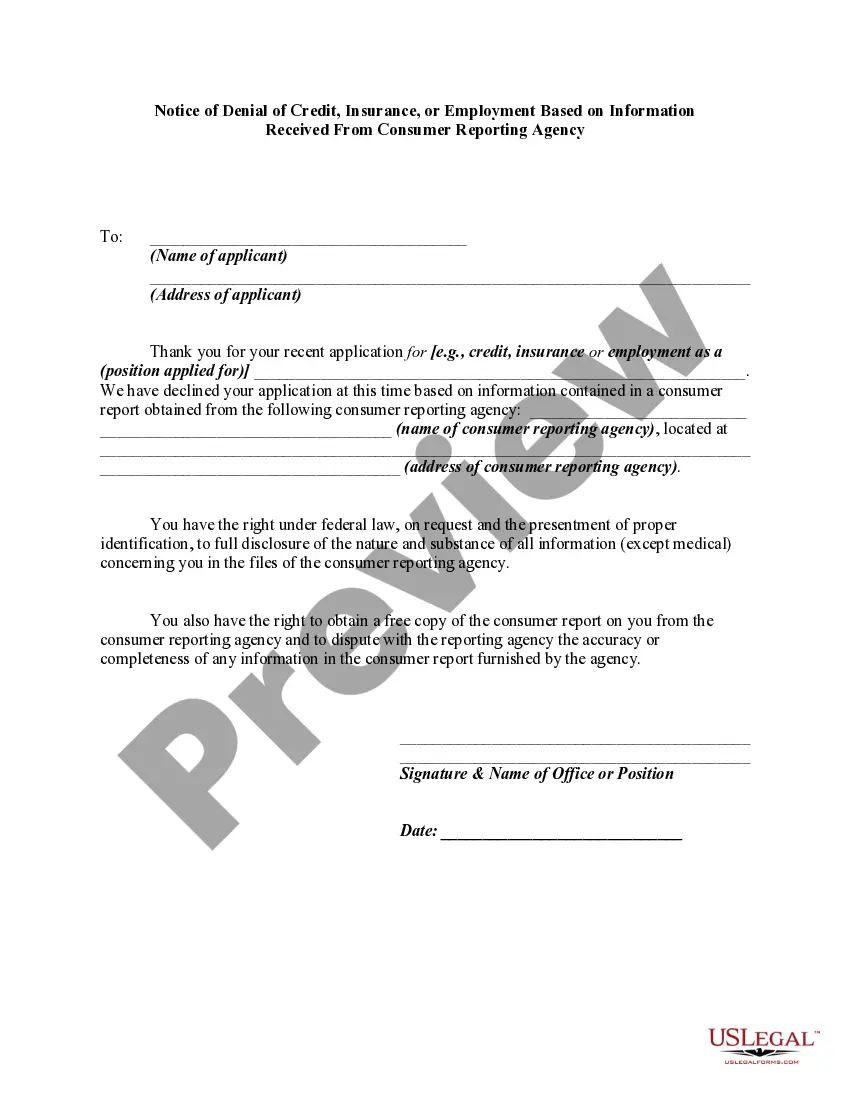

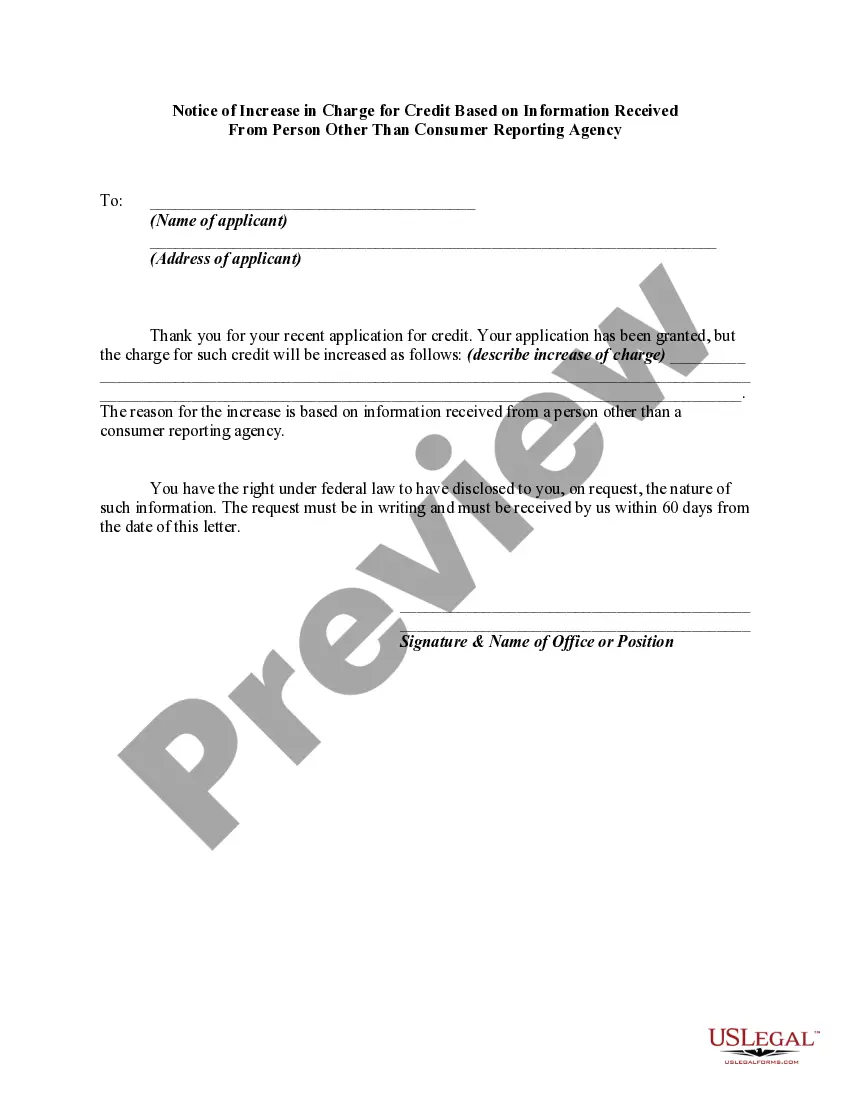

Under the Fair Credit Reporting Act, whenever credit or insurance for personal, family, or household purposes, or employment involving a consumer is denied, or the charge for such credit or insurance is increased, either wholly or partly because of information contained in a consumer report from a consumer reporting agency, the user of the consumer report must:

notify the consumer of the adverse action,

identify the consumer reporting agency making the report, and

notify the consumer of the consumer's right to obtain a free copy of a consumer report on the consumer from the consumer reporting agency and to dispute with the reporting agency the accuracy or completeness of any information in the consumer report furnished by the agency.

North Carolina Notice of Increase in Charge for Credit or Insurance Based on Information Received From Consumer Reporting Agency

Category:

State:

Multi-State

Control #:

US-01410BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Notice Of Increase In Charge For Credit Or Insurance Based On Information Received From Consumer Reporting Agency?

Are you presently within a position that you will need documents for either organization or person uses almost every day time? There are tons of lawful document templates available on the net, but locating versions you can rely on isn`t effortless. US Legal Forms gives a large number of kind templates, much like the North Carolina Notice of Increase in Charge for Credit or Insurance Based on Information Received From Consumer Reporting Agency, which can be composed to fulfill state and federal specifications.

If you are currently informed about US Legal Forms website and possess your account, merely log in. Next, you are able to download the North Carolina Notice of Increase in Charge for Credit or Insurance Based on Information Received From Consumer Reporting Agency format.

If you do not have an account and wish to start using US Legal Forms, follow these steps:

- Discover the kind you want and ensure it is for the proper town/area.

- Utilize the Review option to check the shape.

- Look at the outline to actually have selected the proper kind.

- If the kind isn`t what you`re looking for, utilize the Research field to get the kind that meets your needs and specifications.

- When you discover the proper kind, just click Acquire now.

- Pick the costs program you would like, complete the specified info to make your money, and buy your order utilizing your PayPal or credit card.

- Select a handy file format and download your copy.

Discover every one of the document templates you have bought in the My Forms menus. You can aquire a more copy of North Carolina Notice of Increase in Charge for Credit or Insurance Based on Information Received From Consumer Reporting Agency at any time, if needed. Just go through the essential kind to download or print the document format.

Use US Legal Forms, the most comprehensive collection of lawful kinds, to save time as well as stay away from blunders. The assistance gives professionally made lawful document templates which can be used for a variety of uses. Generate your account on US Legal Forms and start generating your daily life easier.

Form popularity

FAQ

The short answer is no. There is no direct affect between car insurance and your credit, paying your insurance bill late or not at all could lead to debt collection reports. Debt collection reports do appear on your credit report (often for 7-10 years) and can be read by future lenders.

Most of Your Everyday Bills Are Not Reported While your credit card accounts and lines of credit are pulled into your credit report, your day-to-day bills, such as your rent and utility payments like Internet, water, and electricity aren't roped in.

Typically, credit providers report data to the credit bureaus approximately every 30 days. Your credit report also shows any defaults ? accounts that are more than three months in arrears and where the credit provider has noted that you are in default.

In Quebec, it's become common practice: when you're shopping around for automobile or home insurance, most insurers will ask for permission to look at your credit score. Know that you're free to refuse their request.

Why do insurance companies use credit information? Some insurance companies have shown that information in a credit report can predict which consumers are likely to file insurance claims. They believe that consumers who are more likely to file claims should pay more for their insurance.

Virtually any small business or organization that extends credit to consumers can report this data to the four credit reporting agencies. Experian, Equifax, Innovis, and TransUnion will all accept information about your customers' or tenants' payments.