The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

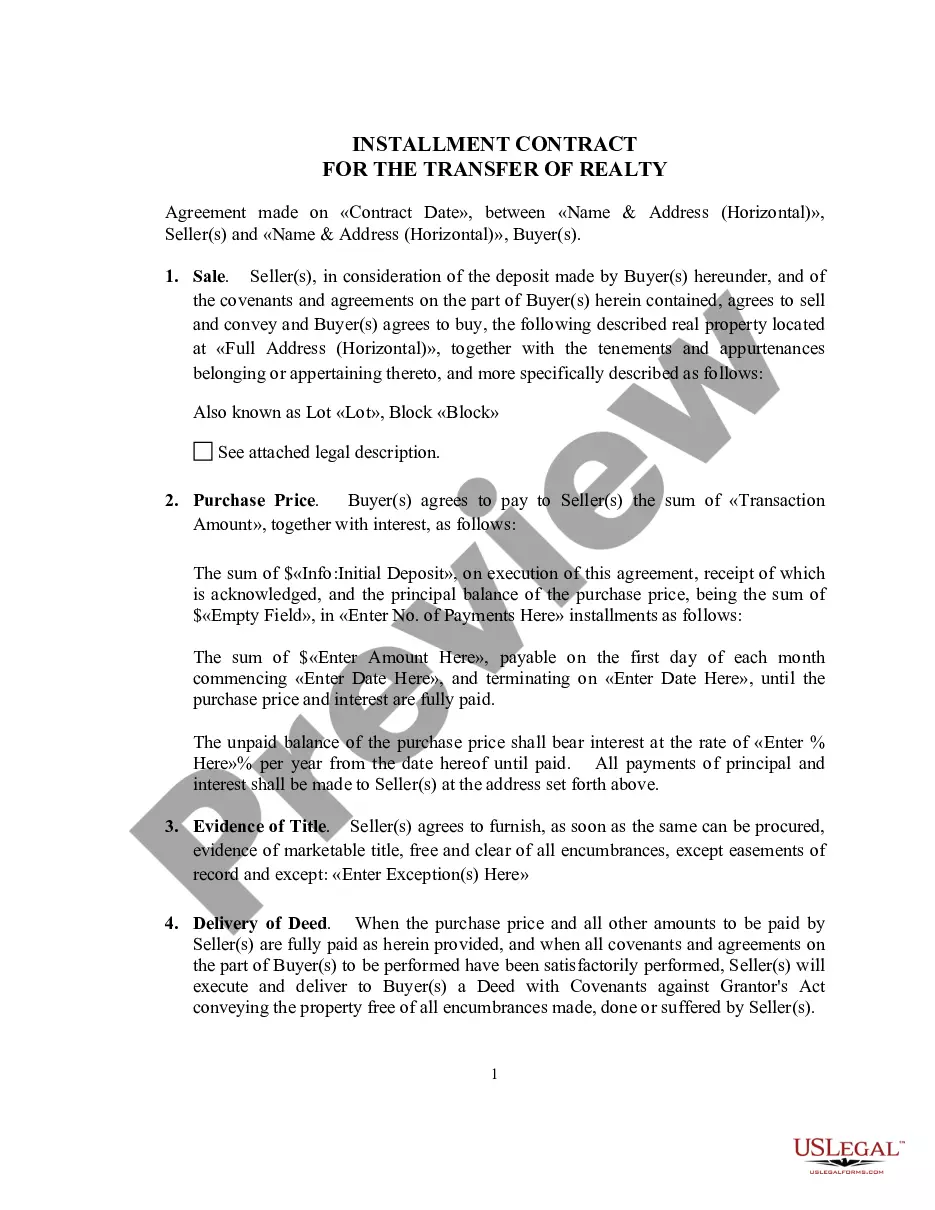

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Category:

State:

Multi-State

Control #:

US-02514BG

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures?

You may spend time browsing online for the authentic document template that meets the state and national requirements you need.

US Legal Forms offers thousands of legitimate templates that have been assessed by professionals.

You can obtain or create the North Carolina General Disclosures Mandated By The Federal Truth In Lending Act - Retail Installment Agreement - Closed End Disclosures through my services.

If available, use the Review button to preview the document template as well.

- If you already possess a US Legal Forms account, you can Log In and then click the Get button.

- After that, you can complete, modify, generate, or sign the North Carolina General Disclosures Mandated By The Federal Truth In Lending Act - Retail Installment Agreement - Closed End Disclosures.

- Every legitimate document template you purchase becomes yours permanently.

- To get another copy of any acquired form, go to the My documents section and click the relevant button.

- If this is your initial visit to the US Legal Forms site, follow the simple instructions listed below.

- First, ensure that you have selected the correct document template for the region/area of your choice.

- Check the document details to make sure you have picked the right form.

Form popularity

FAQ

Regulation Z requires that installment loans disclose the annual percentage rate, total finance charges, and payment terms. These disclosures ensure that borrowers are aware of the total costs associated with their loans. Understanding these details is essential when reviewing the North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, as it impacts your financial future.

If you believe there has been a violation of the Truth in Lending Act, you should first contact the lender for clarification. If the issue remains unresolved, you can file a complaint with the Consumer Financial Protection Bureau. For comprehensive support regarding the North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, reaching out to a legal professional or service like US Legal Forms can provide additional guidance.

The Retail Installment Sales Act in North Carolina governs how retail installment contracts are structured and disclosed. It ensures that consumers receive clear information regarding the terms of financing, including interest rates and payment schedules. By complying with the North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, retailers can build trust and transparency with their customers.

According to Regulation Z, all material closed-end credit disclosures must be clear, conspicuous, and in writing. They should be presented in a way that is easy for consumers to understand, using plain language and an organized format. The North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures exemplify these standards, promoting greater consumer awareness.

Regulation Z mandates specific consumer disclosures aimed at promoting informed borrowing. This includes the disclosure of the APR, finance charges, and the payment schedule, among other details. Adhering to the North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures is essential for lenders to comply with these regulations and avoid penalties.

A Truth in Lending disclosure statement must include the annual percentage rate (APR), finance charges, payment schedule, and total amount financed. Additionally, it may also contain information about any late fees and prepayment penalties. These details are essential for compliance with the North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

In an installment sales contract, the seller typically retains a security interest in the goods being sold until the buyer fulfills all payment obligations. This means that if payments are not made, the seller has the right to reclaim the item. Understanding this arrangement is vital for both parties, especially in the context of the North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

The Truth in Lending Disclosure must include several key items like the annual percentage rate (APR), total finance charges, payment schedule, and total amount financed. Additionally, it should also specify any fees or penalties for late payments. This comprehensive breakdown is essential for consumers to understand their financial commitments fully, as highlighted in the North Carolina General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.