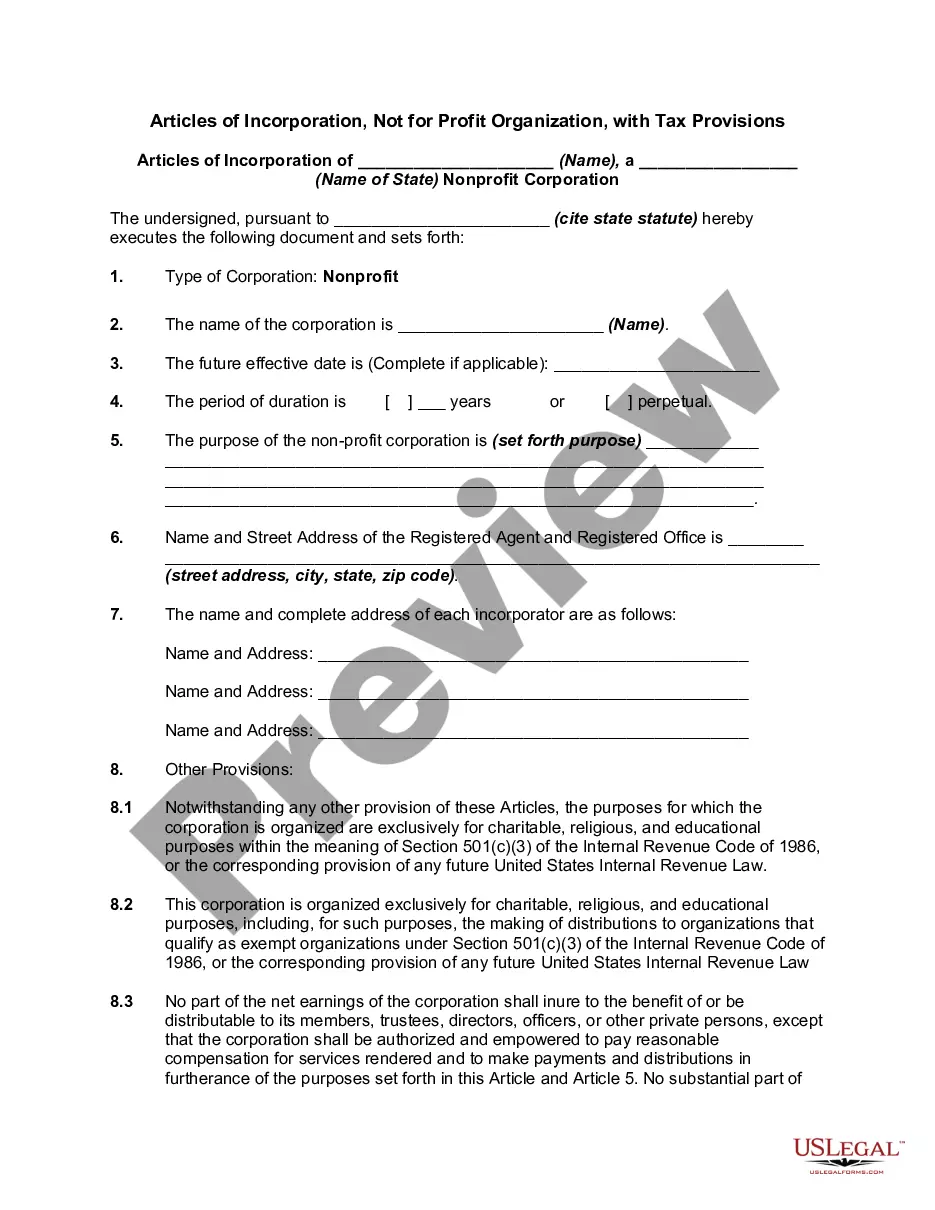

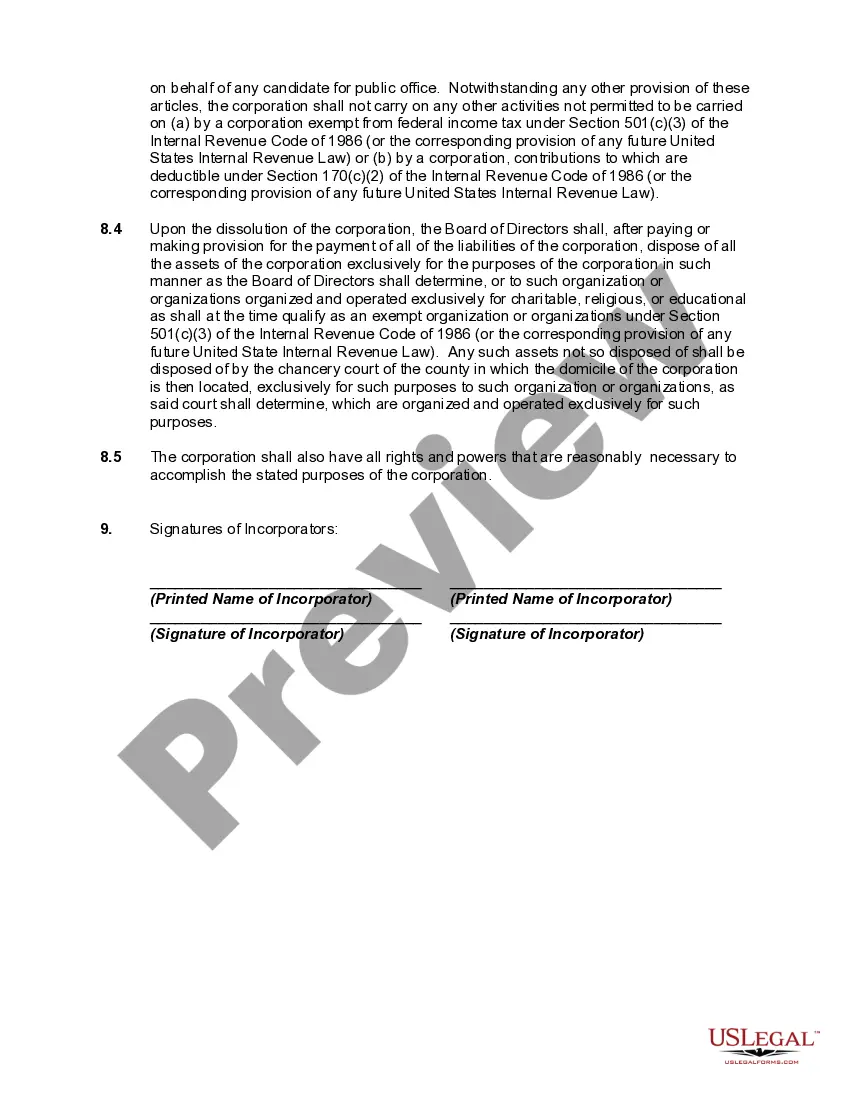

The proper form and necessary content of articles or certificates of incorporation for a nonprofit corporation depend largely on the requirements of the state nonprofit corporation act in the state of incorporation. Typically nonprofit corporations have no capital stock and therefore have members, not stockholders. Because federal tax-exempt status will be sought for most nonprofit corporations, the articles or certificate of incorporation must be carefully drafted to include specific language designed to ensure qualification for tax-exempt status.

North Carolina Articles of Incorporation for Not for Profit Organization with Tax Provisions The North Carolina Articles of Incorporation for a Not for Profit Organization with Tax Provisions is a legal document used to establish a non-profit organization in the state of North Carolina while ensuring compliance with tax regulations. This document outlines various key details, including the purpose of the organization, its registered agent, the members or directors, and the specific tax provisions it will adhere to. The purpose of a non-profit organization, as specified in its Articles of Incorporation, is to address a specific social, educational, religious, or humanitarian need. These purposes can vary widely, from supporting underprivileged communities, promoting the arts, advocating for human rights, or conducting scientific research. The Articles of Incorporation outline the organization's mission and goals, emphasizing its dedication to public welfare rather than generating profits. In North Carolina, different types of non-profit organizations may exist, each requiring specific Articles of Incorporation. They include charitable organizations, religious organizations, educational institutions, scientific research bodies, and others. To maintain their non-profit status, these organizations must abide by relevant tax provisions set forth by the Internal Revenue Service (IRS) and the North Carolina Department of Revenue. The North Carolina Articles of Incorporation for a Not for Profit Organization with Tax Provisions also require necessary information regarding the organization's leadership. This includes the names and addresses of the initial directors or members responsible for overseeing the organization's activities. The document also designates a registered agent who will act as the main point of contact for any legal correspondence. Regarding tax provisions, the organization must specify its commitment to comply with applicable state and federal tax laws. This typically involves obtaining the appropriate tax-exempt status, such as 501(c)(3) under the IRS regulations. By obtaining this status, the organization can qualify to receive tax-deductible donations and exemptions from certain taxes. Careful attention must be paid to accurately articulate the organization's tax-exempt purpose and activities in alignment with the tax laws. In some cases, the Articles of Incorporation may also include additional provisions, such as limitations on the organization's activities, requirements for the distribution of assets upon dissolution, or specific provisions related to membership and governance. Overall, the North Carolina Articles of Incorporation for a Not for Profit Organization with Tax Provisions play a crucial role in establishing a legally recognized non-profit entity. By carefully adhering to the specific requirements and tax provisions, organizations can gain tax-exempt status and fulfill their mission to serve the public interest in the state of North Carolina.