This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

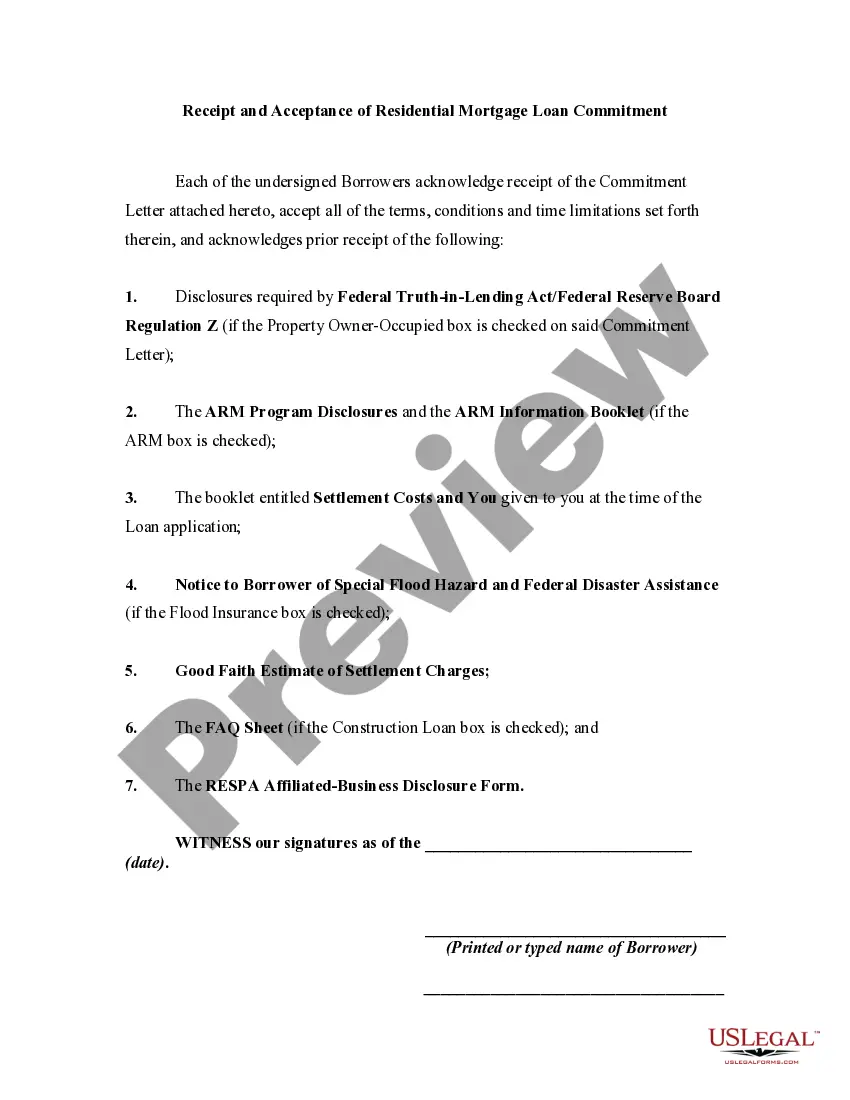

North Carolina Receipt and Acceptance of Residential Mortgage Loan Commitment is a legal document designed to acknowledge the borrower's receipt and acceptance of a mortgage loan commitment for a residential property in the state of North Carolina. This agreement demonstrates the borrower's intent to proceed with the mortgage transaction and acknowledges their understanding of the terms and conditions outlined in the commitment. The North Carolina Receipt and Acceptance of Residential Mortgage Loan Commitment form typically includes various key details such as the borrower's name, address, and contact information, the property address, loan amount, interest rate, loan term, and any specific conditions or contingencies associated with the loan commitment. It is important for the borrower to carefully review and understand all the terms before signing this document. In North Carolina, there may be different types of Receipt and Acceptance of Residential Mortgage Loan Commitment forms depending on the loan program or specific lender requirements. Some potential variations may include: 1. Conventional Loan Receipt and Acceptance: This form is applicable for borrowers seeking a conventional mortgage loan from a traditional lending institution such as a bank or credit union. It would outline the specific terms and conditions for such a loan. 2. Federal Housing Administration (FHA) Loan Receipt and Acceptance: This variation pertains to borrowers receiving a mortgage loan insured by the Federal Housing Administration. FHA loans often have different qualification criteria and additional guidelines compared to conventional loans. 3. Veterans Affairs (VA) Loan Receipt and Acceptance: This specific form is relevant for borrowers who are eligible for a VA loan program, which is offered to qualified veterans, active-duty service members, and surviving spouses. VA loans have unique requirements and benefits tailored to members of the military community. It is crucial for borrowers to consult with their lender or mortgage professional to ensure they are using the correct receipt and acceptance form based on the specific loan type and program they are applying for. This document plays a crucial role in formalizing the borrower's agreement to proceed with the mortgage loan commitment and signifies their acceptance of the terms and conditions set forth by the lender.