limited to a percentage or portion of the business's overall indebtedness. The contract would set forth the exact percentage or amount for which the guarantor will be responsible. 5. Limited Liability for Specific Obligations: This variation of the continuing guaranty restricts the guarantor's liability to specific obligations or debts. The contract clearly identifies the obligations for which the guarantor will be held accountable and excludes any other potential liabilities. It is important to consult with a legal professional to draft and understand the specific terms and provisions of a North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, ensuring compliance with state laws and individual business requirements.

The North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is a legal contract that outlines the terms and conditions under which a guarantor agrees to be held responsible for the outstanding debts and obligations of a business. This type of guaranty provides some protection to the guarantor by restricting their liability to a specific amount or limiting it to certain circumstances. Keywords: North Carolina, Continuing Guaranty, Business Indebtedness, Guarantor, Limited Liability, legal contract, outstanding debts, obligations, protection. There are different types of North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability that can be tailored to meet specific needs, including: 1. Limited Liability Guaranty: This type of guaranty limits the guarantor's liability to a specific amount, typically defined in the contract. The guarantor is only responsible for the debts and obligations up to that predetermined limit, providing a level of certainty and protection. 2. Conditional Guaranty: In a conditional guaranty, the guarantor's liability is limited to certain circumstances or events specified in the contract. They are only obligated to fulfill their guarantor duties if the specified conditions are met. This type of guaranty offers more flexibility and control to the guarantor. 3. Limited Guaranty with Exceptions: This version of the continuing guaranty allows the guarantor to limit their liability while also excluding certain obligations from their responsibility. The contract explicitly enumerates the specific debts or categories of debts that are exempt from the guarantor's obligations. 4. Partial Limited Guaranty: In this type of agreement, the guarantor's liability is limited to a percentage or portion of the business's overall indebtedness. The contract would set forth the exact percentage or amount for which the guarantor will be responsible. 5. Limited Liability for Specific Obligations: This variation of the continuing guaranty restricts the guarantor's liability to specific obligations or debts. The contract clearly identifies the obligations for which the guarantor will be held accountable and excludes any other potential liabilities. It is important to consult with a legal professional to draft and understand the specific terms and provisions of a North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, ensuring compliance with state laws and individual business requirements.