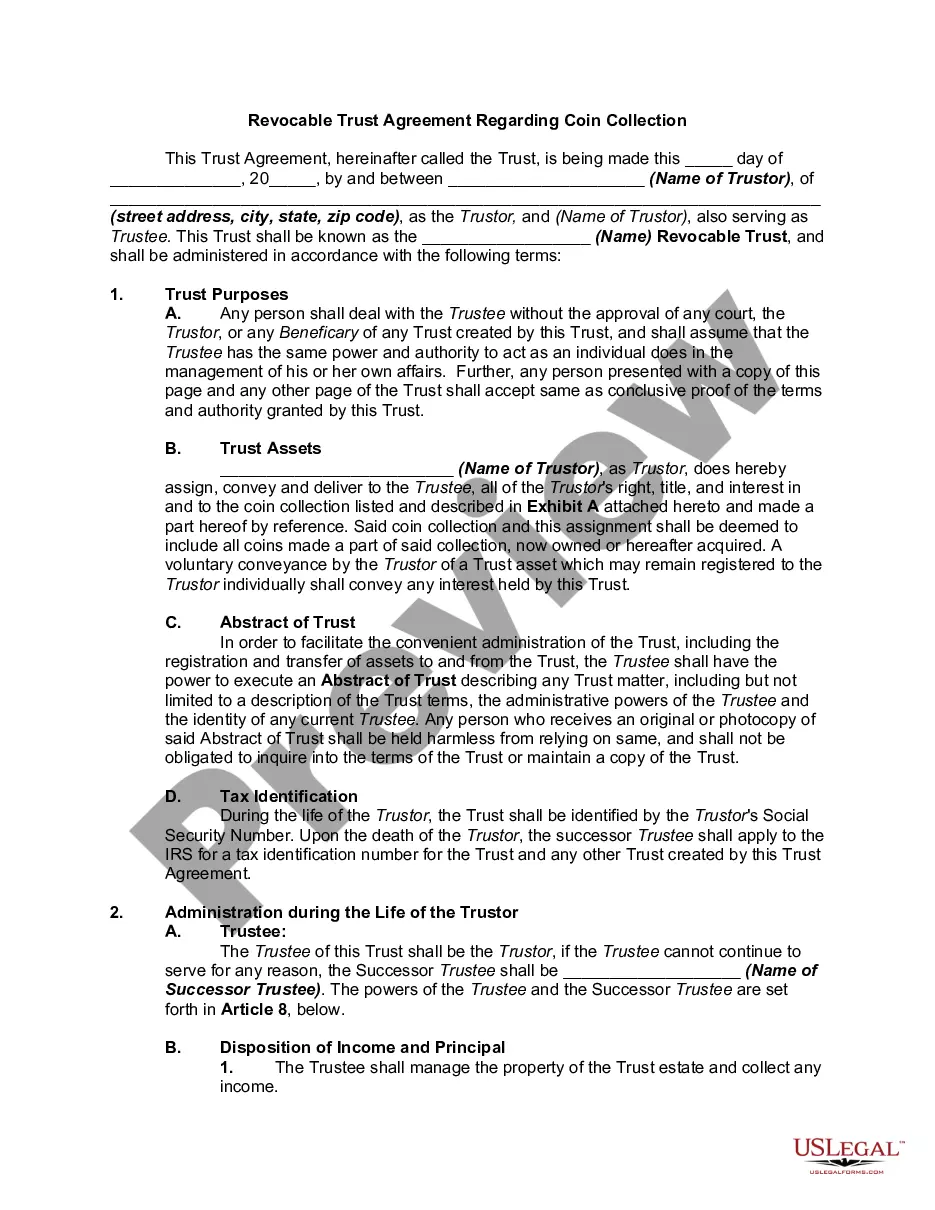

A Trust is an entity which owns assets for the benefit of a third person (the beneficiary). A Living Trust is an effective way to provide lifetime and after-death property management and estate planning. When you set up a Living Trust, you are the Grantor. Anyone you name within the Trust who will benefit from the assets in the Trust is a beneficiary. In addition to being the Grantor, you can also serve as your own Trustee. As the Trustee, you can transfer legal ownership of your property to the Trust. A revocable living trust does not constitute a gift, so there are no gift tax consequences in setting it up.

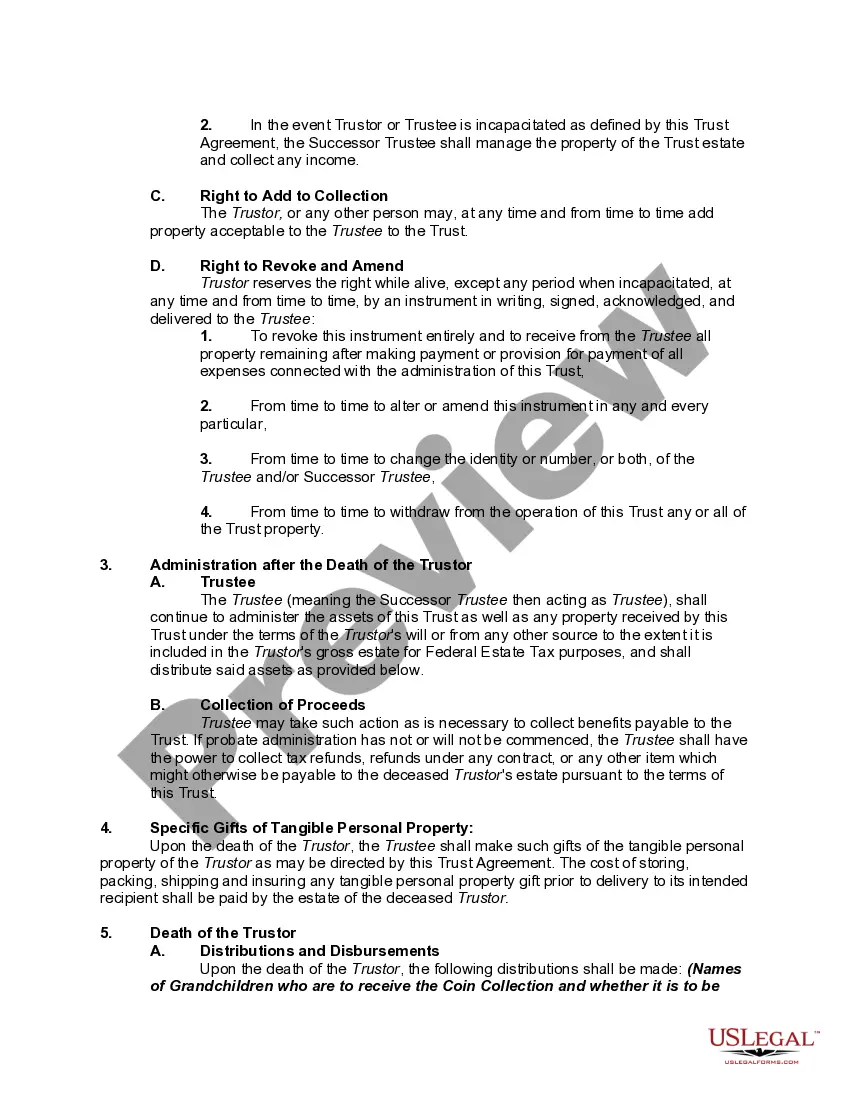

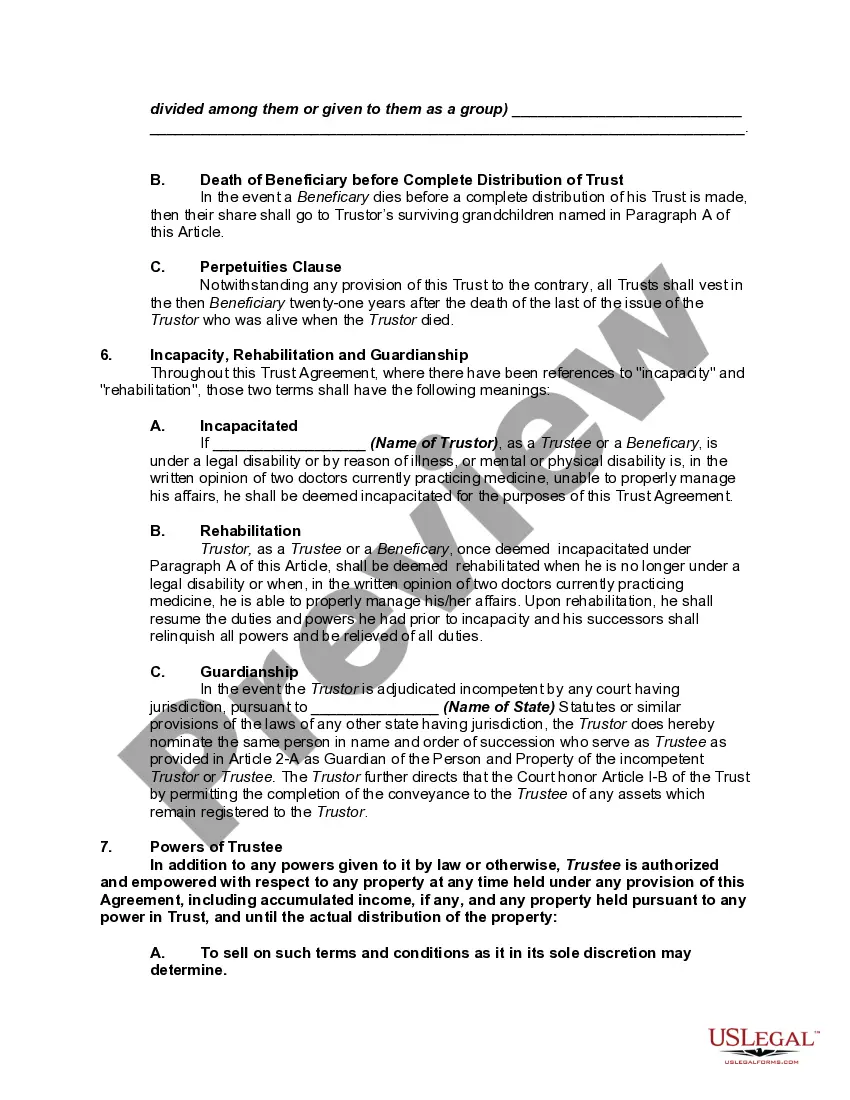

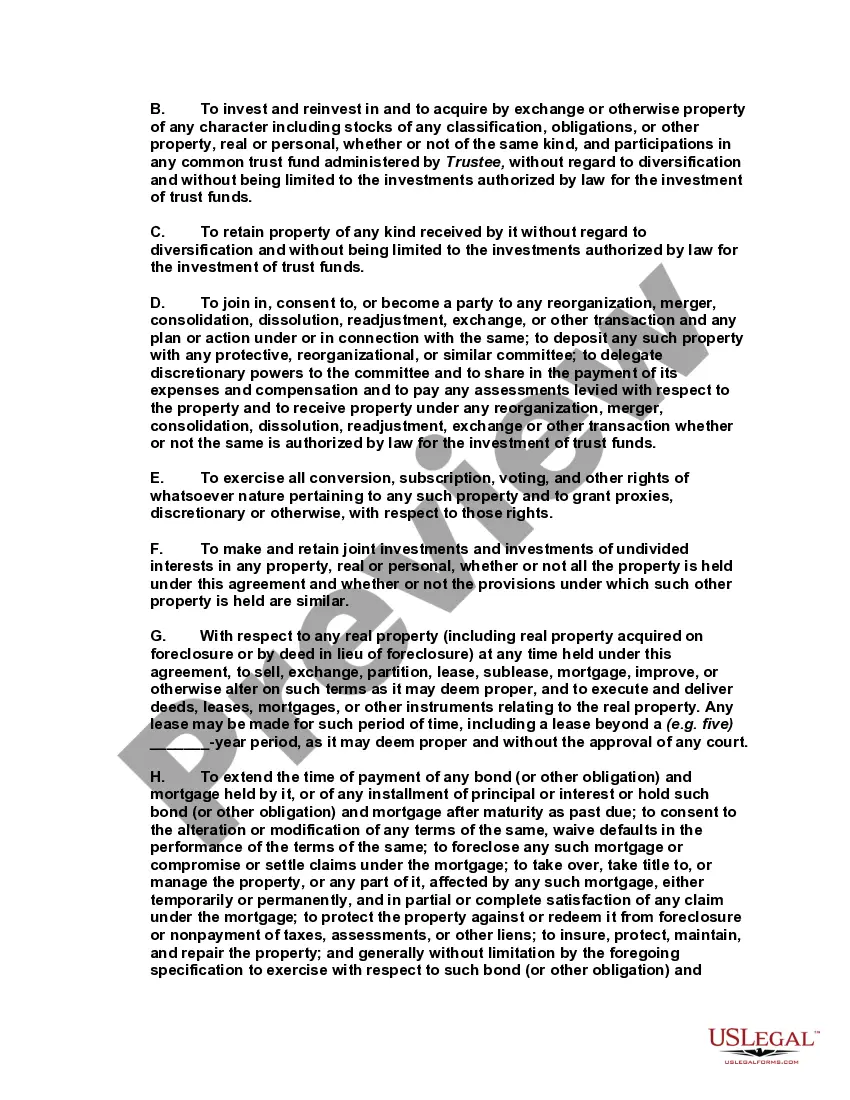

A North Carolina Revocable Trust Agreement Regarding Coin Collection is a legally binding document that outlines the terms and conditions for the ownership, management, and distribution of a coin collection placed within a trust in North Carolina. This agreement serves to protect the value, integrity, and preservation of the coins while enabling the trust's creator, known as the granter, to retain control over the assets during their lifetime. The North Carolina revocable trust agreement provides flexibility by allowing the granter to amend or revoke the trust at any time while they are alive, ensuring they maintain control over their coin collection. This type of trust agreement is often chosen by individuals who wish to plan for the management and ultimate distribution of their coins upon their death while avoiding probate. There are several variations or additional clauses that can be included in a North Carolina Revocable Trust Agreement Regarding Coin Collection, depending on the granter's specific needs: 1. Distribution Instructions: This clause details how the coin collection should be distributed among the beneficiaries upon the granter's death, whether it be dividing the collection equally among multiple beneficiaries or designating specific coins to individuals. 2. Successor Trustee Appointment: In the event of the granter's incapacitation or death, a successor trustee is named to take over the management of the trust and ensure the proper administration and distribution of the coins. 3. Preservation Guidelines: This clause outlines guidelines for the care, maintenance, and preservation of the coin collection, ensuring it remains in excellent condition and retains its value. 4. Appraisal Process: The agreement may include instructions on how the coin collection is to be appraised periodically to determine its value. This provides clarity and transparency to the beneficiaries and ensures the trust's assets are properly accounted for. 5. Tax and Legal Considerations: A North Carolina Revocable Trust Agreement Regarding Coin Collection may incorporate tax planning strategies or legal considerations to mitigate any potential tax liabilities or legal issues that may arise upon the granter's death. By establishing a North Carolina Revocable Trust Agreement Regarding Coin Collection, individuals can have peace of mind knowing that their collection will be properly managed and distributed according to their wishes. Consulting with an experienced attorney in North Carolina who specializes in estate planning and trusts is highly recommended ensuring compliance with state laws and to draft an agreement that accurately reflects the granter's intentions.A North Carolina Revocable Trust Agreement Regarding Coin Collection is a legally binding document that outlines the terms and conditions for the ownership, management, and distribution of a coin collection placed within a trust in North Carolina. This agreement serves to protect the value, integrity, and preservation of the coins while enabling the trust's creator, known as the granter, to retain control over the assets during their lifetime. The North Carolina revocable trust agreement provides flexibility by allowing the granter to amend or revoke the trust at any time while they are alive, ensuring they maintain control over their coin collection. This type of trust agreement is often chosen by individuals who wish to plan for the management and ultimate distribution of their coins upon their death while avoiding probate. There are several variations or additional clauses that can be included in a North Carolina Revocable Trust Agreement Regarding Coin Collection, depending on the granter's specific needs: 1. Distribution Instructions: This clause details how the coin collection should be distributed among the beneficiaries upon the granter's death, whether it be dividing the collection equally among multiple beneficiaries or designating specific coins to individuals. 2. Successor Trustee Appointment: In the event of the granter's incapacitation or death, a successor trustee is named to take over the management of the trust and ensure the proper administration and distribution of the coins. 3. Preservation Guidelines: This clause outlines guidelines for the care, maintenance, and preservation of the coin collection, ensuring it remains in excellent condition and retains its value. 4. Appraisal Process: The agreement may include instructions on how the coin collection is to be appraised periodically to determine its value. This provides clarity and transparency to the beneficiaries and ensures the trust's assets are properly accounted for. 5. Tax and Legal Considerations: A North Carolina Revocable Trust Agreement Regarding Coin Collection may incorporate tax planning strategies or legal considerations to mitigate any potential tax liabilities or legal issues that may arise upon the granter's death. By establishing a North Carolina Revocable Trust Agreement Regarding Coin Collection, individuals can have peace of mind knowing that their collection will be properly managed and distributed according to their wishes. Consulting with an experienced attorney in North Carolina who specializes in estate planning and trusts is highly recommended ensuring compliance with state laws and to draft an agreement that accurately reflects the granter's intentions.