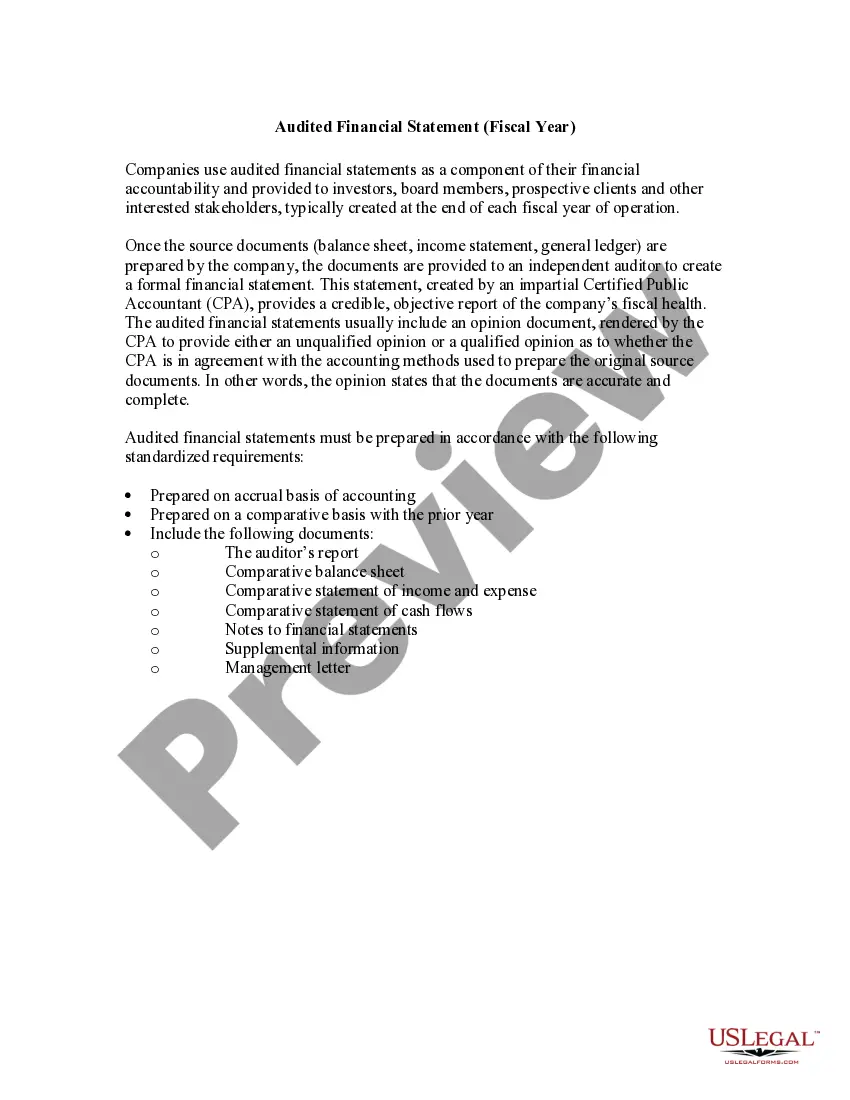

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

North Carolina Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

If you need to compile, download, or create legal document templates, utilize US Legal Forms, the most extensive collection of legal forms available online.

Leverage the site's straightforward and convenient search feature to obtain the documents you need. Various templates for business and personal use are organized by categories and jurisdictions, or keywords.

Use US Legal Forms to access the North Carolina Report of Independent Accountants following the Audit of Financial Statements in just a few clicks.

Every legal document template you acquire is yours permanently. You have access to all forms you downloaded in your account. Click the My documents section and select a document to print or download again.

Be proactive and download, and print the North Carolina Report of Independent Accountants after the Audit of Financial Statements with US Legal Forms. There are millions of professional and state-specific forms available for your business or personal use.

- If you are already a US Legal Forms user, Log In to your account and click the Acquire button to locate the North Carolina Report of Independent Accountants post-Audit of Financial Statements.

- You can also find forms you have previously downloaded in the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have selected the form relevant to your city/state.

- Step 2. Use the Review option to examine the contents of the form. Don’t forget to check the details.

- Step 3. If you are dissatisfied with the document, use the Search field at the top of the page to find alternative versions of the legal document template.

- Step 4. Once you have located the necessary form, click the Purchase now button. Choose your preferred pricing plan and provide your details to register for an account.

- Step 5. Process the transaction. You can use your credit card or PayPal account to complete the payment.

- Step 6. Choose the format of the legal document and download it to your device.

- Step 7. Complete, review, and print or sign the North Carolina Report of Independent Accountants after the Audit of Financial Statements.

Form popularity

FAQ

An independent audit report provides a professional opinion on the financial statements based on an objective assessment. A statutory audit report, on the other hand, refers to audits conducted to comply with legal mandates, which may have specific requirements. In both cases, the North Carolina Report of Independent Accountants after Audit of Financial Statements highlights the importance of compliance and transparency in financial reporting.

Yes, audited financial statements are often considered public information, especially when the entity is publicly traded or required by law to disclose such documents. These statements can be accessed through various channels, including corporate websites and public registries. The North Carolina Report of Independent Accountants after Audit of Financial Statements is typically made available to ensure stakeholders have the required information for evaluation.

An independent audit report is a formal document that communicates the results of the audit process, detailing the auditor's opinions on the fairness of the financial statements. This report serves as a crucial tool for investors, regulators, and other stakeholders. The North Carolina Report of Independent Accountants after Audit of Financial Statements is a key example of such a report, providing transparency and reliability concerning financial affairs.

An independent CPA becomes associated with financial statements when they conduct an audit or review of those statements. Their involvement provides credibility to the financial reporting, which is crucial for stakeholders. The North Carolina Report of Independent Accountants after Audit of Financial Statements reflects this association, highlighting the level of scrutiny applied to the financial data.

Auditing generally refers to the examination of financial records and processes, which can be conducted by internal staff or external parties. Independent auditing specifically involves third-party auditors who are not affiliated with the organization, ensuring objectivity. The North Carolina Report of Independent Accountants after Audit of Financial Statements underscores this independence, offering an unbiased view of the financial health of the organization.

The primary function of an independent audit is to provide an objective assessment of a company’s financial statements. This process ensures that the financial records reflect the true financial position of the entity. By obtaining a North Carolina Report of Independent Accountants after Audit of Financial Statements, stakeholders gain confidence in the reported figures, which is vital for informed decision-making.

An unmodified audit report indicates that the financial statements are presented fairly, in all material respects, according to the applicable financial reporting framework. This positive outcome is essential for stakeholders who rely on the North Carolina Report of Independent Accountants after Audit of Financial Statements. It provides assurance that the audit process has been conducted with integrity and thoroughness.

To complete an audit report, you must first gather financial statements, relevant documentation, and conduct thorough testing of transactions. After assessing the findings, you will draft the report, ensuring it outlines your opinions in line with the North Carolina Report of Independent Accountants after Audit of Financial Statements requirements. Accuracy and clarity are essential, so reviewing the report for compliance and understanding is crucial. If you seek a streamlined process or templates to ease your workload, consider UsLegalForms as a reliable partner.

The North Carolina Report of Independent Accountants after Audit of Financial Statements typically includes an introductory paragraph, management's responsibility, auditor's responsibility, the audit opinion, and other required disclosures. Each section plays a critical role in ensuring that stakeholders understand the audit process and findings. By clearly outlining these components, the report promotes transparency and trust in financial reporting. If you need help preparing or reviewing your audit report, UsLegalForms offers valuable resources to assist you.

Yes, a CPA can prepare personal financial statements for individuals, providing a clear picture of personal finances. This service can help clients understand their financial position and make informed decisions. While the North Carolina Report of Independent Accountants after Audit of Financial Statements focuses on organizational audits, personal financial statements prepared by a CPA can be equally beneficial for personal financial management.