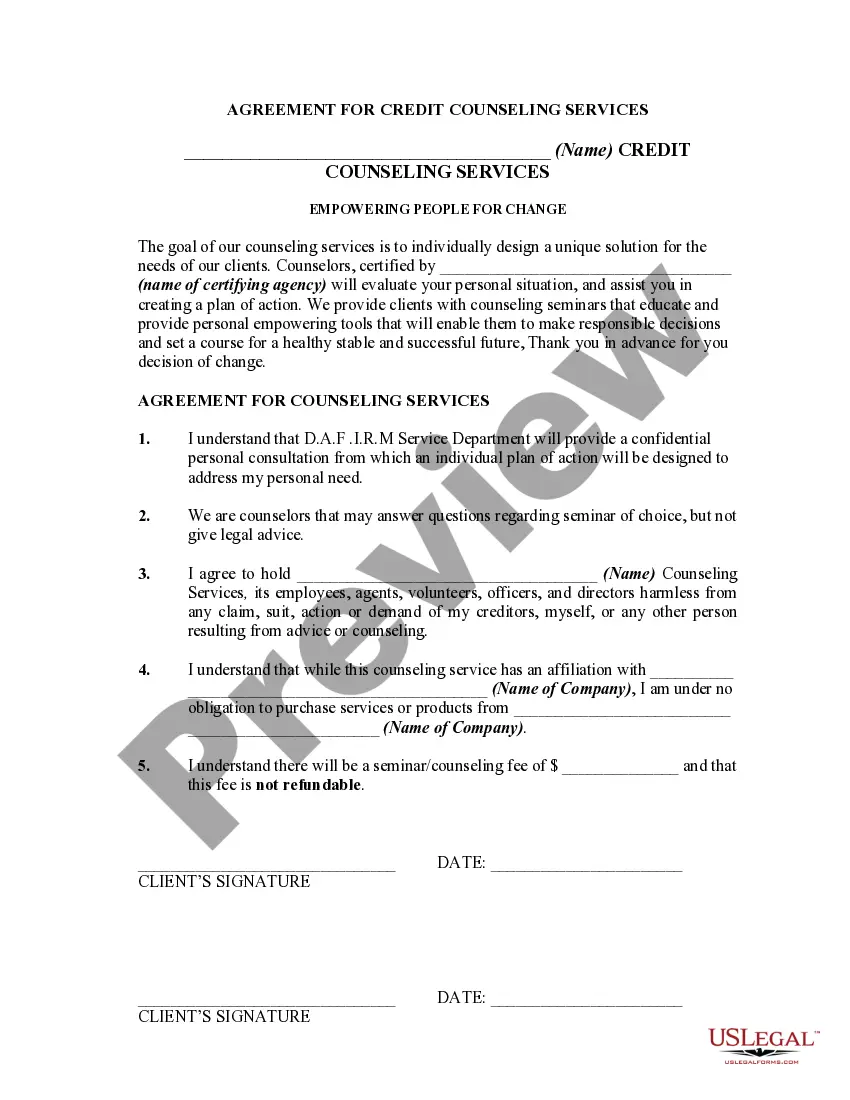

This type of form may be used in connection with a credit counseling seminar which also includes individual credit counseling. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The North Carolina Agreement for Credit Counseling Services is a legal document designed to outline the terms and conditions between a credit counseling organization and a consumer seeking financial assistance and guidance. This agreement serves as a binding contract that ensures both parties understand their rights, responsibilities, and obligations throughout the credit counseling process. In North Carolina, there are various types of agreements for credit counseling services available, each catering to specific needs and circumstances. These may include: 1. Debt Management Plans (Dumps): This type of agreement focuses on helping individuals struggling with overwhelming debt by providing a structured repayment plan. The credit counseling organization negotiates with creditors to obtain reduced interest rates and fees, creating an affordable monthly payment plan for the consumer. 2. Budgeting and Financial Education: Some credit counseling services emphasize comprehensive financial education and budgeting assistance. The agreement may include provisions for creating personalized budgets, exploring effective saving strategies, incorporating wise debt management practices, and educating consumers on proper money management. 3. Credit Report Analysis and Dispute Assistance: Another type of agreement may focus on credit report analysis and offering guidance on addressing inaccuracies or disputes. This service helps consumers understand their credit reports, identify potential errors, and provides assistance on resolving issues that negatively impact their creditworthiness. 4. Housing Counseling: Certain credit counseling organizations specialize in housing counseling, guiding consumers through the complex process of homeownership, rental assistance, or foreclosure prevention. This agreement may include components such as pre-purchase workshops, post-purchase counseling, rental counseling, and foreclosure intervention. 5. Bankruptcy Counseling: For individuals considering bankruptcy, some credit counseling agencies offer specific services in compliance with North Carolina bankruptcy regulations. These agreements require the credit counseling organization to provide mandatory counseling and debtor education services, ensuring consumers are well-informed about the consequences and alternatives to bankruptcy. Regardless of the specific type of agreement for credit counseling services, it is essential for both the consumer and the credit counseling organization to carefully review and understand its content. Key provisions typically include the scope of services provided, fee structure (if applicable), confidentiality, termination circumstances, rights and responsibilities of each party, dispute resolution procedures, and compliance with applicable state and federal laws. By establishing a comprehensive and transparent North Carolina Agreement for Credit Counseling Services, consumers can confidently seek professional assistance while credit counseling organizations can operate ethically, promoting long-term financial stability and well-being.