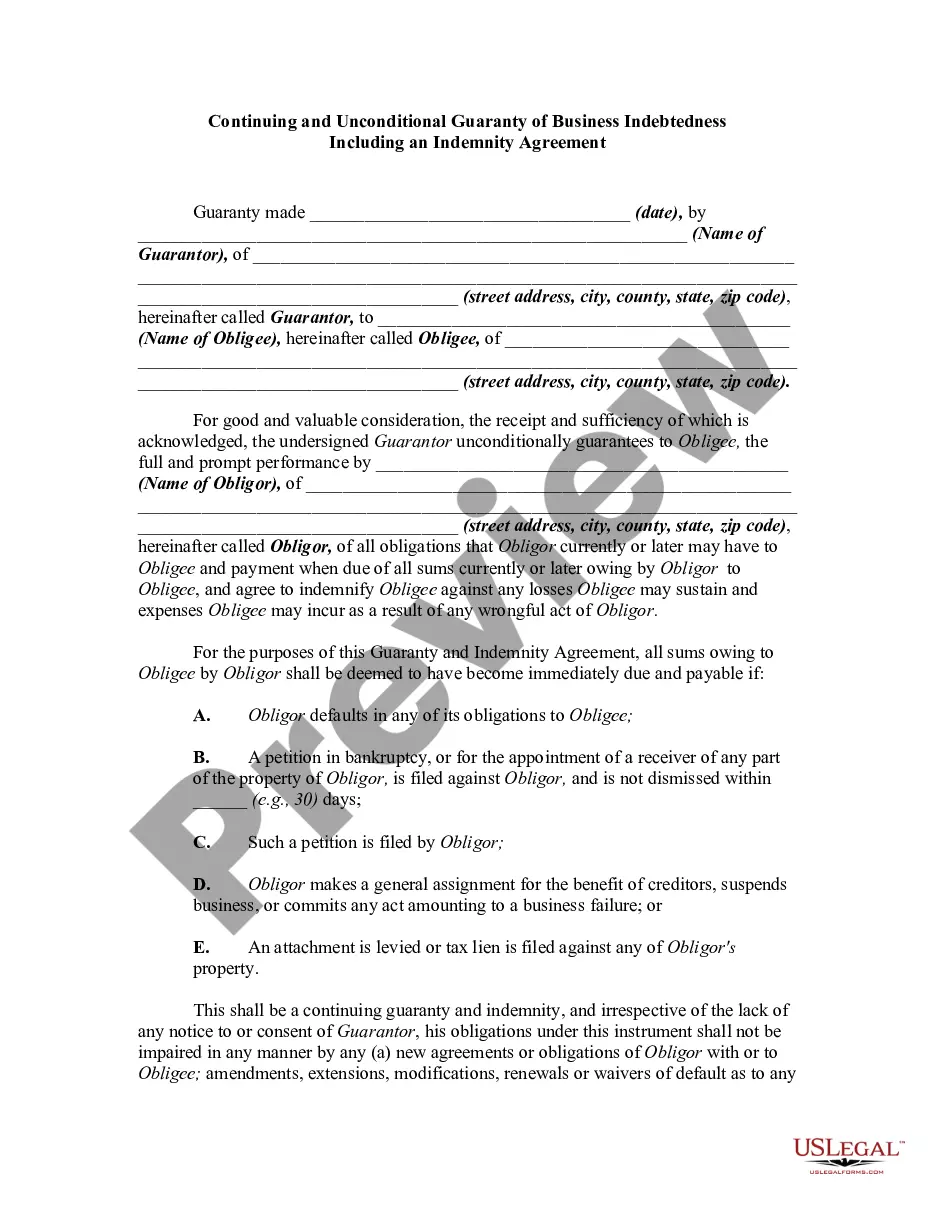

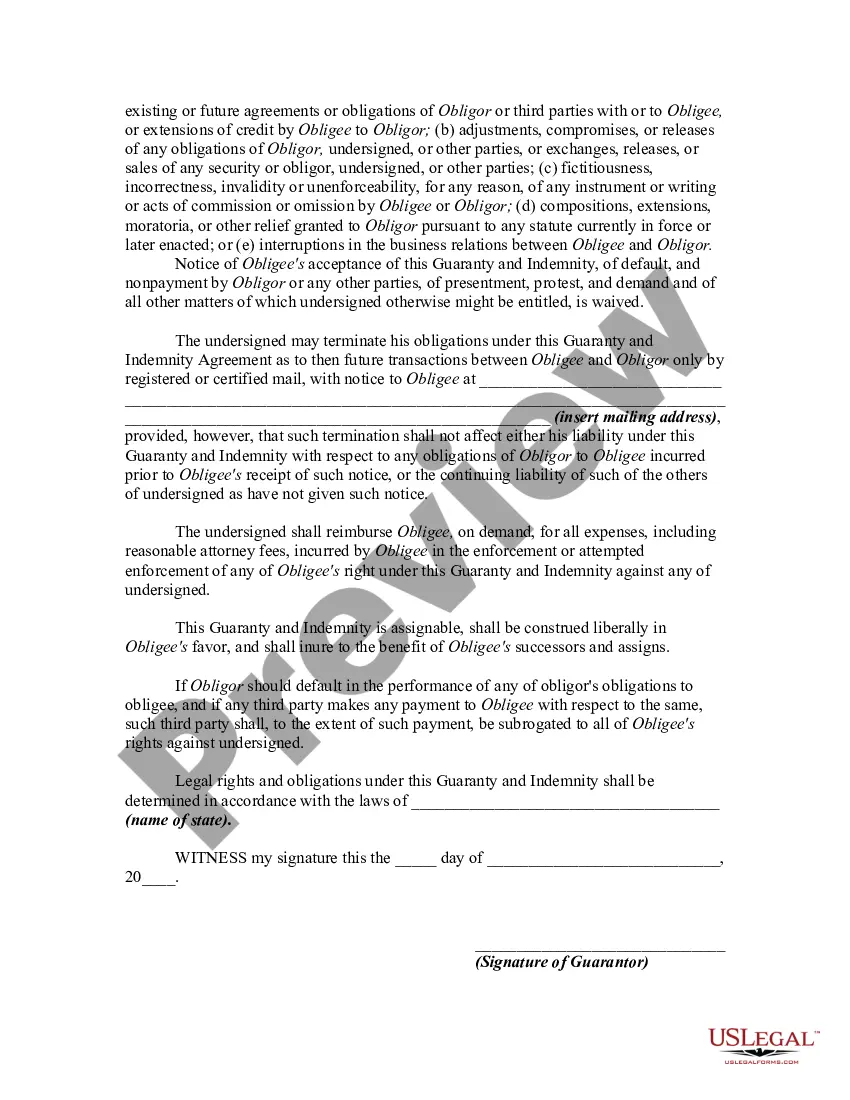

A guaranty is an undertaking on the part of one person (the guarantor) which binds the guarantor to performing the obligation of the debtor or obligor in the event of default by the debtor or obligor. The contract of guaranty may be absolute or it may be conditional. An absolute or unconditional guaranty is a contract by which the guarantor has promised that if the debtor does not perform the obligation or obligations, the guarantor will perform some act (such as the payment of money) to or for the benefit of the creditor.

A guaranty may be either continuing or restricted. The contract is restricted if it is limited to the guaranty of a single transaction or to a limited number of specific transactions and is not effective as to transactions other than those guaranteed. The contract is continuing if it contemplates a future course of dealing during an indefinite period, or if it is intended to cover a series of transactions or a succession of credits, or if its purpose is to give to the principal debtor a standing credit to be used by him or her from time to time.

A North Carolina Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement is a legally binding contract that provides an additional layer of security for lenders in the event that a business defaults on its debts. This type of agreement is commonly used in commercial transactions and can take different forms depending on the specific terms and conditions. In its essence, this agreement involves a third party, often an individual or another business entity, known as the guarantor, who agrees to take on the responsibility of repaying the business debt if the primary borrower fails to do so. The term "continuing" implies that the guarantor's obligation extends beyond a one-time guarantee, and it covers both current and future debts incurred by the borrower. The North Carolina Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement serves as a formal undertaking, providing financial security to the lender by ensuring that they have recourse in the event of default. This agreement is especially crucial when the borrower's creditworthiness or financial stability raises concerns, providing reassurance to the lender and encouraging the extension of credit. In addition to guaranteeing the repayment of business debts, this agreement often includes an indemnity clause. An indemnity agreement goes beyond guaranteeing payment, as it provides protection from any losses or damages that the lender may incur as a result of the borrower's default. It serves as a means for the lender to recover any legal costs, collection fees, or other expenses that arise from enforcing the debt. Different variations of the North Carolina Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement might exist, tailored to specific industries, loan types, or financial arrangements. Some common types include: 1. Real Estate Financing Guaranty: This pertains to mortgages or loans related to real estate properties. The guarantor is typically an individual or entity with a vested interest, such as the property owner or a related business. 2. Trade Credit Guaranty: This involves guarantors who are suppliers, manufacturers, or distributors extending credit to a business customer. The guarantee helps secure the trade credit provided, ensuring the supplier will be paid even if the customer defaults. 3. Small Business Administration (SBA) Loan Guaranty: This specific type applies when a business seeks financing through an SBA loan program. The guaranty ensures repayment of the loan by a third party if the business fails to fulfill its obligations. Overall, the North Carolina Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement is a crucial legal document that safeguards lenders from financial losses due to borrower defaults. With various types available, it is vital for all parties involved to understand the specific terms, conditions, and obligations outlined in the agreement to ensure compliance and protect their respective interests.A North Carolina Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement is a legally binding contract that provides an additional layer of security for lenders in the event that a business defaults on its debts. This type of agreement is commonly used in commercial transactions and can take different forms depending on the specific terms and conditions. In its essence, this agreement involves a third party, often an individual or another business entity, known as the guarantor, who agrees to take on the responsibility of repaying the business debt if the primary borrower fails to do so. The term "continuing" implies that the guarantor's obligation extends beyond a one-time guarantee, and it covers both current and future debts incurred by the borrower. The North Carolina Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement serves as a formal undertaking, providing financial security to the lender by ensuring that they have recourse in the event of default. This agreement is especially crucial when the borrower's creditworthiness or financial stability raises concerns, providing reassurance to the lender and encouraging the extension of credit. In addition to guaranteeing the repayment of business debts, this agreement often includes an indemnity clause. An indemnity agreement goes beyond guaranteeing payment, as it provides protection from any losses or damages that the lender may incur as a result of the borrower's default. It serves as a means for the lender to recover any legal costs, collection fees, or other expenses that arise from enforcing the debt. Different variations of the North Carolina Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement might exist, tailored to specific industries, loan types, or financial arrangements. Some common types include: 1. Real Estate Financing Guaranty: This pertains to mortgages or loans related to real estate properties. The guarantor is typically an individual or entity with a vested interest, such as the property owner or a related business. 2. Trade Credit Guaranty: This involves guarantors who are suppliers, manufacturers, or distributors extending credit to a business customer. The guarantee helps secure the trade credit provided, ensuring the supplier will be paid even if the customer defaults. 3. Small Business Administration (SBA) Loan Guaranty: This specific type applies when a business seeks financing through an SBA loan program. The guaranty ensures repayment of the loan by a third party if the business fails to fulfill its obligations. Overall, the North Carolina Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement is a crucial legal document that safeguards lenders from financial losses due to borrower defaults. With various types available, it is vital for all parties involved to understand the specific terms, conditions, and obligations outlined in the agreement to ensure compliance and protect their respective interests.