This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

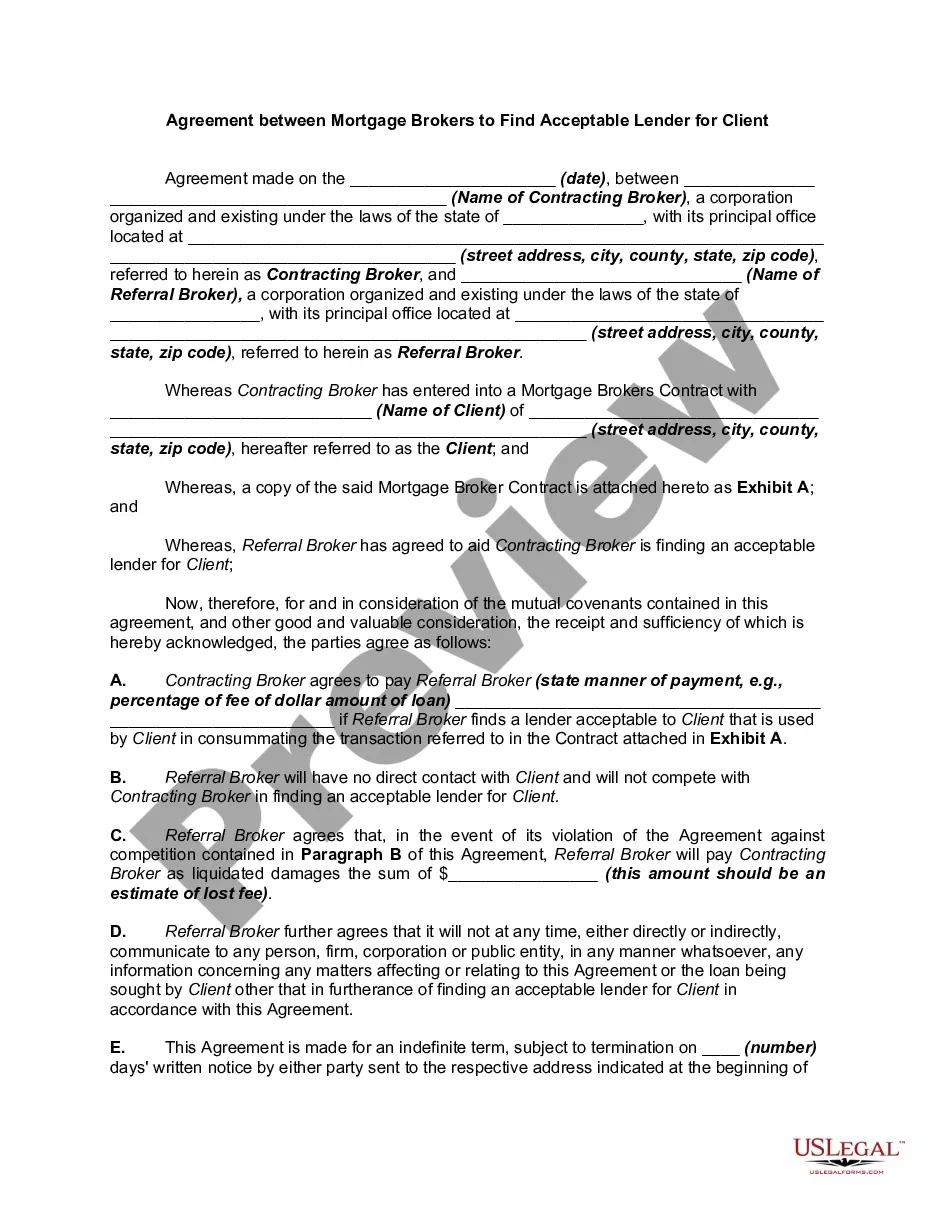

A North Carolina Agreement between Mortgage Brokers to Find an Acceptable Lender for a Client is a legally binding contract that outlines the terms and conditions agreed upon by multiple mortgage brokers to collaborate and identify a suitable lender for a client's mortgage needs within the state of North Carolina. This agreement is crucial in ensuring transparency, the protection of the client's interests, and the smooth facilitation of the mortgage application process. Here are some relevant keywords to include in the content: 1. North Carolina: As the agreement specifically pertains to the state of North Carolina, it is essential to mention this location to highlight the regional context and legal applicability. 2. Agreement: This term signifies the legally binding nature of the contract and the mutual understanding reached among the participating mortgage brokers. 3. Mortgage Brokers: These professionals act as intermediaries between borrowers and lenders, helping clients find the best mortgage options available to them. They play a pivotal role in guiding borrowers through the complex mortgage market. 4. Acceptable Lender: This phrase emphasizes the objective of the agreement — to identify a lender that meets the client's requirements and provides suitable mortgage terms and conditions. 5. Client: Refers to the individual or entity seeking mortgage financing. The client's interests, needs, and preferences are the primary focus of the agreement. Different types of North Carolina Agreement between Mortgage Brokers to Find Acceptable Lender for Client could include: 1. Exclusive Referral Agreement: This type of agreement limits the collaborating brokers to refer the client only to a specific list of lenders with whom they have a pre-established working relationship. 2. Multiple Broker Collaboration Agreement: In this scenario, several mortgage brokers join forces to collectively identify and evaluate potential lenders for the client. This approach allows for a wider range of options and expertise. 3. Fee-Sharing Agreement: Some agreements include provisions for the sharing of fees or commissions earned by the collaborative brokers after the client's mortgage has been successfully facilitated. This incentivizes brokers to work together efficiently and effectively. 4. Non-Disclosure Agreement: To ensure the confidentiality of sensitive client information, a non-disclosure agreement may be included in the broader agreement. This helps protect the client's privacy throughout the mortgage application process. Remember, it is crucial to consult legal professionals and comply with the specific laws and regulations of North Carolina when drafting and entering into such agreements.