North Carolina Owner Financing Contract for Moblie Home

Description

How to fill out Owner Financing Contract For Moblie Home?

Have you ever found yourself in a circumstance where you require documents for either business or personal purposes almost every workday.

There are numerous legal document templates accessible online, but identifying versions you can trust is quite challenging.

US Legal Forms provides thousands of form templates, including the North Carolina Owner Financing Agreement for Mobile Home, designed to comply with federal and state regulations.

Choose a convenient document format and download your copy.

Access all the document templates you have acquired in the My documents section. You can obtain another copy of the North Carolina Owner Financing Agreement for Mobile Home anytime, if required. Just select the desired form to download or print the document template.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- Then, you can download the North Carolina Owner Financing Agreement for Mobile Home template.

- If you don’t have an account and wish to start using US Legal Forms, follow these instructions.

- Acquire the form you need and ensure it is for the correct city/county.

- Utilize the Preview button to evaluate the document.

- Review the description to confirm you have selected the correct form.

- If the document is not what you are looking for, use the Search bar to locate the form that satisfies your needs and requirements.

- Once you find the correct document, click Purchase now.

- Select the pricing plan you prefer, complete the necessary information to create your account, and pay for the order using your PayPal or credit card.

Form popularity

FAQ

The average credit score required to buy a mobile home varies by lender, but it generally falls between 580 to 620. A score within this range may qualify you for financing, although lower scores can also be considered through owner financing options. Using a North Carolina Owner Financing Contract for Mobile Home can provide a more lenient path for buyers with varying credit situations.

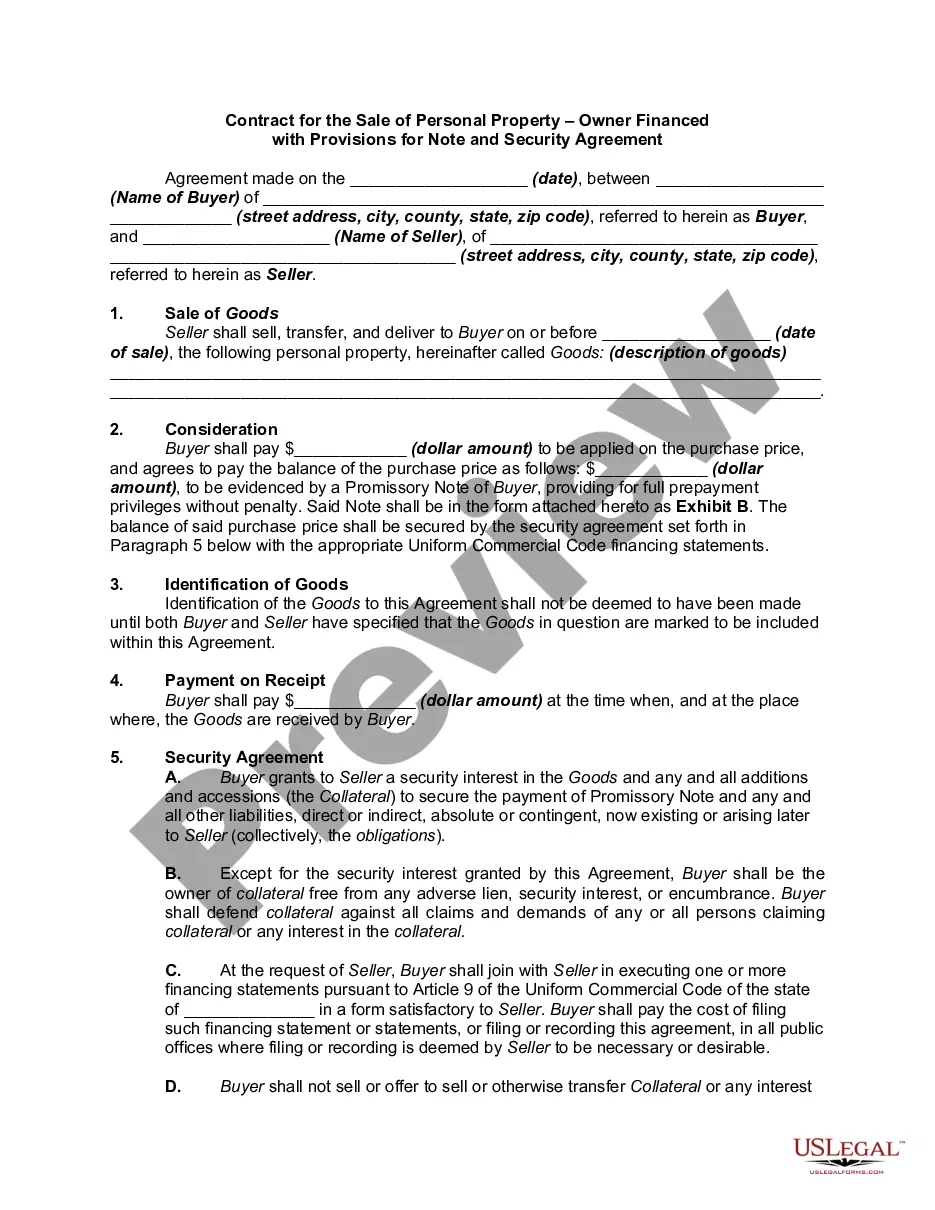

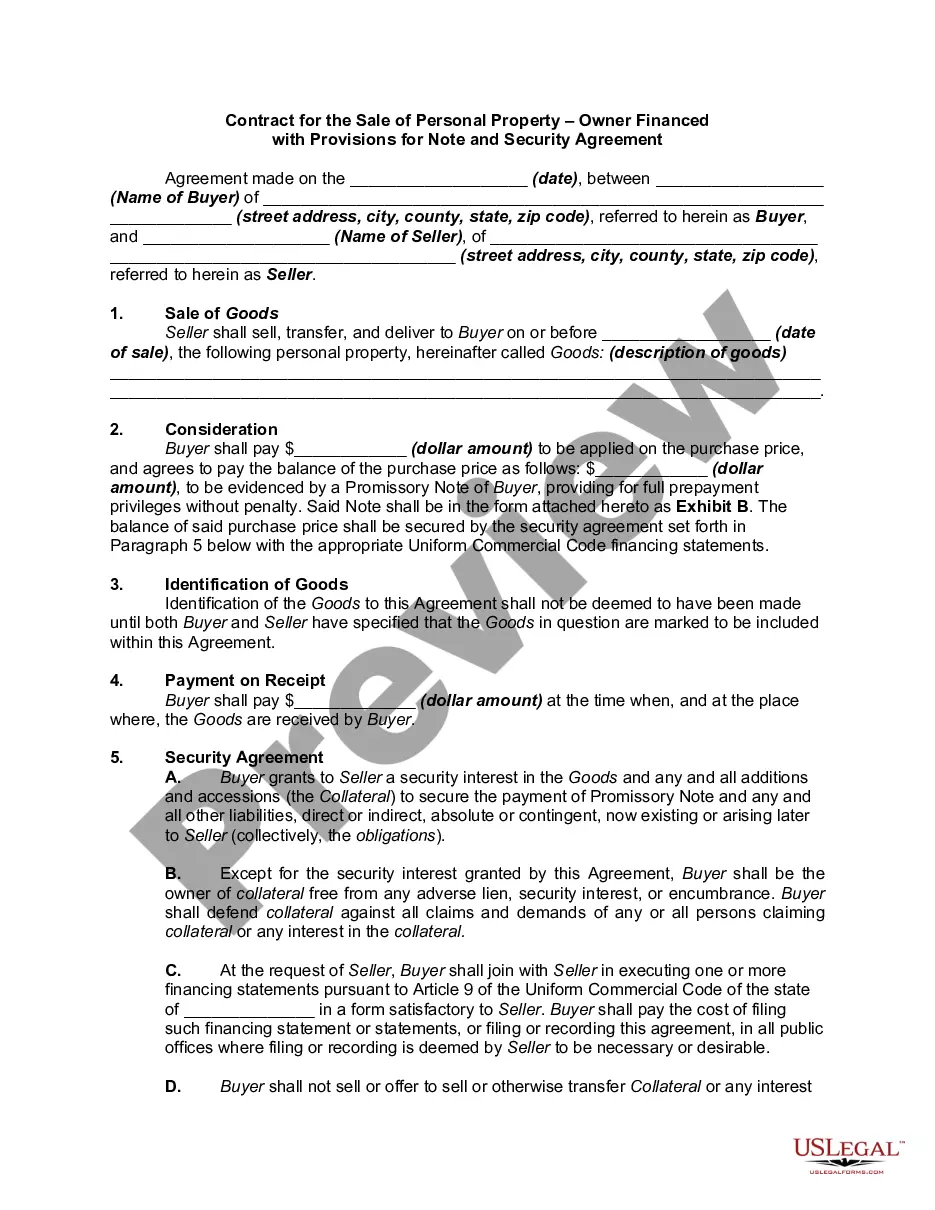

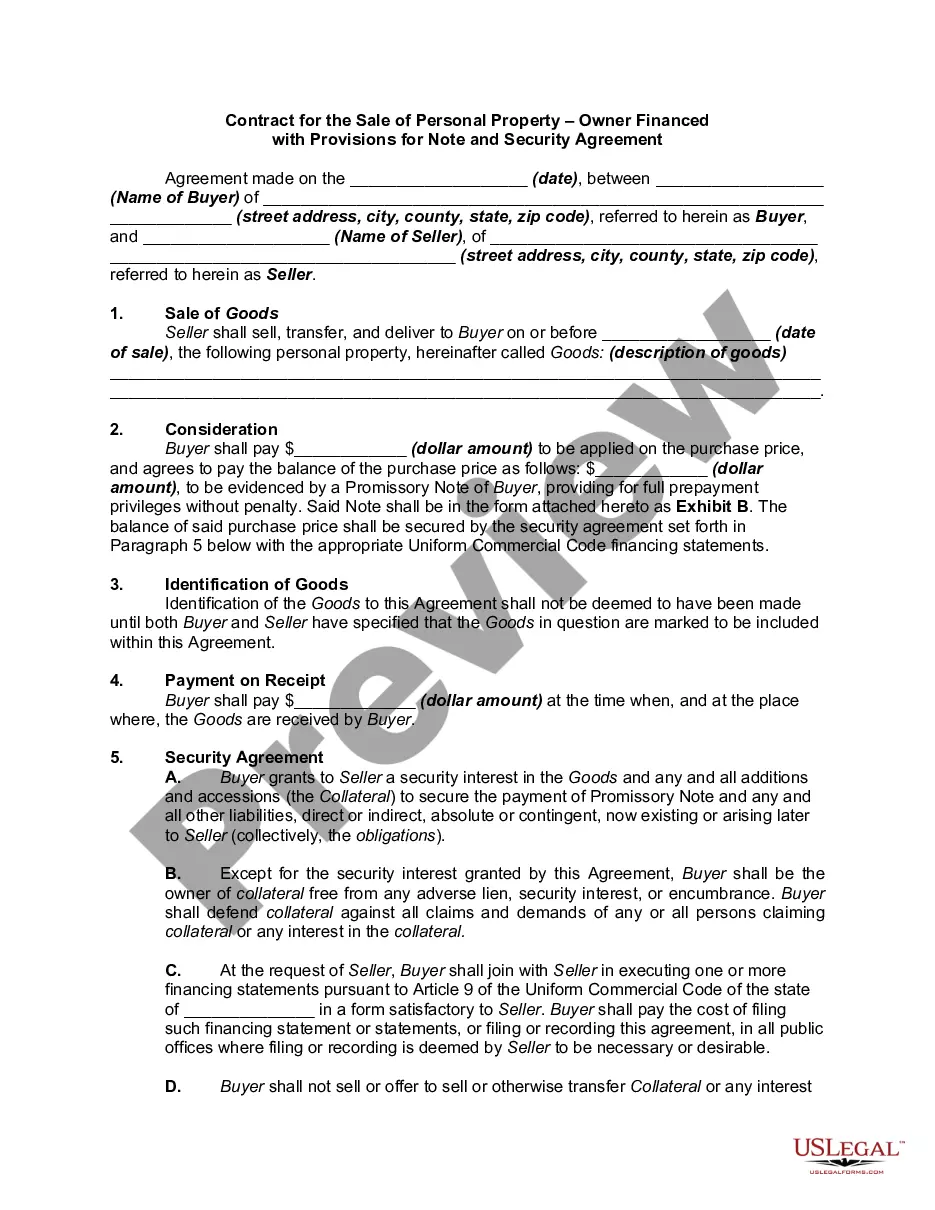

Yes, you can owner finance a mobile home in North Carolina. This arrangement allows the seller to directly finance the buyer, bypassing traditional lenders. It is a flexible option that can benefit both parties, especially when using a North Carolina Owner Financing Contract for Mobile Home. This contract outlines the terms, ensuring a clear understanding of payment schedules and responsibilities.

Different types of owner financing include land contracts, lease options, and wraparound mortgages. Each of these methods offers unique benefits and structures that can accommodate the needs of both buyers and sellers. A well-structured North Carolina Owner Financing Contract for Mobile Home can facilitate a beneficial agreement tailored to the situation of both parties.

Owner financing offers an appealing alternative to traditional mortgages, especially for buyers who may struggle to qualify for loans. It allows buyers to negotiate terms directly with sellers, which can make the process more flexible. In North Carolina, using an Owner Financing Contract for Mobile Home can provide buyers access to properties they might not otherwise afford.

If the buyer defaults on a North Carolina Owner Financing Contract for Mobile Home, the seller can take several actions. Typically, the buyer risks losing their investment, as the seller has the right to reclaim the mobile home. The contract may outline specific terms regarding default, including potential grace periods and notice requirements. It is essential for both parties to understand these terms clearly, and platforms like uslegalforms can provide guidance to create a solid and fair contract.

In a North Carolina Owner Financing Contract for Mobile Home, the lender typically does not hold the deed. Instead, the seller retains ownership of the deed while allowing the buyer to occupy and use the property. This arrangement provides a layer of security for the seller, as they still have legal title to the mobile home until the financing terms are fully met. Understanding this concept is crucial for both parties involved in the transaction.

In owner financing, the seller typically retains the deed to the mobile home until the buyer completes all payment obligations outlined in the North Carolina Owner Financing Contract for Mobile Home. This arrangement protects the seller's interests while allowing the buyer to occupy and improve the property. Once the final payment is made, the seller should transfer the deed to the buyer. This ensures a clear transfer of ownership and title.

Typical terms for owner financing vary but generally include a down payment of 10% to 20%, with repayment periods ranging from 3 to 10 years. Interest rates may range from 5% to 10%, depending on the buyer’s creditworthiness and the seller’s preferences. The North Carolina Owner Financing Contract for Mobile Home should clearly outline these terms to provide clarity and protection for both parties. Comparing these terms with traditional financing options can also help in making informed decisions.

While owner financing offers flexibility, there are downsides to consider. Buyers might face higher interest rates compared to traditional loans, and sellers may risk default without the protections afforded by a bank. Additionally, it is crucial for both parties to have a solid North Carolina Owner Financing Contract for Mobile Home in place, as a lack of formal agreements can lead to disputes. Understanding these factors helps mitigate potential issues.