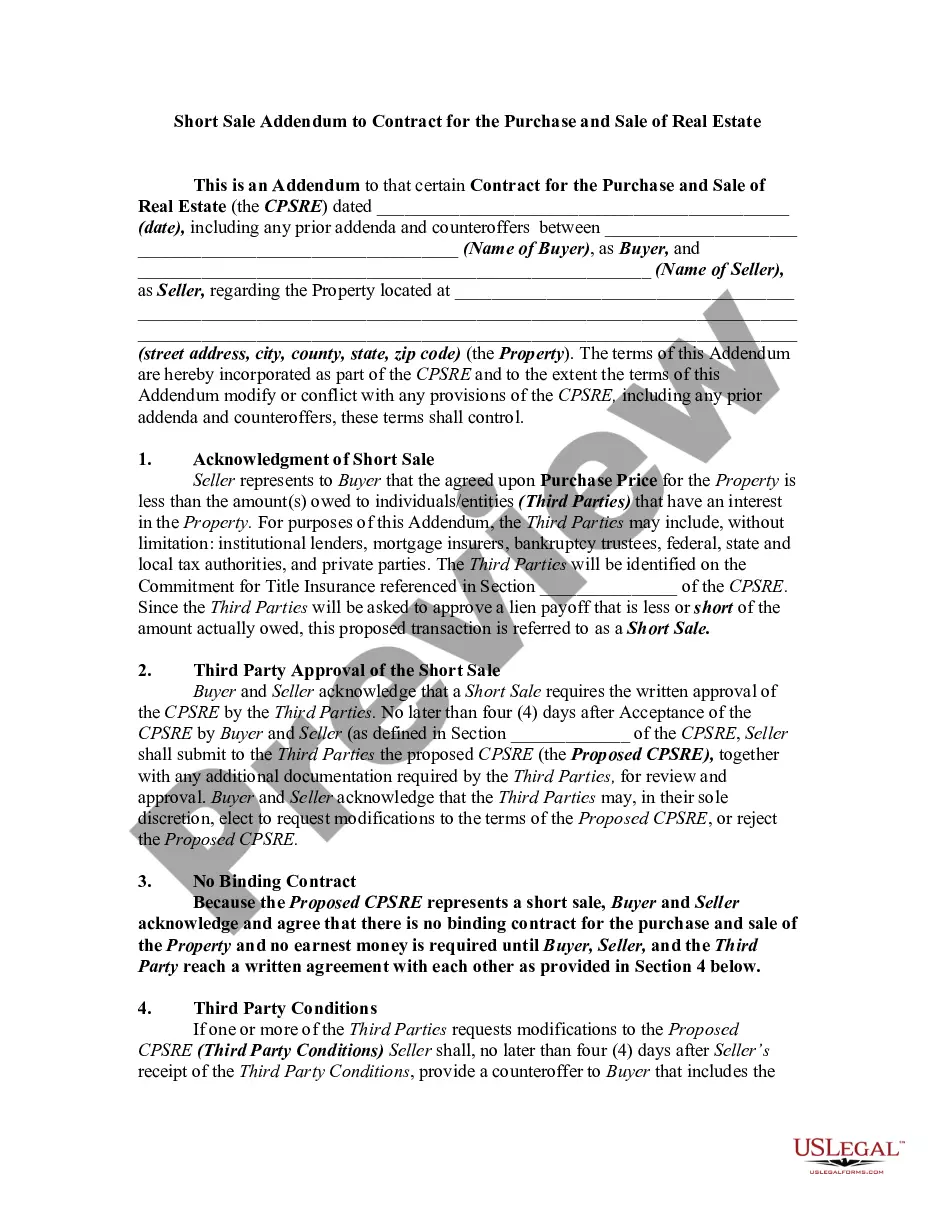

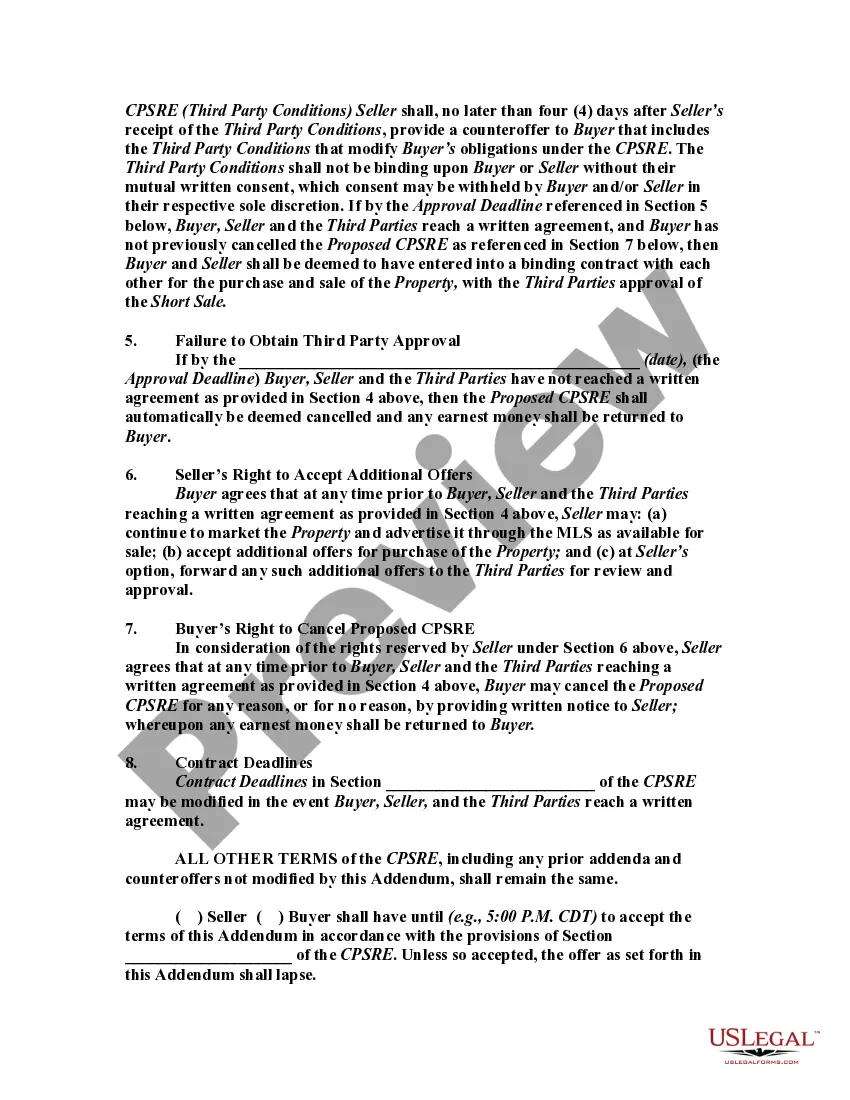

In real estate, a short sale occurs when a bank or mortgage lender agrees to discount a loan balance due to an economic hardship on the part of the mortgagor (i.e., the seller). Circumstances determine whether or not banks will discount a loan balance. These circumstances are usually related to the current real estate market climate and the individual borrower's financial situation. A short sale typically is executed to prevent a home foreclosure. Often a bank will choose to allow a short sale if they believe that it will result in a smaller financial loss than foreclosing.

This form is a sample of an Addendum to a standard real estate sales contract in order to incorporate the short sales provisions. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

In North Carolina, a Short Sale Addendum to Contract for the Price, Purchase, and Sale of Real Estate is an important document involved in the real estate transaction process. This addendum is specifically designed to address the unique aspects and requirements of a short sale transaction. A short sale occurs when the proceeds from the sale of a property fall short of the outstanding mortgage balance. This indicates that the lender or lien holder will have to approve the sale in order for it to move forward. The Short Sale Addendum serves as a contractual agreement between the buyer, seller, and lender, outlining the terms and conditions of the short sale transaction. The North Carolina Short Sale Addendum provides detailed information about the property being sold, including its legal description, physical address, and tax parcel identification number. It also incorporates the terms of the original purchase and sale contract, with specific references to addendum provisions. This ensures that the short sale addendum acts as an extension of the primary contract while incorporating unique conditions related to the short sale process. The addendum outlines important aspects such as the required lender approval and any associated timelines. It specifies the responsibilities and obligations of all parties involved, addressing key elements like the submission of necessary documentation, dealing with outstanding liens, and negotiating any deficiency judgments. In North Carolina, there are no specific variations or types of Short Sale Addendums defined by the state as they are usually customized to meet the requirements of each specific short sale scenario. The addendum is typically prepared by the seller's real estate agent, attorney, or lender, and presented to the buyer for review and acceptance. It is important for all parties involved in a short sale transaction to fully understand and comply with the terms of the Short Sale Addendum for a smooth and successful completion of the sale. Working closely with experienced professionals, such as a real estate agent specializing in short sales or a real estate attorney, can help navigate the complexities associated with short sale transactions in North Carolina.In North Carolina, a Short Sale Addendum to Contract for the Price, Purchase, and Sale of Real Estate is an important document involved in the real estate transaction process. This addendum is specifically designed to address the unique aspects and requirements of a short sale transaction. A short sale occurs when the proceeds from the sale of a property fall short of the outstanding mortgage balance. This indicates that the lender or lien holder will have to approve the sale in order for it to move forward. The Short Sale Addendum serves as a contractual agreement between the buyer, seller, and lender, outlining the terms and conditions of the short sale transaction. The North Carolina Short Sale Addendum provides detailed information about the property being sold, including its legal description, physical address, and tax parcel identification number. It also incorporates the terms of the original purchase and sale contract, with specific references to addendum provisions. This ensures that the short sale addendum acts as an extension of the primary contract while incorporating unique conditions related to the short sale process. The addendum outlines important aspects such as the required lender approval and any associated timelines. It specifies the responsibilities and obligations of all parties involved, addressing key elements like the submission of necessary documentation, dealing with outstanding liens, and negotiating any deficiency judgments. In North Carolina, there are no specific variations or types of Short Sale Addendums defined by the state as they are usually customized to meet the requirements of each specific short sale scenario. The addendum is typically prepared by the seller's real estate agent, attorney, or lender, and presented to the buyer for review and acceptance. It is important for all parties involved in a short sale transaction to fully understand and comply with the terms of the Short Sale Addendum for a smooth and successful completion of the sale. Working closely with experienced professionals, such as a real estate agent specializing in short sales or a real estate attorney, can help navigate the complexities associated with short sale transactions in North Carolina.