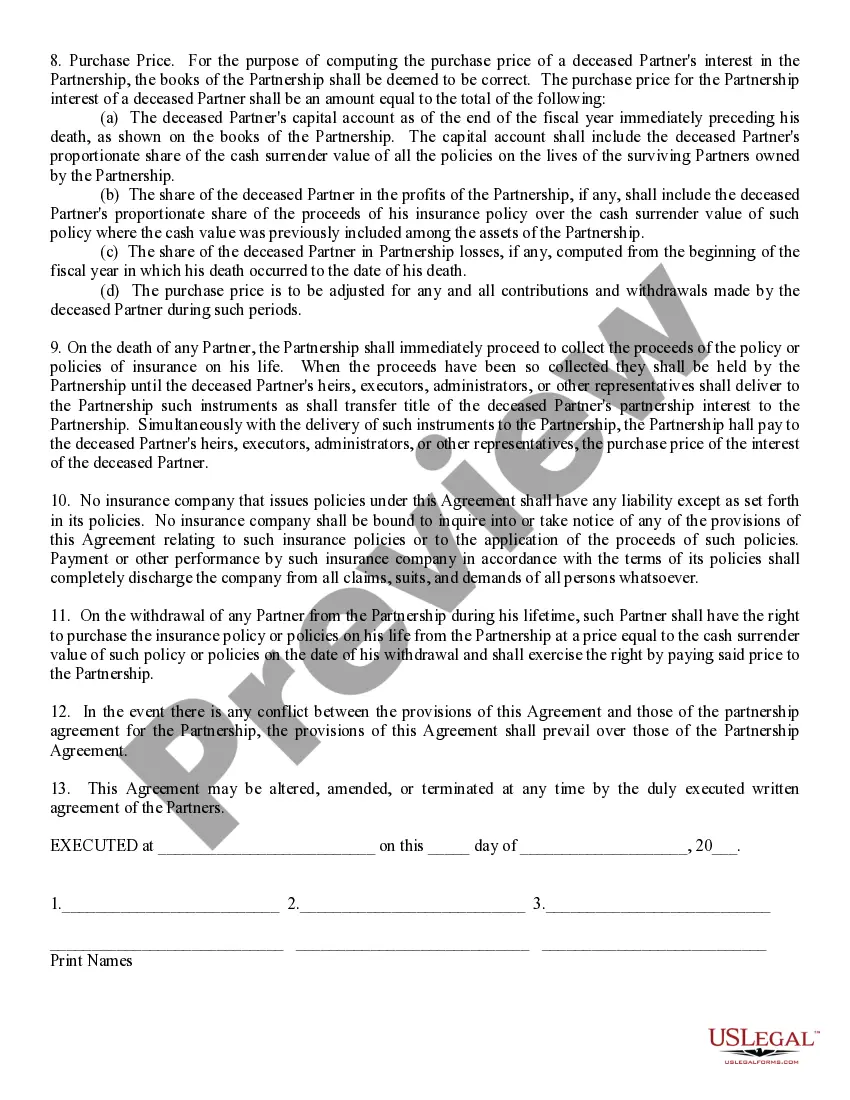

When a partner unfortunately passes away in North Carolina, the Sale of Deceased Partner's Interest becomes a crucial legal process in order to facilitate the smooth transfer of assets and ownership within the partnership. The deceased partner's interest in the business must be handled carefully to ensure the fair distribution of assets, protect the rights of the surviving partners, and provide for the deceased partner's estate. In North Carolina, there are two distinct types of Sale of Deceased Partner's Interest that can occur: voluntary sale and involuntary sale. Let's explore each type in more detail. Voluntary Sale of Deceased Partner's Interest: In this scenario, the deceased partner's interest can be willingly sold by the estate representatives or heirs of the deceased partner. It involves reaching an agreement between the surviving partners and the estate representatives regarding the fair value of the deceased partner's interest. The process typically includes various legal steps, such as appraising the value of the interest, negotiating fair terms, and finalizing the sale contract. Voluntary sales often aim to maintain a positive relationship among surviving partners and the estate, while ensuring a reasonable price for the deceased partner's share. Involuntary Sale of Deceased Partner's Interest: When the surviving partners and the estate representatives cannot reach an agreement on the sale of the deceased partner's interest, an involuntary sale may be initiated. In this situation, North Carolina law provides a legal mechanism called a "Judicial Sale." A Judicial Sale involves the court's intervention to determine the fair value of the deceased partner's interest and enforce the sale. The court-appointed appraiser assesses the value, allowing for a fair distribution of assets. It is essential to note that the North Carolina Revised Uniform Partnership Act (RPA) governs the Sale of Deceased Partner's Interest, conferring specific rights and obligations upon all parties involved. All relevant legal documents, such as partnership agreements, wills, and estate plans, are taken into consideration during the process to ensure compliance with the law and respect the wishes of the deceased partner. In summary, the North Carolina Sale of Deceased Partner's Interest is a legally significant process that necessitates careful consideration, negotiation, and potential judicial involvement. Whether it is a voluntary sale or an involuntary sale, the objective is to equitably distribute the deceased partner's interest among the surviving partners and the estate while adhering to the provisions set forth by the North Carolina RPA.

North Carolina Sale of Deceased Partner's Interest

Description

How to fill out North Carolina Sale Of Deceased Partner's Interest?

Selecting the appropriate legal document format can be challenging.

It goes without saying that there are countless templates accessible online, but how will you find the legal document you need.

Utilize the US Legal Forms website. The service offers thousands of templates, such as the North Carolina Sale of Deceased Partner's Interest, suitable for business and personal purposes.

You can browse the form using the Review button and read the form description to confirm it is the right one for you.

- All templates are reviewed by experts and comply with both federal and state regulations.

- If you are already registered, Log In to your account and click the Download button to obtain the North Carolina Sale of Deceased Partner's Interest.

- Use your account to search for the legal documents you have previously purchased.

- Navigate to the My documents section of your account and retrieve another copy of the document you need.

- If you are a new user of US Legal Forms, here are straightforward steps you should follow.

- First, ensure you have chosen the correct template for your city/state.

Form popularity

FAQ

Under the purchase scenario, one or more remaining partners may buy out the terminating partner's interest for fair market value (FMV) plus any relief of debt realized by the partner.

The business partnership offers a lot of advantages to those who choose to use it.1 Less formal with fewer legal obligations.2 Easy to get started.3 Sharing the burden.4 Access to knowledge, skills, experience and contacts.5 Better decision-making.6 Privacy.7 Ownership and control are combined.More items...?27-Aug-2017

The North Carolina Secretary of State's Office asks business owners to declare their Articles of Dissolution by mail or online. A person must select the Online Filing box under Submit a Filing with an Existing Entity for their business and click Upload a PDF Filing..

Understanding General Partnership Advantages and DisadvantagesAdvantage: Easy to Create.Disadvantage: Easy to Dissolve.Advantage: Flow of Personal Income.Disadvantage: Little Protection.Advantage: Flexibility.Disadvantages: Lack of Structure.

Other advantages of a general partnership are that the partners can combine resources and share the financial commitment. There are disadvantages to general partnerships, principally liability. General partners are personally liable for the business debts and liabilities.

A sale of a partnership interest occurs when one partner sells their ownership interest to another person or entity. The partnership is generally not involved in the transaction. However, the buyer and seller will notify the partnership of the transaction.

If your business is a limited liability company or general partnership, your partner can't sell the company without your consent. He may, however, sell his interest in the company if you don't have a buy-sell agreement.

1. Reduction in liability for other people's actions. 2. Same advantages found in general partnership re; sharing management duties (allowed to manage, not just invest), ability to raise capital by adding new partners.

Partnerships are generally guided by a partnership agreement, which may allow or restrict transfers of partnership interest. Partners must follow the terms of the agreement. If the agreement allows it, a partner can transfer ownership stakes in terms of profits, voting rights and responsibilities.

Your legal partnership is essentially a single legal entity, and the situation can become complicated when one partner wants to sell his or her shares and the other partner refuses. Whether or not you can force your business partner to buy you out largely depends on your written agreement.

Interesting Questions

More info

Tax Return Apply a Tax File.