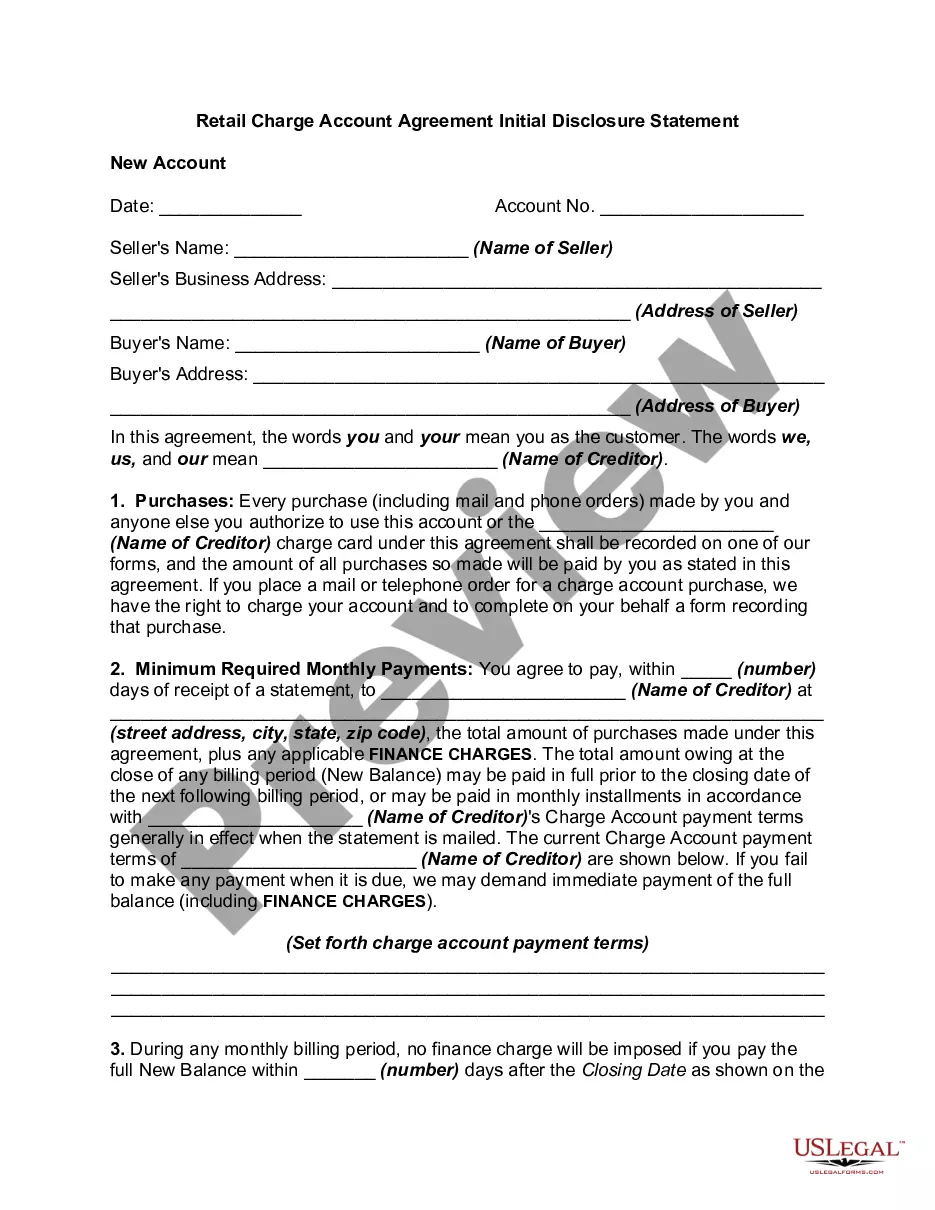

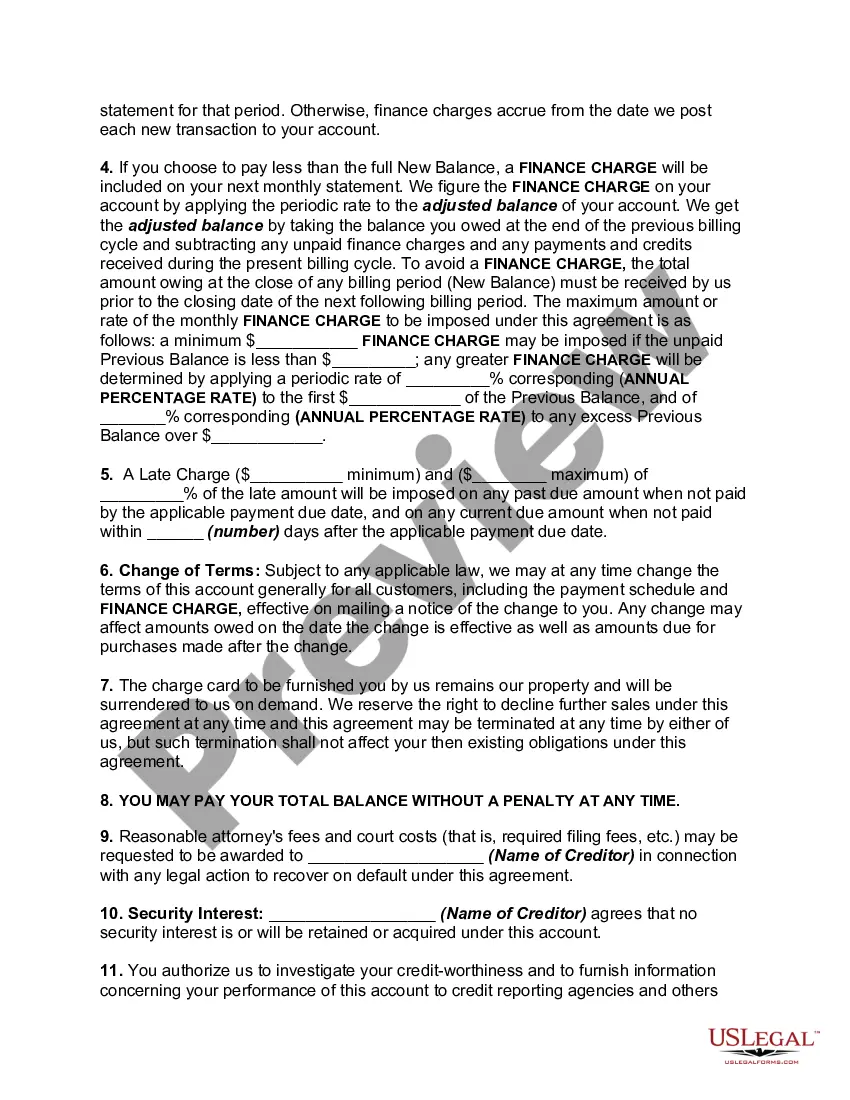

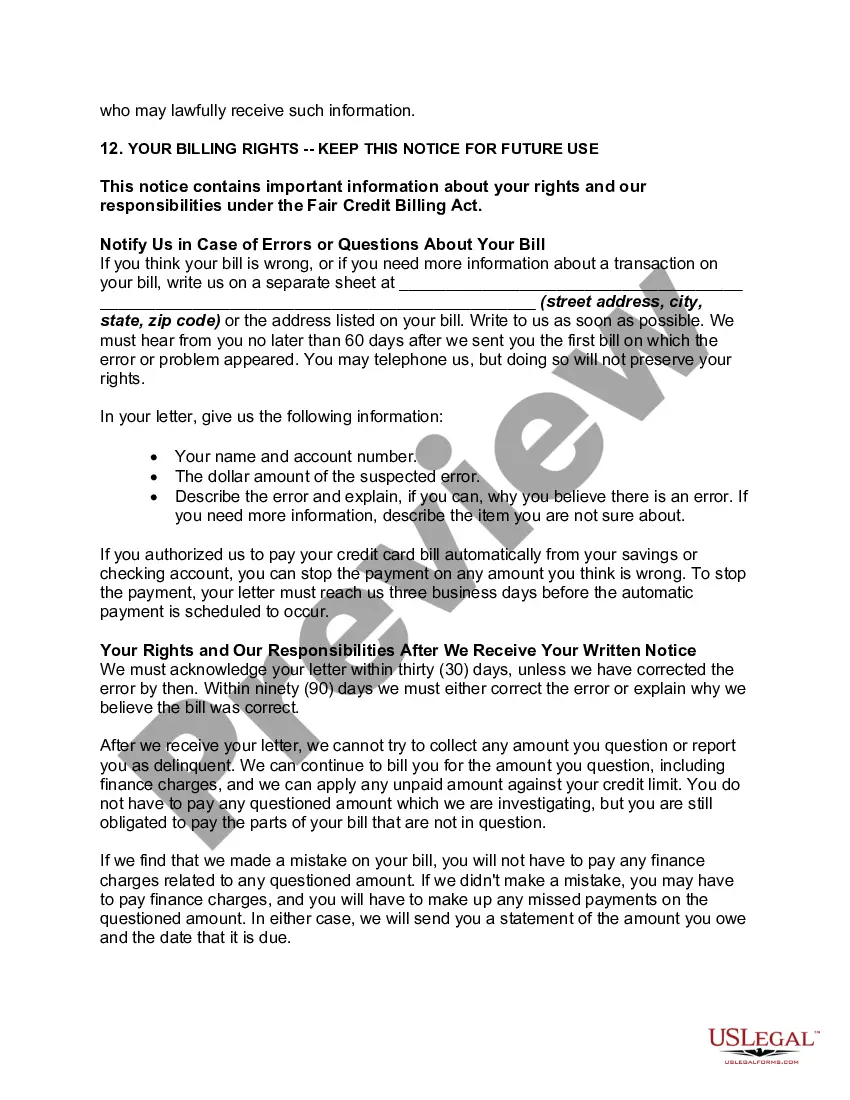

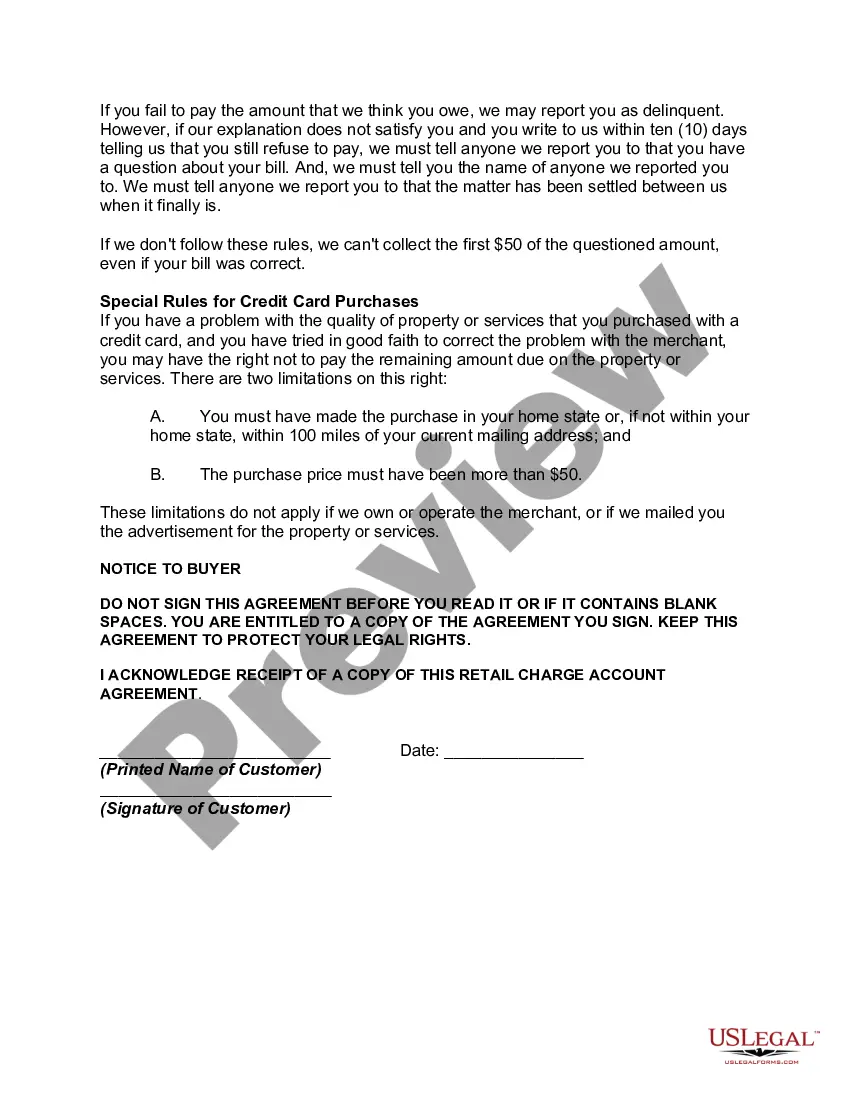

The North Carolina Retail Charge Account Agreement Initial Disclosure Statement is a legally binding document that outlines the terms and conditions of a retail charge account in the state of North Carolina. This statement serves as a key initial disclosure for both the retailer and the consumer, ensuring transparency and providing crucial information related to the credit agreement. The Retail Charge Account Agreement Initial Disclosure Statement in North Carolina cover various aspects concerning the establishment, management, and usage of the retail charge account. This includes the terms of the credit extension, interest rates, fees, grace periods, payment schedules, and more. Compliance with state-specific laws and regulations is also highlighted within the document. There are different types of North Carolina Retail Charge Account Agreement Initial Disclosure Statements depending on the nature of the retail establishment. For instance, department stores, convenience stores, specialty shops, and online retailers may have distinct sets of initial disclosures. While the general framework remains the same, specific terms, interest rates, and fees may vary based on the retailer's policies. When consumers apply for a retail charge account in North Carolina, they are provided with this Initial Disclosure Statement as part of the application process. It is essential for consumers to carefully read and understand the terms outlined in the document before accepting the retail charge account. By doing so, they can make informed decisions and ensure they are fully aware of their obligations and rights as a cardholder. Moreover, this document offers protection to consumers against unfair practices and hidden charges by retailers. It acts as a legal framework that guarantees transparency and prevents misunderstandings or deceptive acts. Retailers, on the other hand, benefit from the Initial Disclosure Statement as it sets clear guidelines for conducting business and establishes a foundation for maintaining a healthy retailer-customer relationship. In summary, the North Carolina Retail Charge Account Agreement Initial Disclosure Statement is a crucial document that outlines the terms and conditions of a retail charge account in the state. By providing comprehensive and relevant information, it ensures transparency and protects the rights of both retailers and consumers. It is vital for individuals to carefully review this document, considering factors such as interest rates, fees, and payment schedules, before accepting a retail charge account.

North Carolina Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out North Carolina Retail Charge Account Agreement Initial Disclosure Statement?

US Legal Forms - one of many biggest libraries of authorized varieties in the United States - provides a wide array of authorized file layouts you are able to down load or produce. While using website, you will get thousands of varieties for enterprise and specific reasons, categorized by types, says, or key phrases.You can get the most up-to-date variations of varieties such as the North Carolina Retail Charge Account Agreement Initial Disclosure Statement within minutes.

If you currently have a membership, log in and down load North Carolina Retail Charge Account Agreement Initial Disclosure Statement in the US Legal Forms catalogue. The Acquire switch will show up on each form you perspective. You get access to all earlier downloaded varieties from the My Forms tab of your accounts.

If you want to use US Legal Forms for the first time, here are basic directions to get you started out:

- Be sure you have picked the proper form for your personal area/region. Go through the Preview switch to analyze the form`s information. Read the form information to ensure that you have chosen the right form.

- If the form does not satisfy your demands, use the Look for industry near the top of the display to obtain the one that does.

- In case you are pleased with the form, confirm your choice by visiting the Acquire now switch. Then, select the prices program you prefer and offer your credentials to register for an accounts.

- Method the purchase. Use your credit card or PayPal accounts to complete the purchase.

- Choose the structure and down load the form on the product.

- Make adjustments. Fill out, revise and produce and sign the downloaded North Carolina Retail Charge Account Agreement Initial Disclosure Statement.

Every template you put into your bank account does not have an expiration particular date and is also your own property eternally. So, in order to down load or produce yet another duplicate, just proceed to the My Forms section and then click on the form you want.

Get access to the North Carolina Retail Charge Account Agreement Initial Disclosure Statement with US Legal Forms, one of the most substantial catalogue of authorized file layouts. Use thousands of specialist and status-specific layouts that meet up with your small business or specific needs and demands.