North Carolina Simple Promissory Note for Personal Loan

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Simple Promissory Note For Personal Loan?

US Legal Forms - one of the largest collections of legal documents in the USA - offers a diverse selection of legal document templates that you can download or print.

By utilizing the website, you can access numerous forms for business and personal purposes, categorized by type, state, or keywords.

You can obtain the latest versions of forms such as the North Carolina Simple Promissory Note for Personal Loan in a matter of seconds.

If the document does not fit your requirements, utilize the Search box at the top of the page to find the one that does.

Once satisfied with the document, finalize your selection by clicking the Acquire now button. Then, choose the payment plan you desire and provide your information to create an account.

- If you already have an account, Log In and download the North Carolina Simple Promissory Note for Personal Loan from the US Legal Forms repository.

- The Download button will be visible on every document you view.

- You can access all previously saved documents from the My documents section of your account.

- If you are using US Legal Forms for the first time, here are straightforward steps to get started.

- Ensure you select the correct document for your city/state.

- Click the Preview button to examine the content of the document.

Form popularity

FAQ

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.19-Aug-2021

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

In any event, a promissory note does not have to be notarized to be binding. The private respondents have admitted signing the two notes and they have not succeeded in proving that they did so "under duress, fear and undue influence."

Any two parties who wish to enter into a loan agreement can draft a promissory note, which states the intention of the lender to loan the borrower a specific amount of money, as well as the terms and conditions for repayment of that loan, to which both parties have agreed.

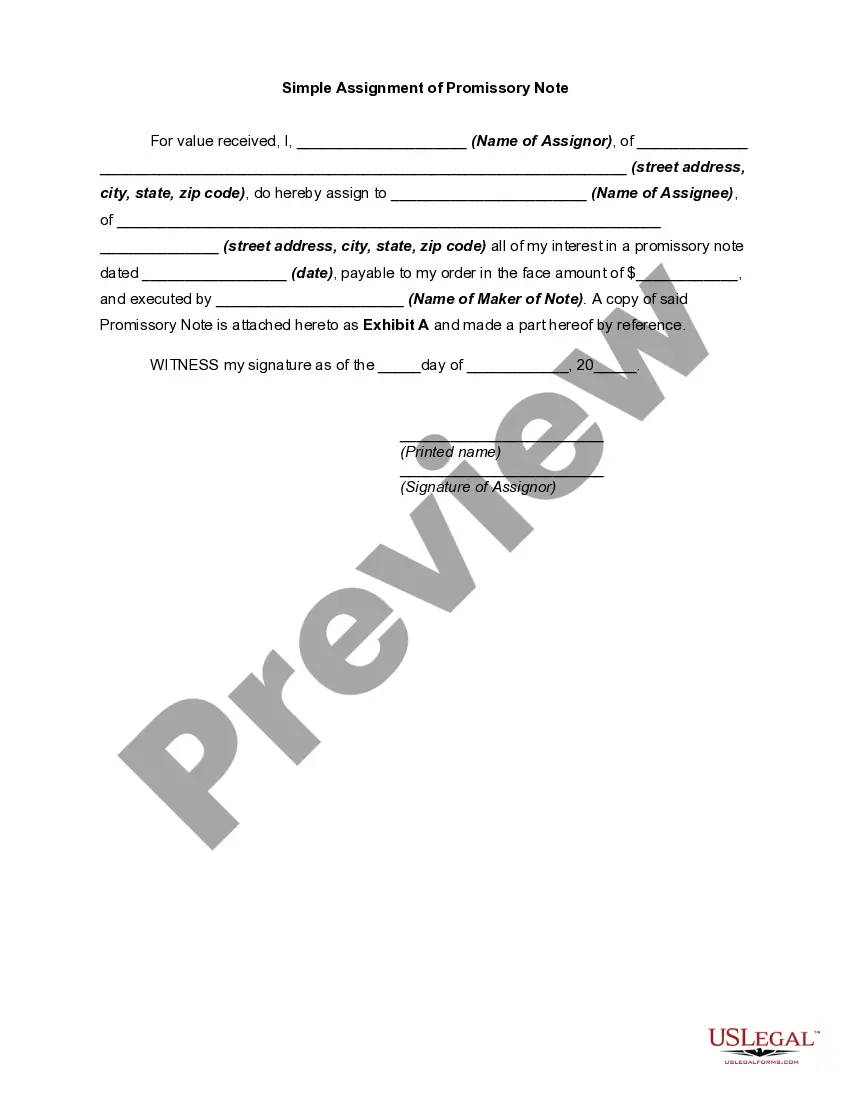

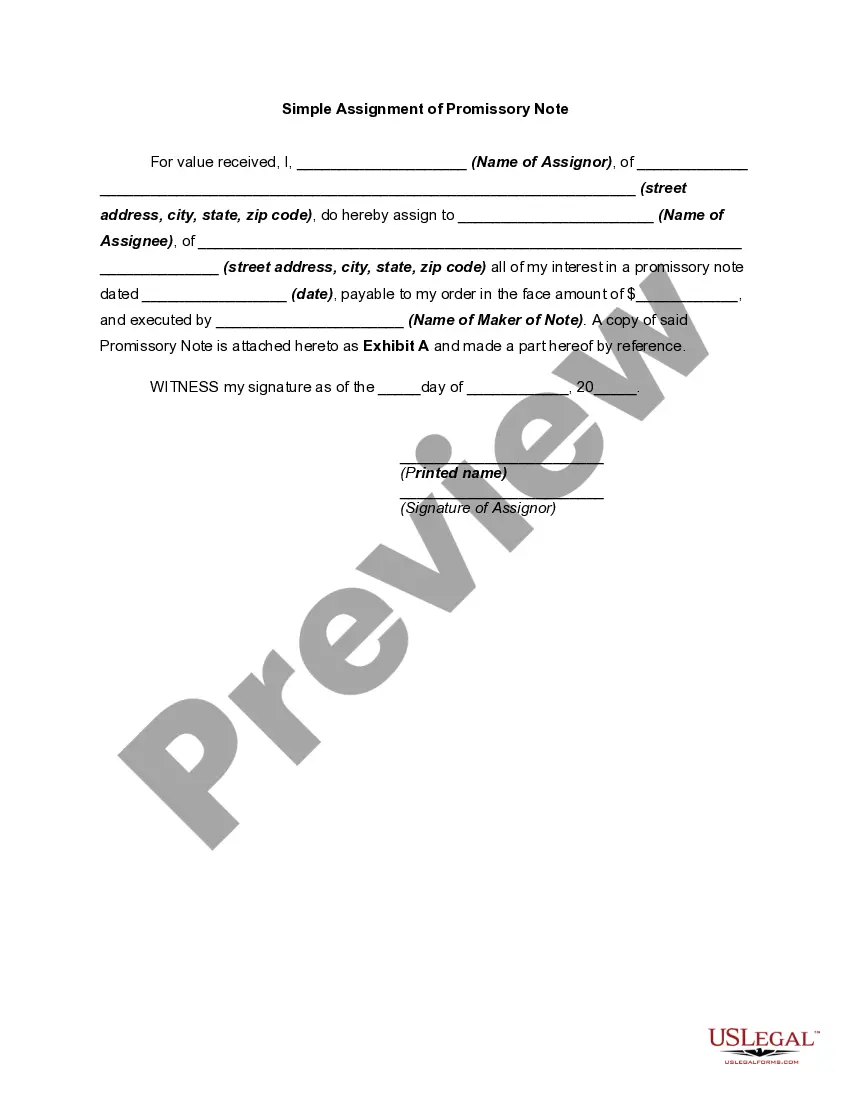

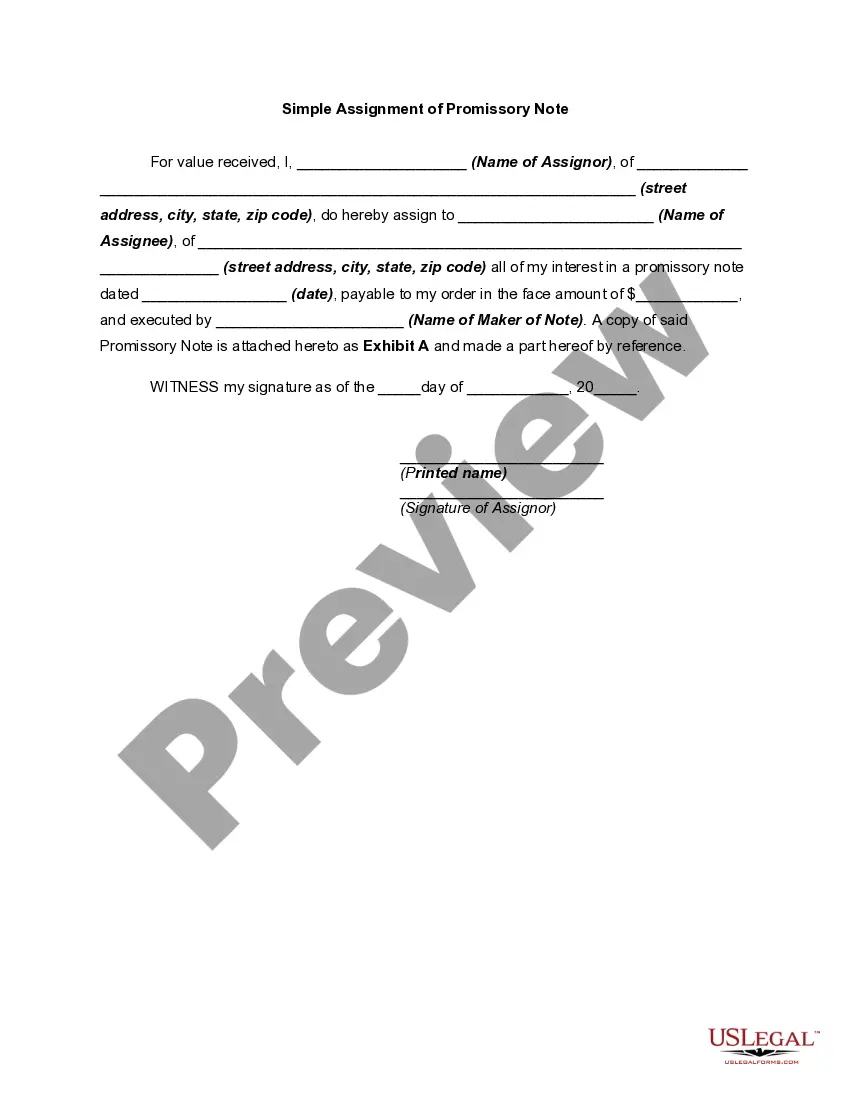

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

There is no legal requirement for most promissory notes to be witnessed or notarized in North Carolina. Still, the parties may decide to have the document certified by a notary public for protection in the event of a lawsuit.

To draft a Loan Agreement, you should include the following:The addresses and contact information of all parties involved.The conditions of use of the loan (what the money can be used for)Any repayment options.The payment schedule.The interest rates.The length of the term.Any collateral.The cancellation policy.More items...