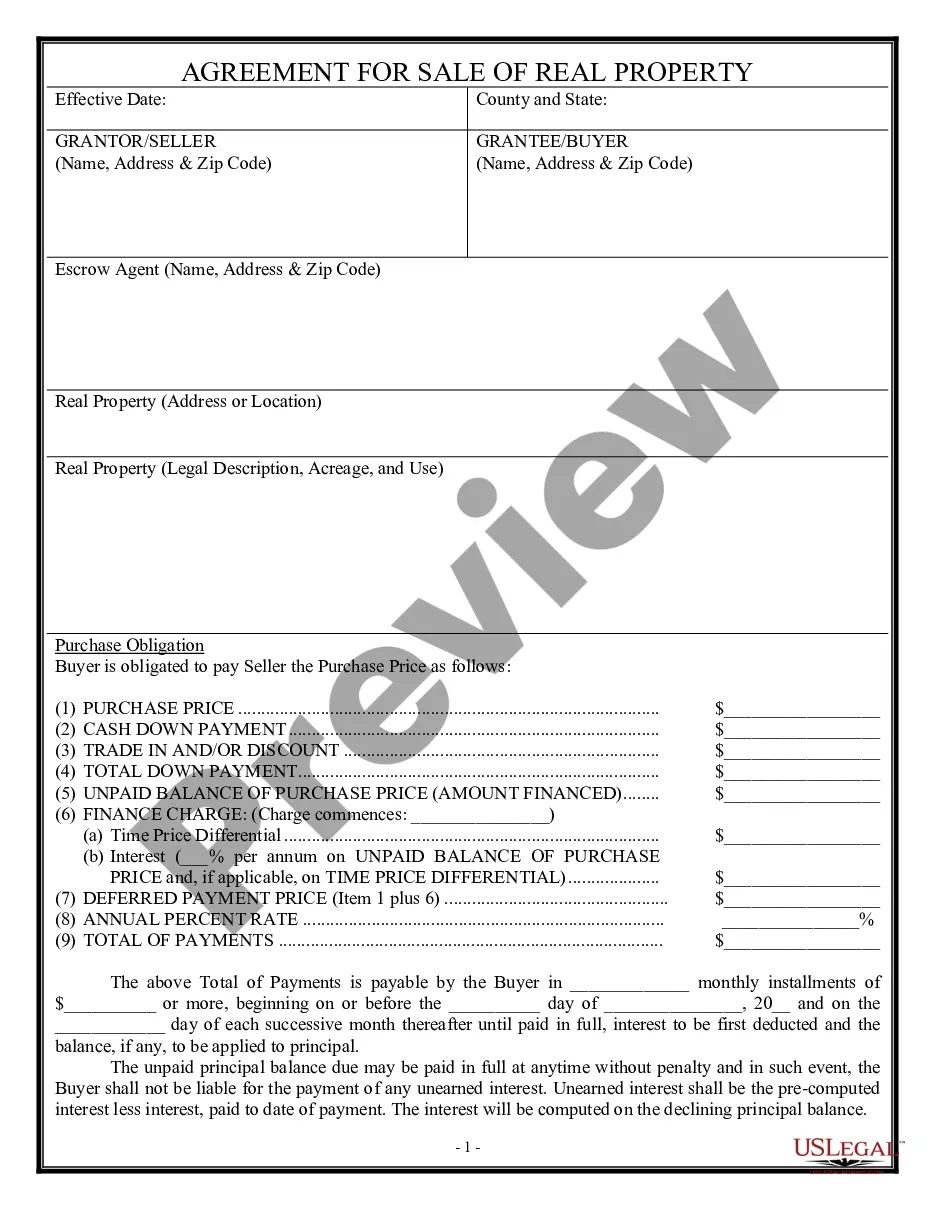

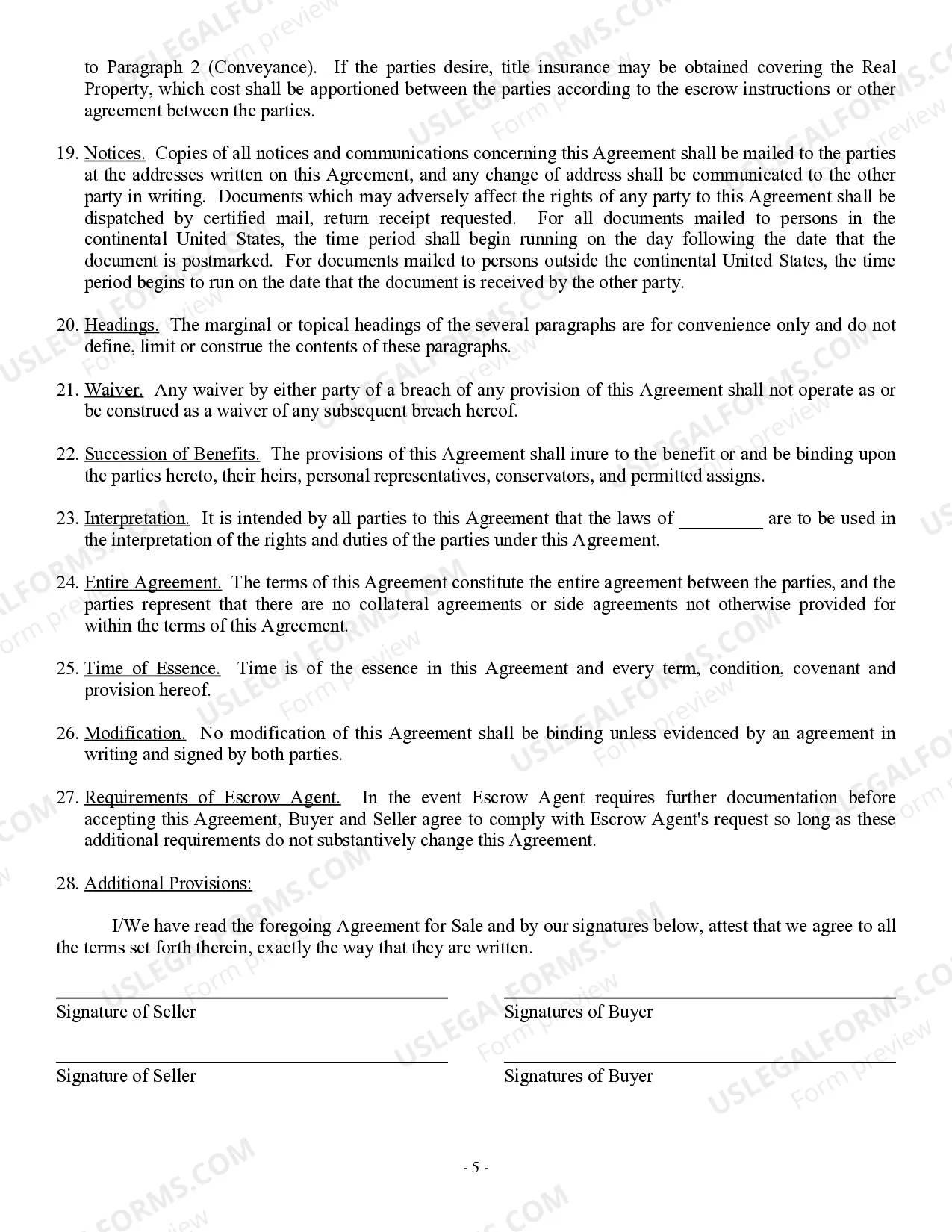

The North Carolina Agreement for Sale — Residential is a legal document used for property transactions within the state of North Carolina. It outlines the terms and conditions of the sale between the seller (also known as the "granter") and the buyer (also known as the "grantee"). This agreement serves as a crucial contract, ensuring a smooth transaction while protecting the rights and interests of both parties involved. The North Carolina Agreement for Sale — Residential typically includes relevant information such as the names and addresses of the buyer and seller, a detailed description of the property being sold, the agreed-upon purchase price, the payment terms, and any contingencies or conditions that need to be met prior to the completion of the sale. It may also include provisions for property inspections, appraisals, and financing arrangements. Different types of North Carolina Agreements for Sale — Residential may vary based on specific factors such as the inclusion of additional clauses, special stipulations, or unique terms tailored to the property and parties involved. Some common types and variations of the agreement include: 1. Standard Residential Purchase Agreement: This is the most commonly used form and covers the sale of a residential property between a buyer and a seller in North Carolina. It follows the standard format provided by the North Carolina Association of Realtors (NEAR) and is widely accepted by real estate professionals. 2. As-Is Residential Purchase Agreement: This agreement is specifically designed for the sale of a residential property in its current condition, without any warranties or guarantees from the seller regarding the condition of the property. It indicates that the buyer accepts the property in its current state and is responsible for any repairs or issues that may arise after the sale. 3. Lease Purchase Agreement: This type of agreement combines elements of both a lease and a sale. It allows a tenant to rent a property with the option to purchase it at a later date. The terms of the agreement specify the rental terms, the purchase price, and the period within which the tenant can exercise their option to buy. 4. Owner Financing Agreement: In cases where the seller provides the financing for the buyer instead of relying on a traditional mortgage, an owner financing agreement is used. This agreement outlines the terms of the loan, including the interest rate, monthly payments, and repayment schedule. It is important to note that while these types of agreements are commonly used, they can be modified or customized to suit the specific needs and requirements of the parties involved in the sale of a residential property in North Carolina. It is advisable for both buyers and sellers to seek legal counsel or consult with a real estate professional to ensure all necessary elements are included and all legal aspects are properly addressed.

North Carolina Agreement for Sale - Residential

Description

How to fill out North Carolina Agreement For Sale - Residential?

Choosing the best legitimate file format could be a battle. Of course, there are a variety of templates accessible on the Internet, but how can you obtain the legitimate kind you want? Utilize the US Legal Forms site. The services offers a large number of templates, like the North Carolina Agreement for Sale - Residential, which you can use for business and private requirements. All the types are inspected by pros and fulfill federal and state needs.

If you are currently listed, log in to the profile and then click the Download option to find the North Carolina Agreement for Sale - Residential. Make use of profile to appear with the legitimate types you might have acquired earlier. Visit the My Forms tab of the profile and get yet another backup in the file you want.

If you are a brand new consumer of US Legal Forms, allow me to share straightforward recommendations that you can stick to:

- Initially, make sure you have selected the correct kind for your town/area. You are able to check out the form utilizing the Review option and study the form outline to ensure this is basically the best for you.

- In case the kind fails to fulfill your preferences, use the Seach industry to obtain the right kind.

- Once you are certain that the form would work, click on the Purchase now option to find the kind.

- Opt for the pricing program you need and type in the necessary details. Make your profile and purchase the order making use of your PayPal profile or credit card.

- Pick the file formatting and acquire the legitimate file format to the gadget.

- Complete, edit and print out and indication the acquired North Carolina Agreement for Sale - Residential.

US Legal Forms is definitely the greatest collection of legitimate types for which you will find different file templates. Utilize the service to acquire professionally-produced papers that stick to status needs.