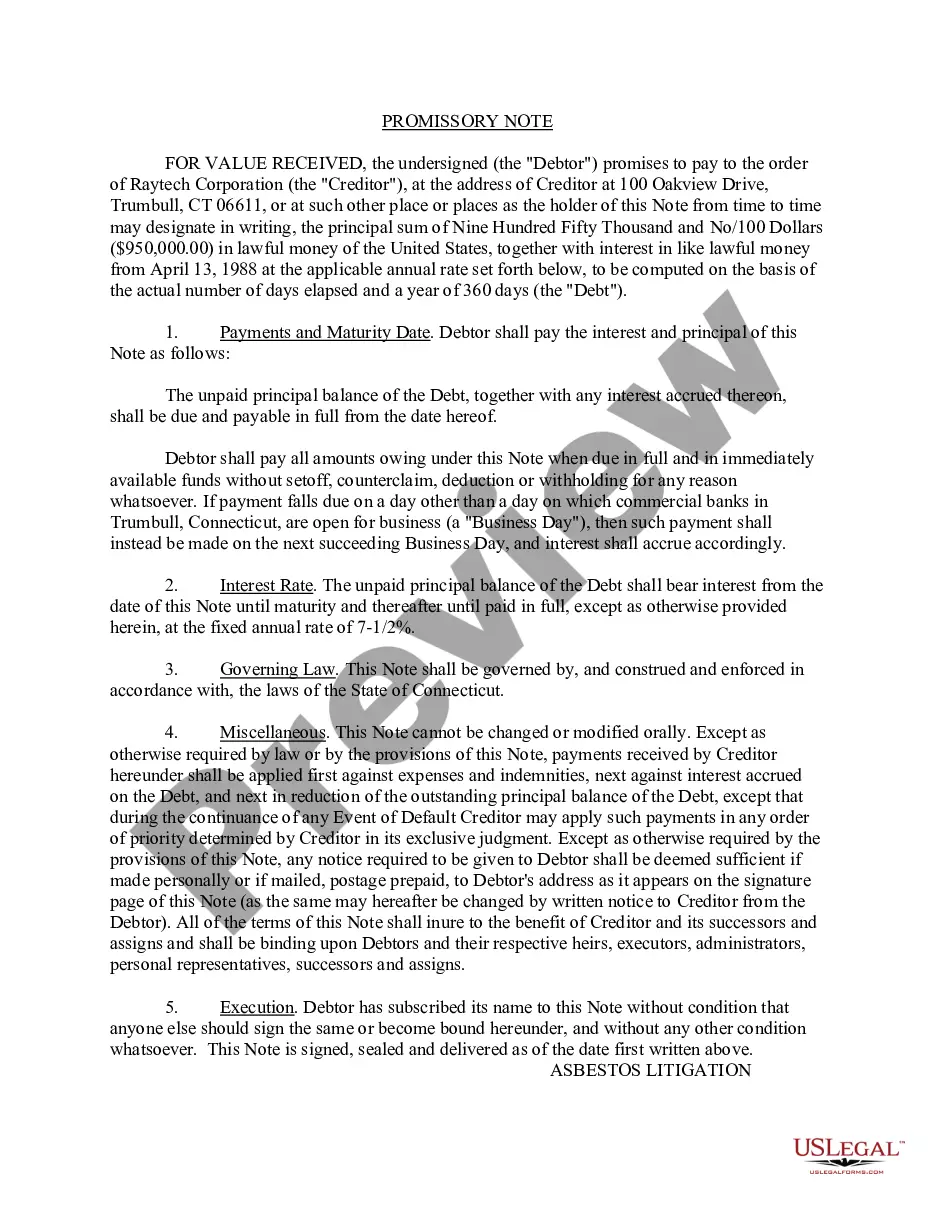

A promissory note is a written promise to pay a debt. It is an unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to the order of a specified person or to the bearer.

A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan. Default terms (what happens if a payment is missed or the loan is not paid off by its due date) should also be spelled out in the promissory note.

North Carolina Promissory Note in Connection with Sale of Motor Vehicle

Category:

State:

Multi-State

Control #:

US-02680BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Promissory Note In Connection With Sale Of Motor Vehicle?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a variety of legal form templates that you can download or print.

By using the website, you can access thousands of forms for business and personal use, organized by category, state, or keywords. You can obtain the latest forms such as the North Carolina Promissory Note related to Sale of Motor Vehicle within minutes.

If you already possess an account, Log In and download the North Carolina Promissory Note related to Sale of Motor Vehicle from the US Legal Forms library. The Download button will appear on every form you view. You can find all previously downloaded forms in the My documents section of your account.

Complete the transaction. Use your credit card or PayPal account to finalize the purchase.

Select the format and download the form onto your device. Make edits. Fill out, modify, print, and sign the downloaded North Carolina Promissory Note related to Sale of Motor Vehicle. All templates added to your account do not have an expiration date and are yours indefinitely. So, if you want to download or print another copy, simply navigate to the My documents section and click on the form you desire. Access the North Carolina Promissory Note related to Sale of Motor Vehicle with US Legal Forms, one of the most extensive collections of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs and requirements.

- Ensure you have selected the correct form for your city/state.

- Click on the Review button to examine the content of the form.

- Read the form description to confirm you have chosen the correct form.

- If the form does not meet your requirements, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your selection by clicking the Purchase now button.

- Then, choose the pricing plan you prefer and provide your details to register for an account.

Form popularity

FAQ

In North Carolina, the validity of a promissory note typically lasts for three years for most debts. However, some specific cases may have different timelines. It is crucial to keep a written record of the agreement to ensure its enforceability. A North Carolina Promissory Note in Connection with Sale of Motor Vehicle solidifies expectations between the buyer and seller, creating clarity for both parties.

Yes, when you sell your car in North Carolina, you must either return the license plate to the DMV or keep it for use on another vehicle. This requirement helps prevent legal issues related to the vehicle after the sale. Make sure to inform the buyer that they need to obtain their own registration and license plates for the vehicle. This maintains proper records for both parties involved in the transaction.

To cancel your car registration in North Carolina, you'll need to return your plates to the DMV or completely destroy them. Fill out the appropriate form to initiate the cancellation process. This step ensures that you are no longer liable for property taxes associated with the vehicle. You may also want to keep a copy of the registration cancellation for your records.

To notify the DMV that you sold your car in North Carolina, you must complete a notice of sale. This form is available on the DMV website or at any local DMV office. After filling it out, submit it by mail or in person. Informing the DMV helps protect you from any liability related to the vehicle after the sale.

To obtain a copy of a promissory note, reach out to the party with whom you entered into the agreement. If the North Carolina promissory note in connection with the sale of a motor vehicle is lost or misplaced, consider creating a new document, ideally using a reliable online platform like uslegalforms. This ensures that your new promissory note is thorough and legally compliant.

In North Carolina, a promissory note does not necessarily need to be notarized to be enforceable. However, having the North Carolina promissory note in connection with the sale of a motor vehicle notarized can add a layer of security and validity to the agreement. It can also help resolve disputes more easily if they arise.

Yes, many dealerships utilize promissory notes to facilitate vehicle sales. Dealerships often issue a North Carolina promissory note in connection with the sale of a motor vehicle, which outlines the terms of the sale and payment structure. This enables buyers to finance their purchases while providing the dealership with legal security.

Promissory notes can indeed hold up in court, especially when they meet legal requirements. In North Carolina, a well-drafted promissory note in connection with the sale of a motor vehicle can serve as strong evidence of the borrowing agreement. It's important to ensure the document contains clear terms and signatures of both parties to avoid disputes later.

Generally, a North Carolina Promissory Note in Connection with Sale of Motor Vehicle does not need registration. However, it is essential to review local laws to confirm that you meet all necessary requirements. To ensure everything is correctly documented, you may want to use resources like uslegalforms, which can guide you through the process.

Typically, a North Carolina Promissory Note in Connection with Sale of Motor Vehicle may be considered exempt from securities regulations under certain conditions. It is vital to understand the specific characteristics of the note to determine its status. Consult a legal expert who can provide insights tailored to your situation.