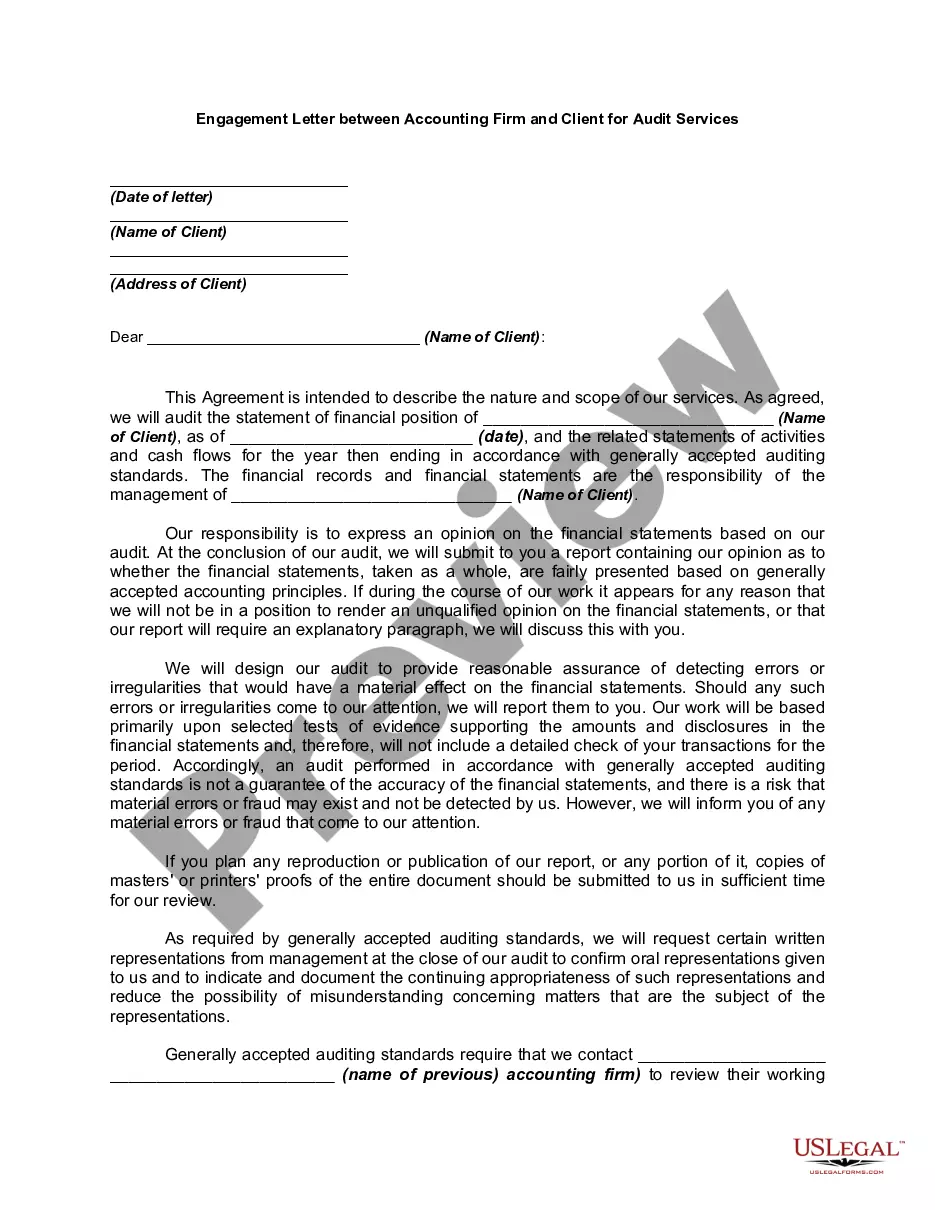

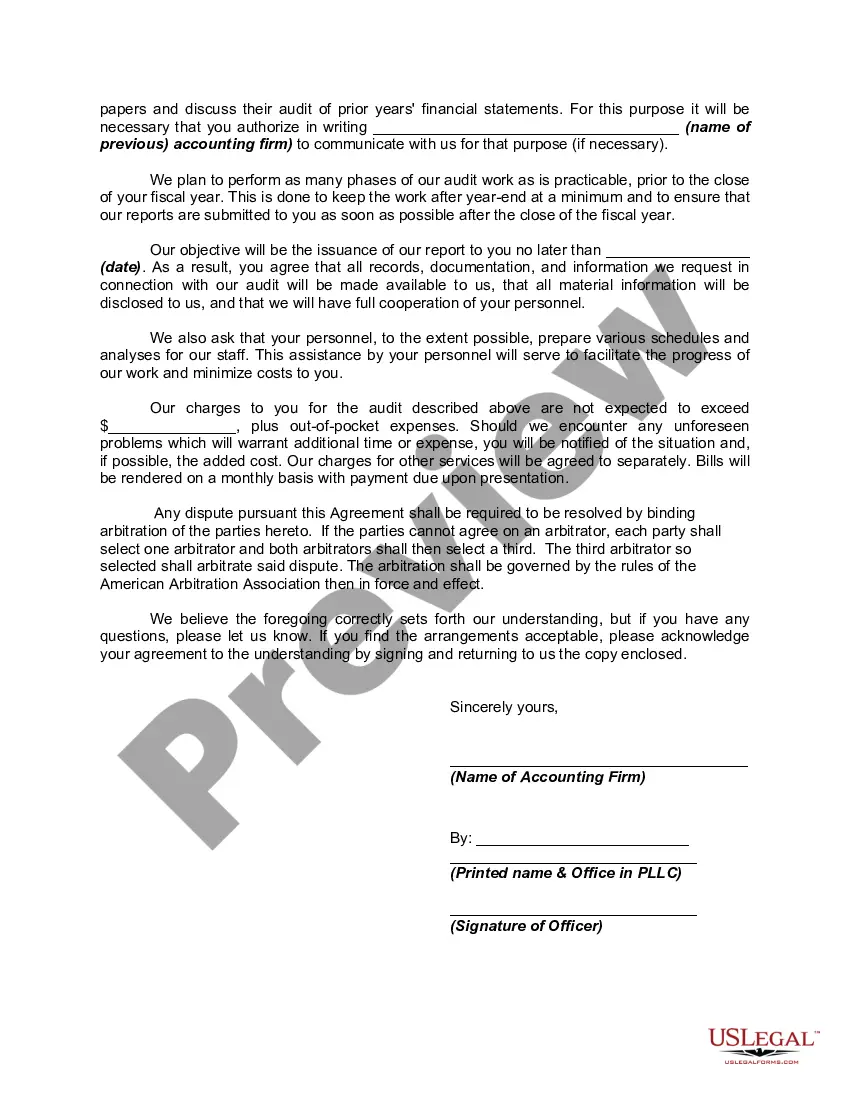

Generally, a contract to employ a certified public accountant need not be in writing. However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books.

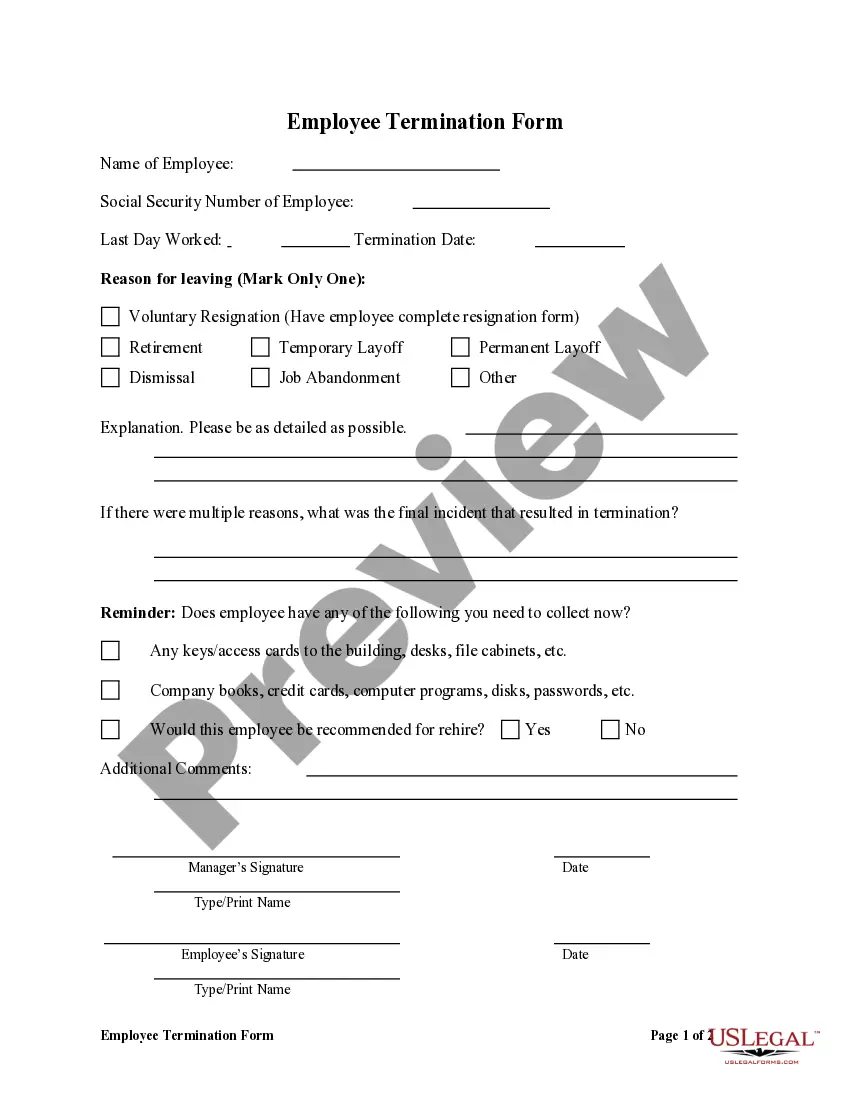

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Title: North Carolina Engagement Letter Between Accounting Firm and Client for Audit Services Introduction: An engagement letter acts as a formal agreement between an accounting firm and a client, outlining the terms and conditions of the audit services to be provided in North Carolina. This comprehensive description will explore various types of engagement letters specific to North Carolina and highlight the essential elements typically included within these documents. 1. Standard North Carolina Engagement Letter for Audit Services: The standard engagement letter for audit services in North Carolina is a comprehensive agreement that outlines the scope of work, responsibilities, and expectations between the accounting firm and the client. It details the specific services to be performed, such as financial statement audits, internal control assessments, and compliance with relevant regulations. 2. Limited Scope North Carolina Engagement Letter: A limited scope engagement letter is employed when the requested audit services are focused on specific areas, such as internal controls, revenue recognition, or inventory management. This specialized engagement letter allows the accounting firm and the client to define the restricted scope of work to attain specific audit objectives according to the client's needs. 3. Specialized North Carolina Engagement Letter for Government Entities: Government entities in North Carolina often require audits that adhere to specific regulatory guidelines. A specialized engagement letter for government entities ensures compliance with government regulations and highlights additional reporting requirements, such as Single Audit Act compliance or Government Auditing Standards (Yellow Book) procedures. 4. Non-Profit North Carolina Engagement Letter for Audit Services: Non-profit organizations in North Carolina may have unique audit requirements. This engagement letter highlights specific considerations for non-profit entities, such as adhering to Generally Accepted Auditing Standards (GAS), reviewing compliance with 501(c)(3) tax-exempt status, assessing potential risks associated with donor contributions, and proper financial reporting for grants. 5. North Carolina Engagement Letter for Internal Audit Services: Internal audit services provide clients with independent assessments of their internal controls, risk management systems, and operational efficiency. This type of engagement letter outlines the scope of the internal audit engagement, emphasizing the importance of objectivity, confidentiality, and professional judgment in conducting internal audit procedures. 6. Joint Venture North Carolina Engagement Letter: When two or more entities collaborate on a business venture in North Carolina, a joint venture engagement letter is used to outline mutual responsibilities, shared costs, and objectives of the audit engagement. This letter establishes the governance structure, financial reporting requirements, and the scope of the audit procedures applicable to the joint venture entity. Conclusion: North Carolina Engagement Letters between accounting firms and clients for audit services come in various types, tailored to specific audit scenarios and industry requirements. These formal agreements ensure a transparent understanding between the accounting firm and the client, allowing for a successful and productive audit engagement. It is essential for both parties to carefully review and agree upon the terms detailed in the engagement letter before commencing any audit services.Title: North Carolina Engagement Letter Between Accounting Firm and Client for Audit Services Introduction: An engagement letter acts as a formal agreement between an accounting firm and a client, outlining the terms and conditions of the audit services to be provided in North Carolina. This comprehensive description will explore various types of engagement letters specific to North Carolina and highlight the essential elements typically included within these documents. 1. Standard North Carolina Engagement Letter for Audit Services: The standard engagement letter for audit services in North Carolina is a comprehensive agreement that outlines the scope of work, responsibilities, and expectations between the accounting firm and the client. It details the specific services to be performed, such as financial statement audits, internal control assessments, and compliance with relevant regulations. 2. Limited Scope North Carolina Engagement Letter: A limited scope engagement letter is employed when the requested audit services are focused on specific areas, such as internal controls, revenue recognition, or inventory management. This specialized engagement letter allows the accounting firm and the client to define the restricted scope of work to attain specific audit objectives according to the client's needs. 3. Specialized North Carolina Engagement Letter for Government Entities: Government entities in North Carolina often require audits that adhere to specific regulatory guidelines. A specialized engagement letter for government entities ensures compliance with government regulations and highlights additional reporting requirements, such as Single Audit Act compliance or Government Auditing Standards (Yellow Book) procedures. 4. Non-Profit North Carolina Engagement Letter for Audit Services: Non-profit organizations in North Carolina may have unique audit requirements. This engagement letter highlights specific considerations for non-profit entities, such as adhering to Generally Accepted Auditing Standards (GAS), reviewing compliance with 501(c)(3) tax-exempt status, assessing potential risks associated with donor contributions, and proper financial reporting for grants. 5. North Carolina Engagement Letter for Internal Audit Services: Internal audit services provide clients with independent assessments of their internal controls, risk management systems, and operational efficiency. This type of engagement letter outlines the scope of the internal audit engagement, emphasizing the importance of objectivity, confidentiality, and professional judgment in conducting internal audit procedures. 6. Joint Venture North Carolina Engagement Letter: When two or more entities collaborate on a business venture in North Carolina, a joint venture engagement letter is used to outline mutual responsibilities, shared costs, and objectives of the audit engagement. This letter establishes the governance structure, financial reporting requirements, and the scope of the audit procedures applicable to the joint venture entity. Conclusion: North Carolina Engagement Letters between accounting firms and clients for audit services come in various types, tailored to specific audit scenarios and industry requirements. These formal agreements ensure a transparent understanding between the accounting firm and the client, allowing for a successful and productive audit engagement. It is essential for both parties to carefully review and agree upon the terms detailed in the engagement letter before commencing any audit services.