A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

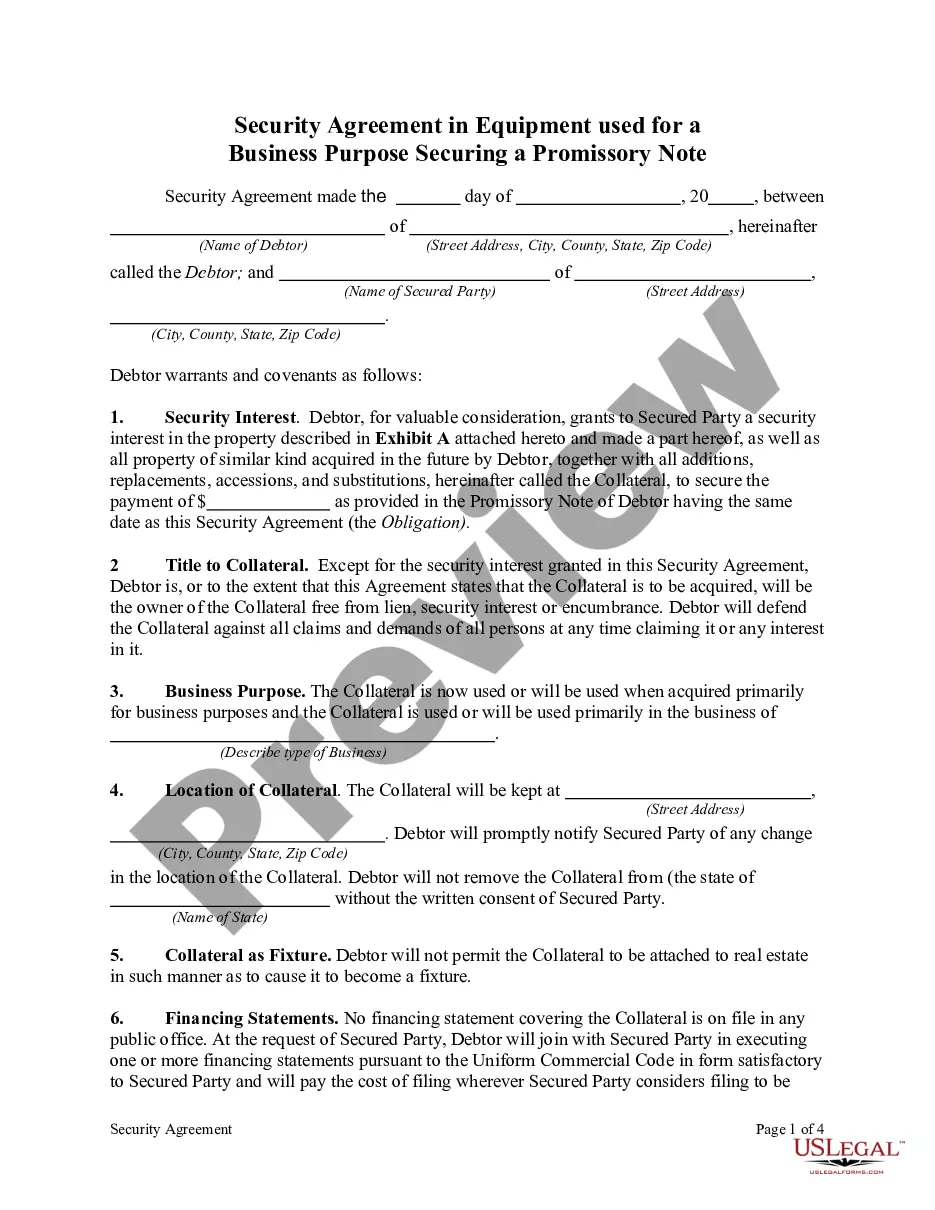

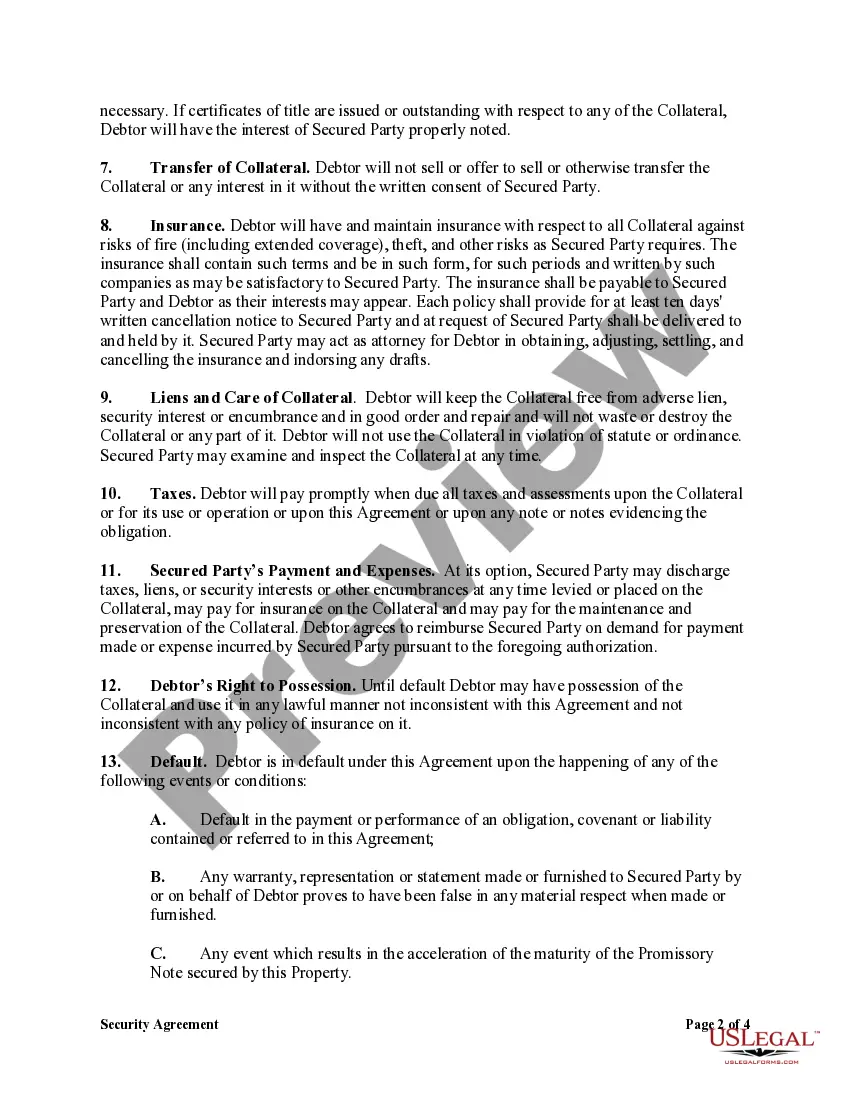

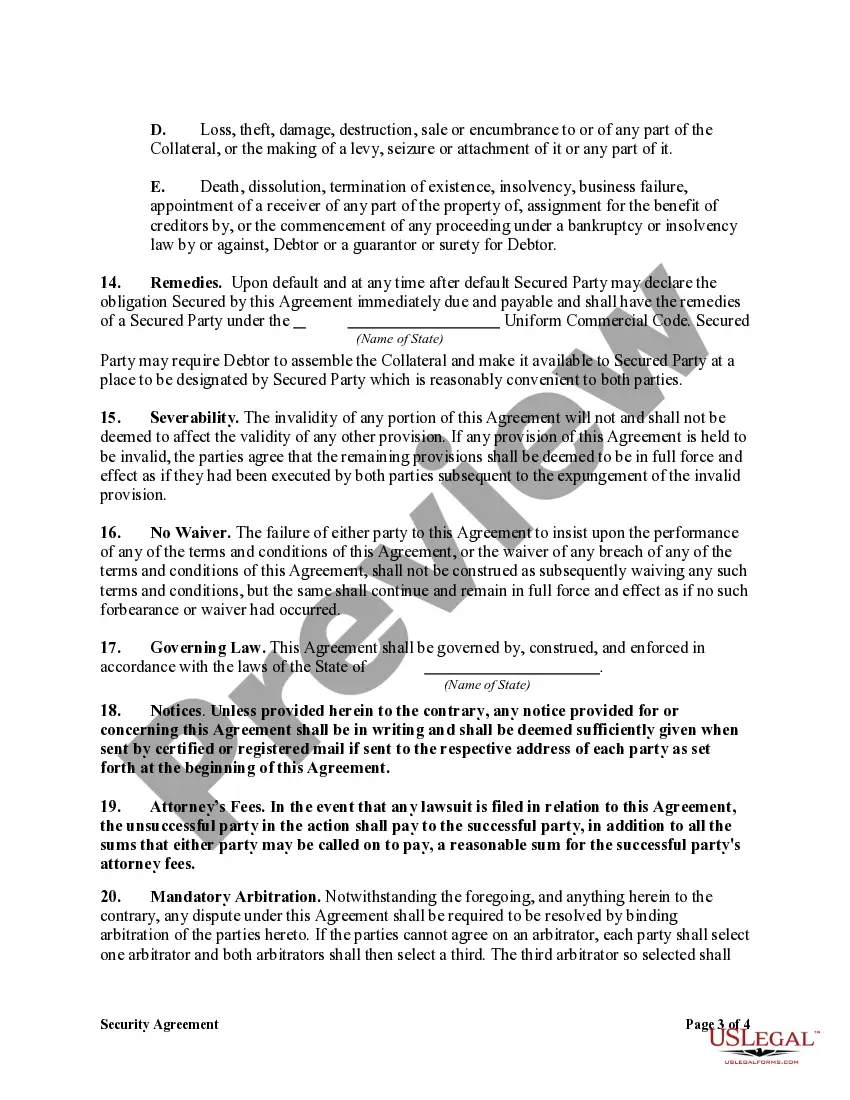

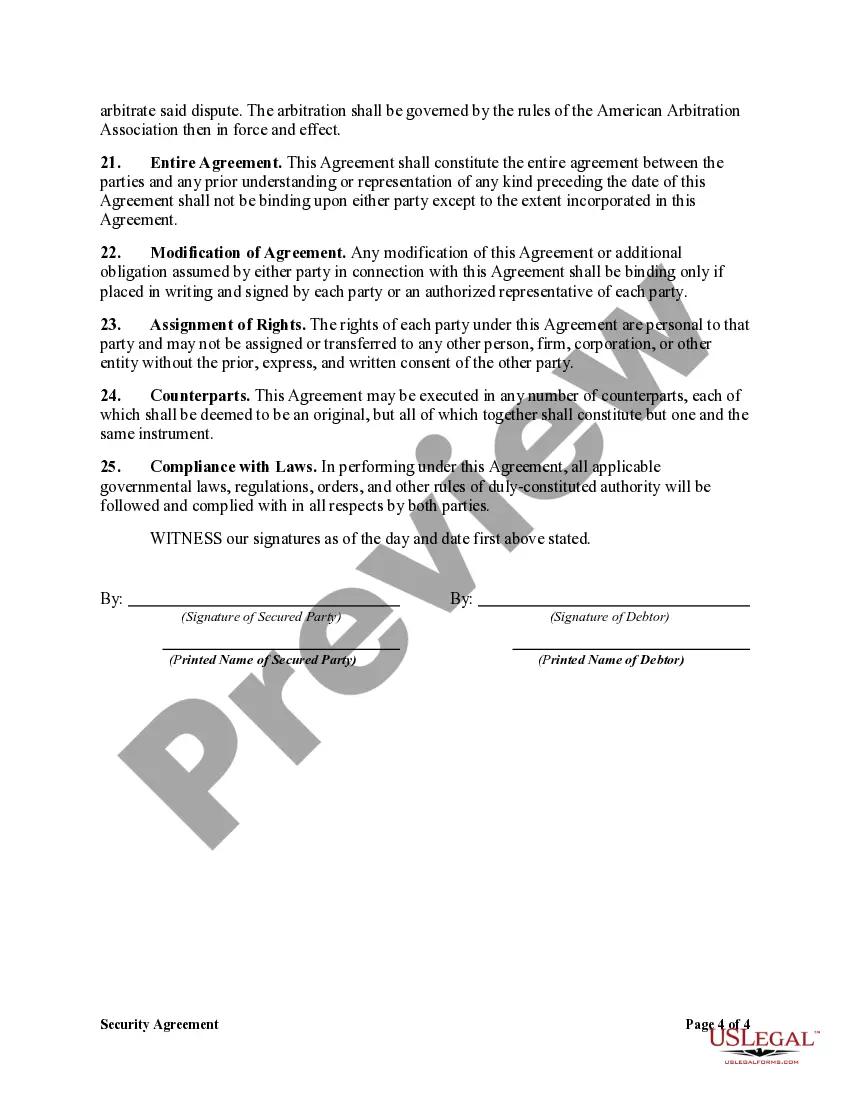

North Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that provides protection to lenders in the state of North Carolina when providing a loan for the purchase of equipment for business purposes. This agreement ensures that the lender has a security interest in the equipment to secure the repayment of the promissory note, minimizing the risk of default for the lender. The North Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note outlines the terms and conditions under which the equipment will be used as collateral for the loan. It includes detailed information about the equipment, such as its make, model, and serial number, to ensure proper identification and attachment of the security interest. The agreement establishes the rights and obligations of both the lender and the borrower. The lender is granted the right to repossess the equipment in the event of default, with the option to sell it to recover any outstanding amounts owed on the promissory note. The borrower, on the other hand, is responsible for maintaining the equipment in good condition and providing insurance coverage for its protection. There are different types of North Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note that vary based on the specific circumstances or requirements of the parties involved. Some common variants may include: 1. Fixed Security Agreement: This type of agreement is used when the equipment being financed is predetermined and does not change throughout the loan term. The lender has a security interest in the specified equipment and does not need to be updated if new purchases are made. 2. Floating Security Agreement: In contrast to the fixed security agreement, a floating security agreement allows the borrower to continually add new equipment to the loan collateral, subject to the lender's approval. This type of agreement is beneficial for businesses that frequently acquire new equipment. 3. Specific Equipment Security Agreement: This agreement is used when the lender and borrower agree to secure a specific piece of equipment as collateral for the loan. The equipment is described in detail within the agreement, including its value, condition, and location. 4. Purchase Money Security Agreement: This type of agreement is entered into when the lender provides financing specifically for the purchase of equipment. The lender's security interest is created at the time of purchase, ensuring that the loan is directly tied to the equipment being financed. In summary, a North Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a crucial legal document that safeguards the interests of lenders when providing loans for the acquisition of equipment. By establishing a security interest in the equipment, lenders can have confidence that their investment is protected and can seek legal remedies in the event of default. The agreement can take different forms depending on the specific circumstances, making it essential for both parties to engage in thorough negotiations and create an agreement that meets their needs.North Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that provides protection to lenders in the state of North Carolina when providing a loan for the purchase of equipment for business purposes. This agreement ensures that the lender has a security interest in the equipment to secure the repayment of the promissory note, minimizing the risk of default for the lender. The North Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note outlines the terms and conditions under which the equipment will be used as collateral for the loan. It includes detailed information about the equipment, such as its make, model, and serial number, to ensure proper identification and attachment of the security interest. The agreement establishes the rights and obligations of both the lender and the borrower. The lender is granted the right to repossess the equipment in the event of default, with the option to sell it to recover any outstanding amounts owed on the promissory note. The borrower, on the other hand, is responsible for maintaining the equipment in good condition and providing insurance coverage for its protection. There are different types of North Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note that vary based on the specific circumstances or requirements of the parties involved. Some common variants may include: 1. Fixed Security Agreement: This type of agreement is used when the equipment being financed is predetermined and does not change throughout the loan term. The lender has a security interest in the specified equipment and does not need to be updated if new purchases are made. 2. Floating Security Agreement: In contrast to the fixed security agreement, a floating security agreement allows the borrower to continually add new equipment to the loan collateral, subject to the lender's approval. This type of agreement is beneficial for businesses that frequently acquire new equipment. 3. Specific Equipment Security Agreement: This agreement is used when the lender and borrower agree to secure a specific piece of equipment as collateral for the loan. The equipment is described in detail within the agreement, including its value, condition, and location. 4. Purchase Money Security Agreement: This type of agreement is entered into when the lender provides financing specifically for the purchase of equipment. The lender's security interest is created at the time of purchase, ensuring that the loan is directly tied to the equipment being financed. In summary, a North Carolina Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a crucial legal document that safeguards the interests of lenders when providing loans for the acquisition of equipment. By establishing a security interest in the equipment, lenders can have confidence that their investment is protected and can seek legal remedies in the event of default. The agreement can take different forms depending on the specific circumstances, making it essential for both parties to engage in thorough negotiations and create an agreement that meets their needs.