A law partnership is a business entity formed by one or more lawyers to engage in the practice of law. The primary service provided by a law partnership is to advise clients about their legal rights and responsibilities, and to represent their clients in civil or criminal cases, business transactions and other matters in which legal assistance is sought.

A partnership is defined by the Uniform Partnership as a relationship created by the voluntary "association of two or more persons to carry on as co-owners of a business for profit." The people associated in this manner are called partners. A partner is the agent of the partnership. A partner is also the agent of each partner with respect to partnership matters. A partner is not an employee of the partnership. A partner is a co-owner of the business, including the assets of the business.

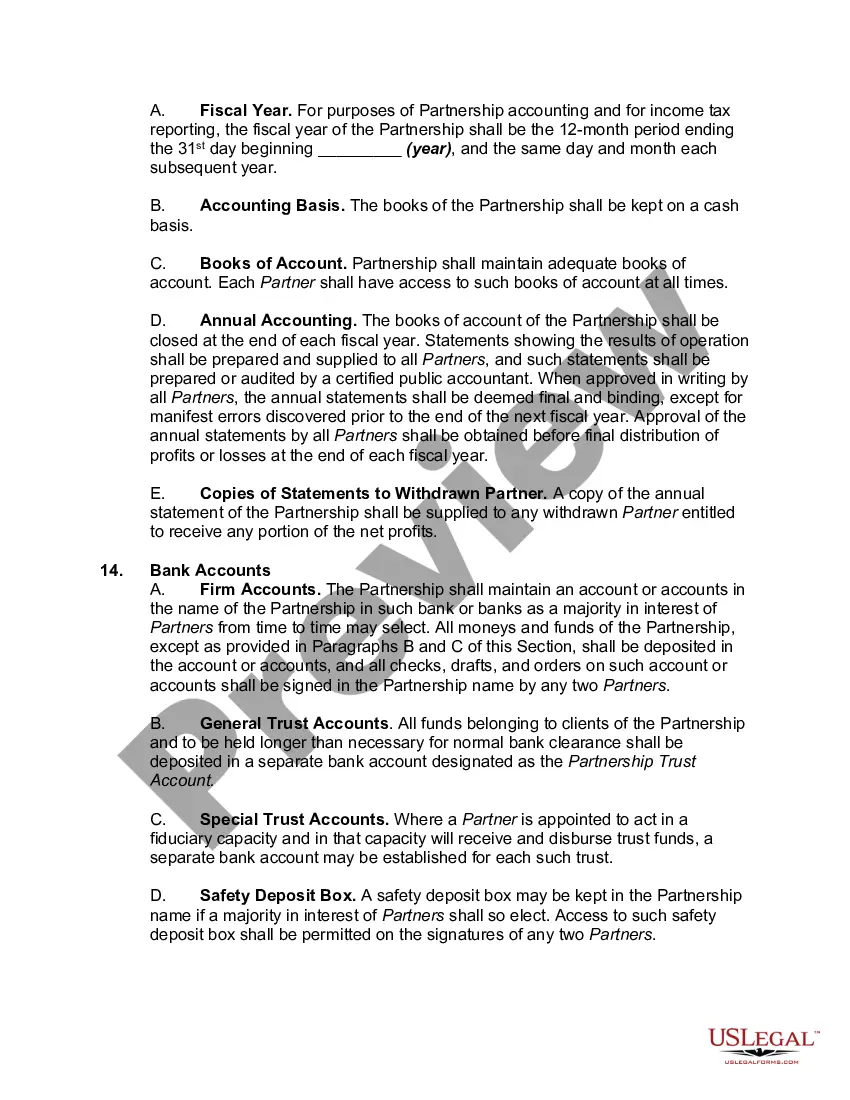

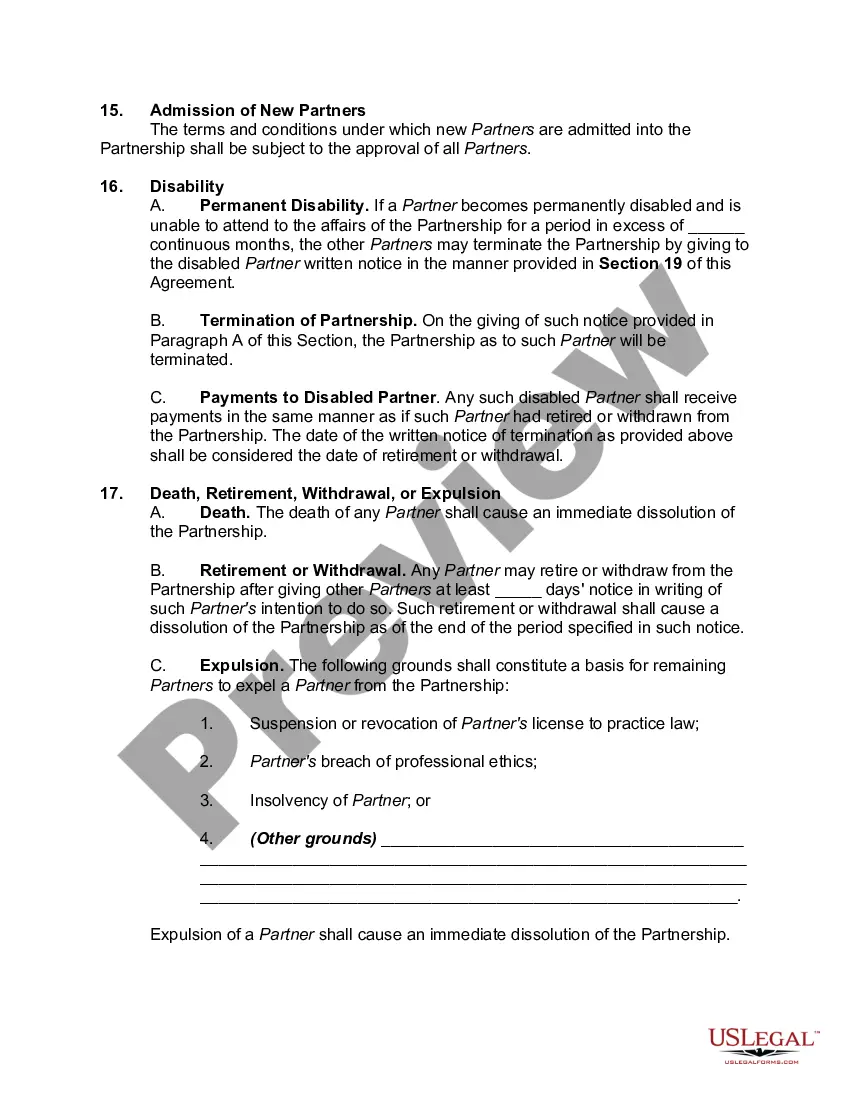

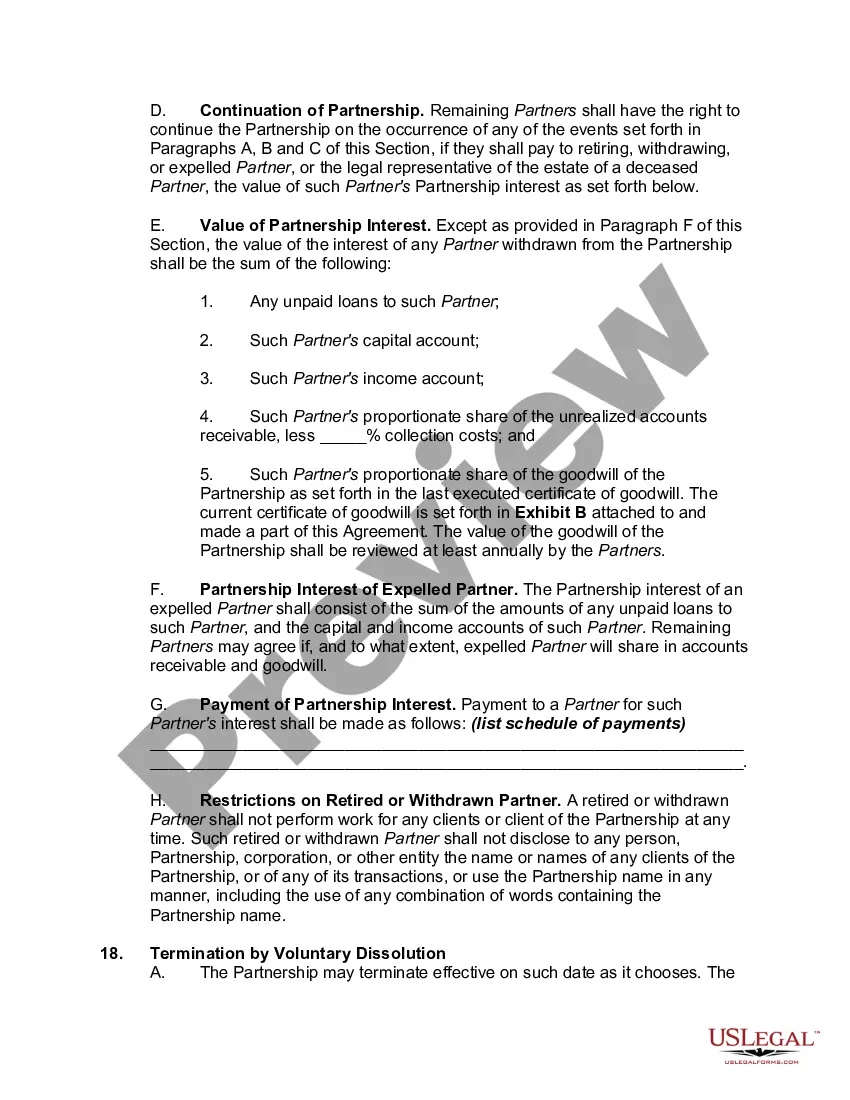

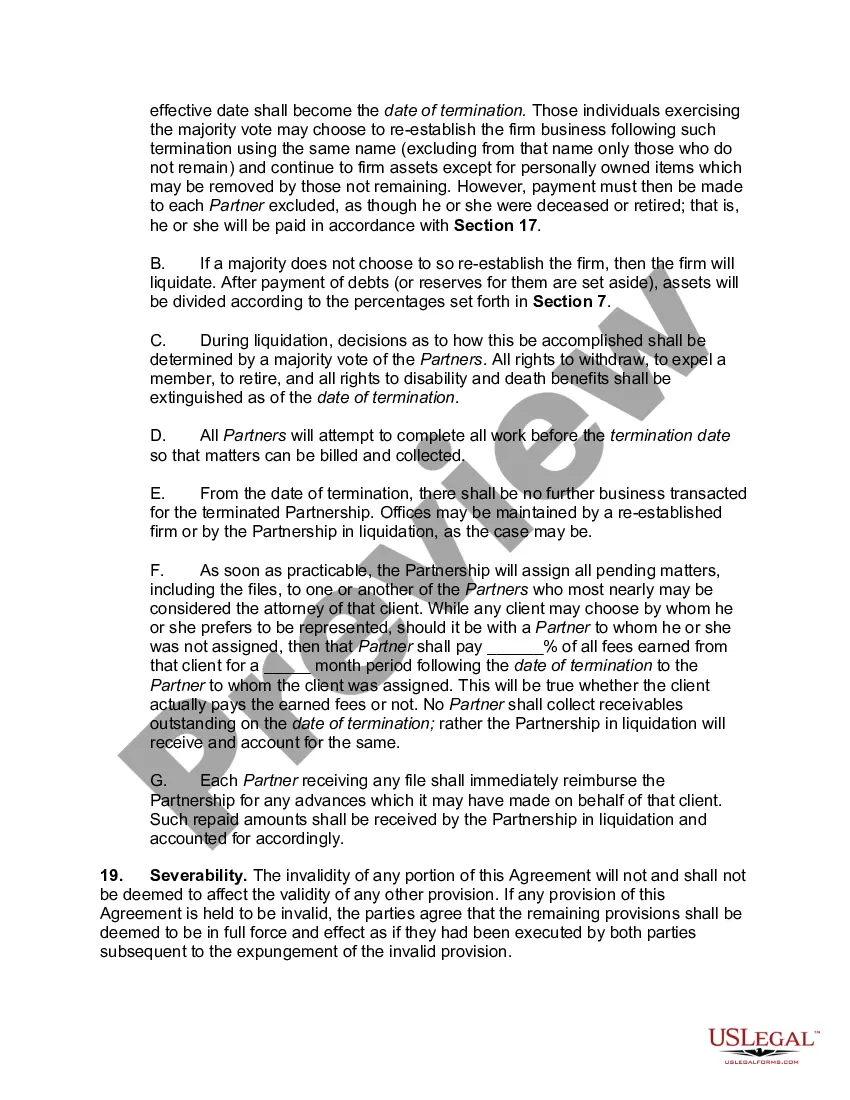

A North Carolina Law Partnership Agreement with Provisions for the Death, Retirement, Withdrawal, or Expulsion of a Partner is a legally binding document that outlines the terms and conditions governing the operations and dynamics of a partnership in North Carolina. This agreement covers various scenarios such as the death, retirement, withdrawal, or expulsion of a partner, aiming to provide clarity and protection for all parties involved. In North Carolina, there are several types of partnership agreements that can be established, each with its own set of provisions and considerations regarding partner changes. The two main types are General Partnership (GP) and Limited Partnership (LP). While both types have similar provisions for partner changes, LP agreements may have additional clauses specific to the roles and responsibilities of general partners versus limited partners. It is essential to consult a legal professional to ensure that the agreement complies with applicable laws and regulations. Provisions for the Death of a Partner: When a partner passes away, the partnership agreement outlines the steps to be taken, ensuring a smooth transition and the fair treatment of the deceased partner's estate. It typically includes provisions such as: — Notification requirements to the surviving partners and the deceased partner's legal representatives. — Valuation methods for determining the deceased partner's interest in the partnership. — The option for the partnership to purchase the deceased partner's interest or transfer it to their designated beneficiary. — Provisions for the allocation of profits, losses, and ongoing obligations during the transition period. Provisions for the Retirement of a Partner: The partnership agreement should clarify the process for a partner's voluntary retirement, focusing on aspects such as: — Notice requirements for retirement intent, allowing partners to plan accordingly. — Valuation methods to determine the retiring partner's interest in the partnership. — Options for distributing the retiring partner's interest, including buyout agreements or transferring it to remaining partners. — Terms for the continuation of the partnership business, including the adjustment of profit-sharing ratios and the redistribution of responsibilities. Provisions for the Withdrawal of a Partner: When a partner decides to withdraw from the partnership without retiring, provisions in the agreement should address: — Notice requirements for withdrawal, providing ample time for the remaining partners to adjust. — Valuation methods for determining the withdrawing partner's interest in the partnership. — Options for the distribution of the withdrawing partner's interest, such as buyout agreements or transferring it to remaining partners. — The impact on ongoing partnership obligations, decision-making, and profit-sharing. Provisions for the Expulsion of a Partner: If circumstances arise that necessitate the expulsion of a partner, the partnership agreement should outline: — The grounds for expulsion, such as a partner's breach of agreed-upon obligations, unethical behavior, or criminal activities. — The process for initiating and conducting an expulsion vote. — The consequences of expulsion, including the valuation and distribution of the expelled partner's interest, potential buyout provisions, and the impact on ongoing partnership operations. In summary, a North Carolina Law Partnership Agreement with provisions for the death, retirement, withdrawal, or expulsion of a partner is a comprehensive legal document that safeguards the rights and interests of all partners involved. Depending on the type of partnership, further variations and considerations may apply. Seeking guidance from a knowledgeable attorney will ensure the creation of a tailored agreement that conforms to North Carolina partnership laws and addresses any specific circumstances or requirements.A North Carolina Law Partnership Agreement with Provisions for the Death, Retirement, Withdrawal, or Expulsion of a Partner is a legally binding document that outlines the terms and conditions governing the operations and dynamics of a partnership in North Carolina. This agreement covers various scenarios such as the death, retirement, withdrawal, or expulsion of a partner, aiming to provide clarity and protection for all parties involved. In North Carolina, there are several types of partnership agreements that can be established, each with its own set of provisions and considerations regarding partner changes. The two main types are General Partnership (GP) and Limited Partnership (LP). While both types have similar provisions for partner changes, LP agreements may have additional clauses specific to the roles and responsibilities of general partners versus limited partners. It is essential to consult a legal professional to ensure that the agreement complies with applicable laws and regulations. Provisions for the Death of a Partner: When a partner passes away, the partnership agreement outlines the steps to be taken, ensuring a smooth transition and the fair treatment of the deceased partner's estate. It typically includes provisions such as: — Notification requirements to the surviving partners and the deceased partner's legal representatives. — Valuation methods for determining the deceased partner's interest in the partnership. — The option for the partnership to purchase the deceased partner's interest or transfer it to their designated beneficiary. — Provisions for the allocation of profits, losses, and ongoing obligations during the transition period. Provisions for the Retirement of a Partner: The partnership agreement should clarify the process for a partner's voluntary retirement, focusing on aspects such as: — Notice requirements for retirement intent, allowing partners to plan accordingly. — Valuation methods to determine the retiring partner's interest in the partnership. — Options for distributing the retiring partner's interest, including buyout agreements or transferring it to remaining partners. — Terms for the continuation of the partnership business, including the adjustment of profit-sharing ratios and the redistribution of responsibilities. Provisions for the Withdrawal of a Partner: When a partner decides to withdraw from the partnership without retiring, provisions in the agreement should address: — Notice requirements for withdrawal, providing ample time for the remaining partners to adjust. — Valuation methods for determining the withdrawing partner's interest in the partnership. — Options for the distribution of the withdrawing partner's interest, such as buyout agreements or transferring it to remaining partners. — The impact on ongoing partnership obligations, decision-making, and profit-sharing. Provisions for the Expulsion of a Partner: If circumstances arise that necessitate the expulsion of a partner, the partnership agreement should outline: — The grounds for expulsion, such as a partner's breach of agreed-upon obligations, unethical behavior, or criminal activities. — The process for initiating and conducting an expulsion vote. — The consequences of expulsion, including the valuation and distribution of the expelled partner's interest, potential buyout provisions, and the impact on ongoing partnership operations. In summary, a North Carolina Law Partnership Agreement with provisions for the death, retirement, withdrawal, or expulsion of a partner is a comprehensive legal document that safeguards the rights and interests of all partners involved. Depending on the type of partnership, further variations and considerations may apply. Seeking guidance from a knowledgeable attorney will ensure the creation of a tailored agreement that conforms to North Carolina partnership laws and addresses any specific circumstances or requirements.