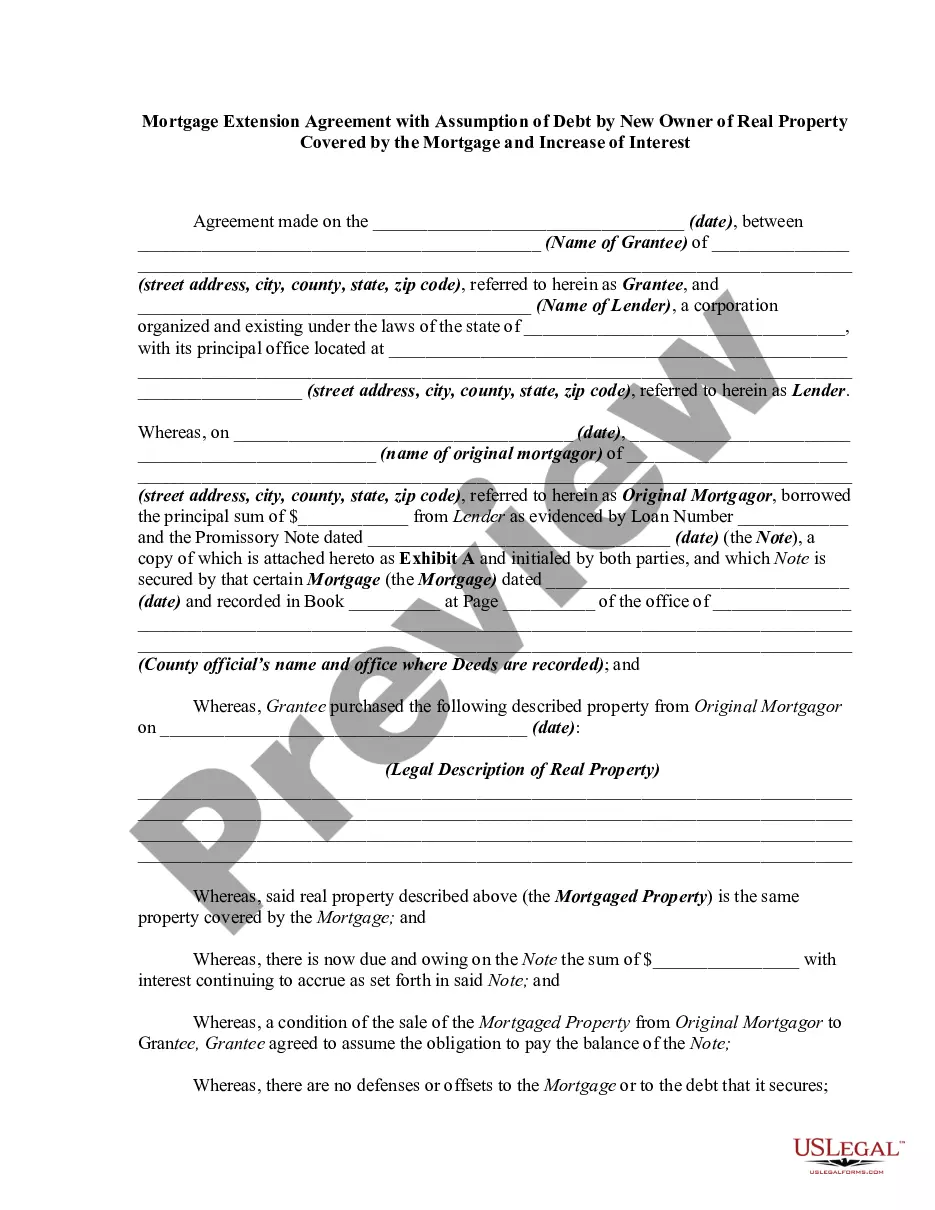

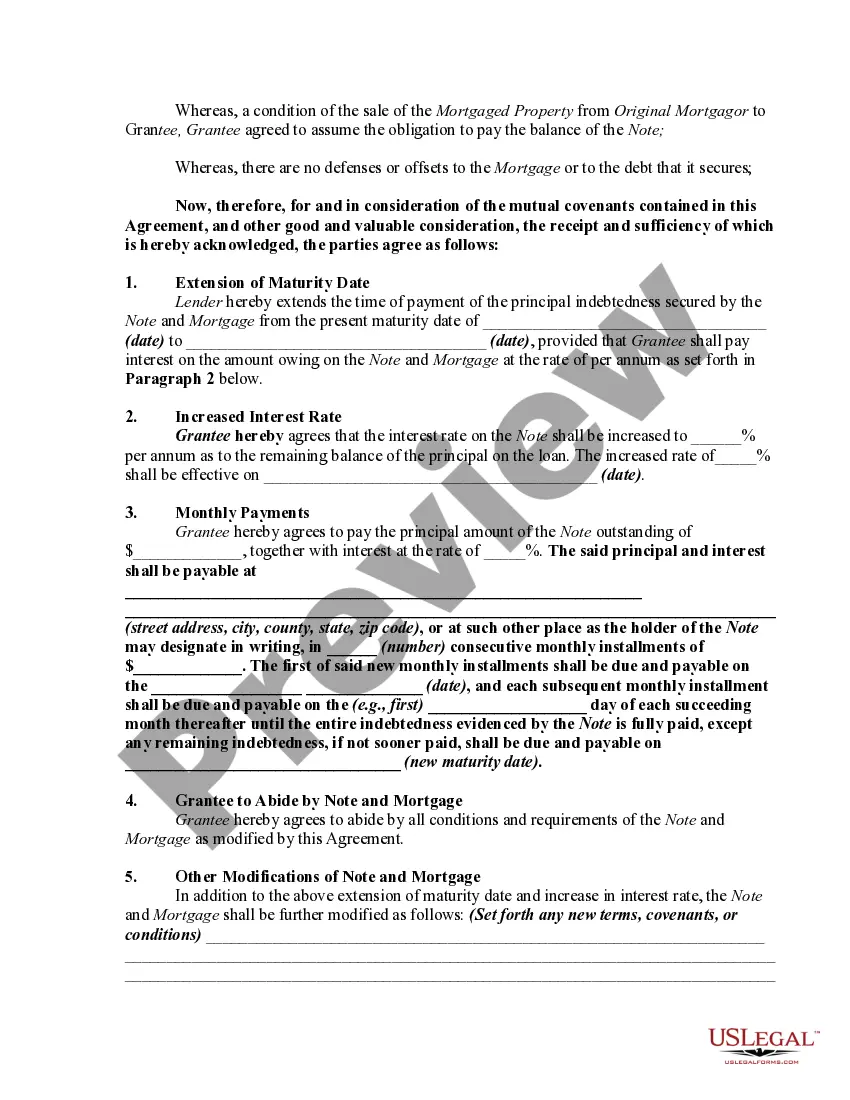

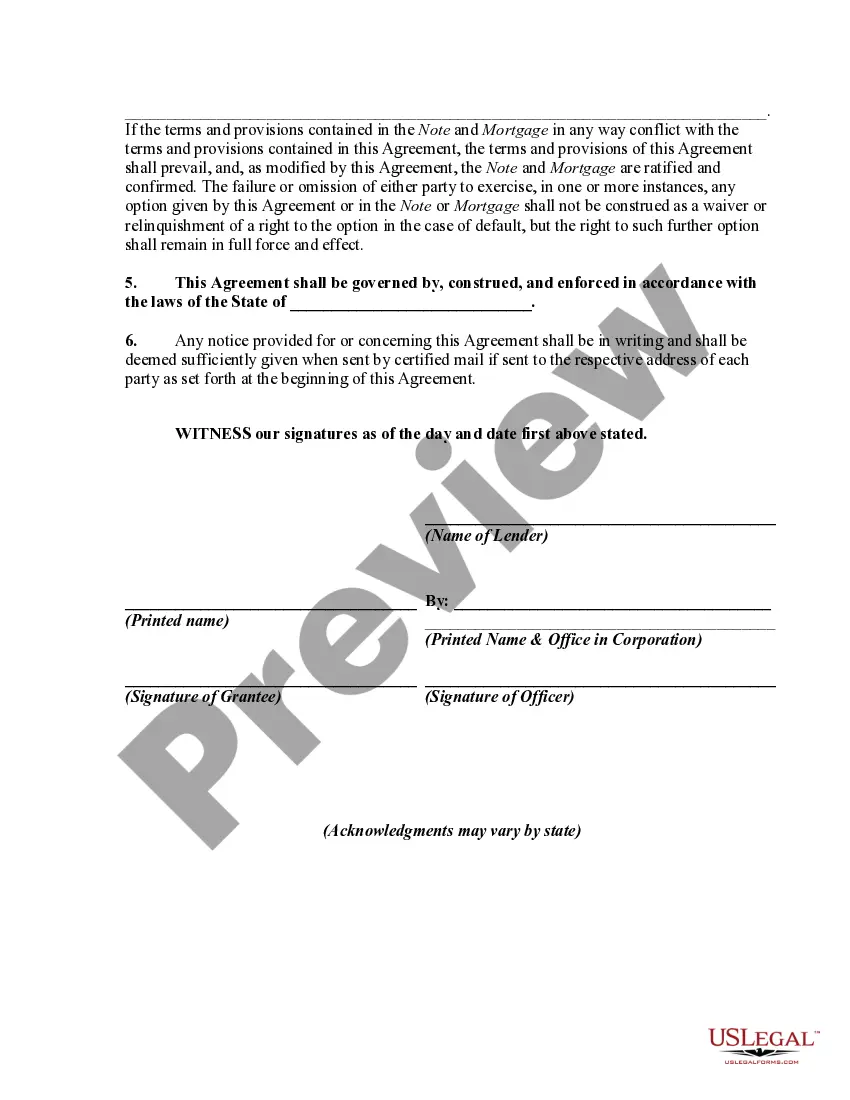

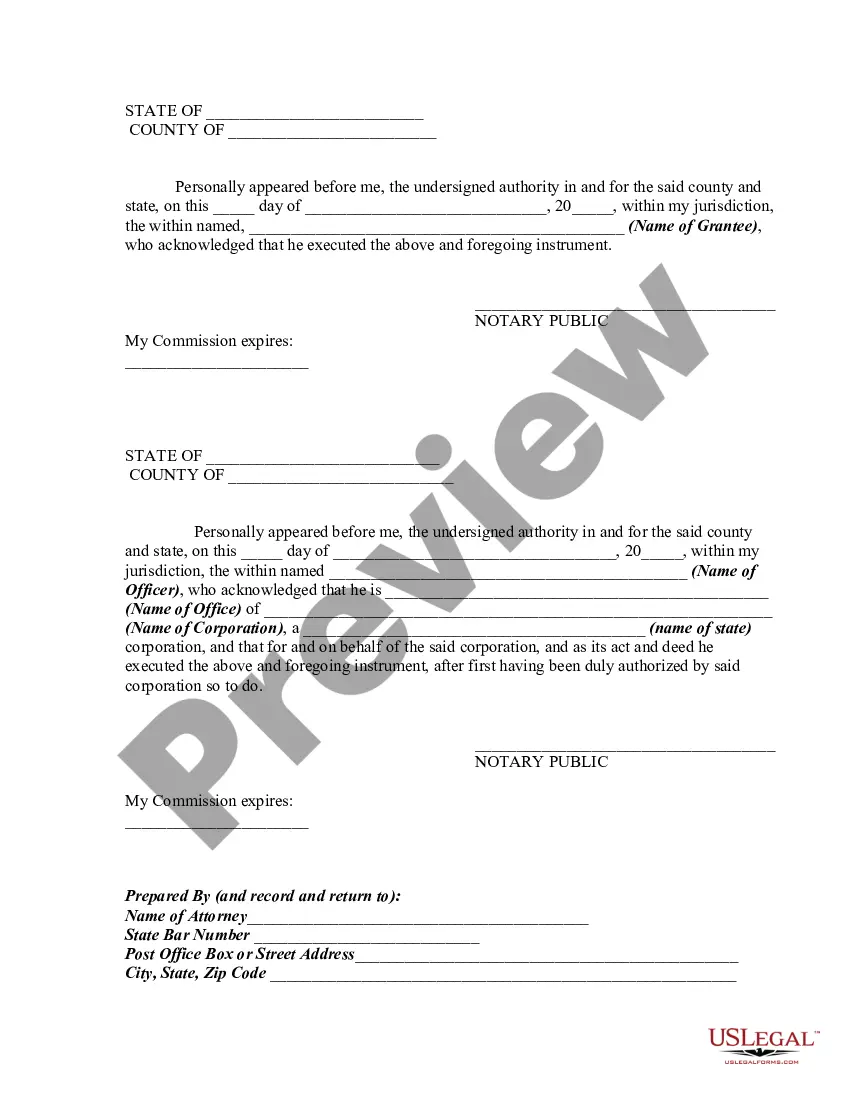

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. Such a modification or extension is contractual in nature and must be supported by consideration. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Keywords: North Carolina mortgage extension agreement, assumption of debt, new owner, real property, increase of interest. Detailed description: A North Carolina Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest refers to a legal contract that allows the transfer of an existing mortgage obligation to a new owner of a property located in North Carolina, while also providing provisions for an extension of the mortgage term and an increase in the interest rate. This agreement is commonly used when a property owner wants to sell their property, but the prospective buyer is unable or unwilling to secure a new mortgage to pay off the existing loan in full. Instead of obtaining a new mortgage, the buyer can assume the existing mortgage and enter into an agreement with the lender to extend the mortgage term and modify the interest rate. The primary purpose of this agreement is to facilitate the transfer of ownership while ensuring that the lender is protected and the terms of the mortgage are properly adjusted. It is crucial to note that the lender's consent is required for such an agreement, as they need to approve the new buyer's creditworthiness and assess the risks associated with the assumptions, extension, and changes in interest rate. There may be different variations of the North Carolina Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest, depending on the specific terms and conditions agreed upon by the parties involved. Some variations may include: 1. Fixed-Rate Extension Agreement: This type of agreement involves extending the mortgage term with a fixed interest rate for a specified period. Both the existing and new owner agree on the terms, ensuring stability throughout the extended period. 2. Adjustable-Rate Extension Agreement: The extension of the mortgage term occurs with an adjustable interest rate. The interest rate may be subject to periodic adjustments based on predefined market indices, resulting in potential fluctuations in the monthly mortgage payments. 3. Balloon-Payment Extension Agreement: This type of agreement involves the extension of the mortgage term, but with a substantial final payment, known as the balloon payment. The balloon payment is due at the end of the extended term, requiring careful financial planning by the new owner to fulfill the obligation. These are just a few examples of the potential variations of the North Carolina Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest. It is crucial for both parties to carefully review and negotiate the agreement, ensuring all terms are clearly specified and understood before signing. As with any legal document, it is recommended to seek professional advice from a qualified attorney to navigate the complexities of the agreement and ensure compliance with North Carolina laws and regulations.