North Carolina General Journal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out General Journal?

Have you ever been in a situation where you needed documents for business or personal reasons on a regular basis.

There are numerous legal document templates accessible online, but locating ones that you can trust isn’t simple.

US Legal Forms offers thousands of form templates, including the North Carolina General Journal, that are designed to fulfill state and federal requirements.

Once you obtain the correct form, click Buy now.

Choose the pricing plan you prefer, provide the necessary information to create your account, and complete the purchase using PayPal or a credit card.

- If you are already familiar with the US Legal Forms site and possess an account, simply Log In.

- After that, you can download the North Carolina General Journal template.

- If you don't have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it is for the appropriate area/state.

- Use the Preview feature to review the document.

- Check the description to ensure you have selected the right form.

- If the form isn’t what you’re searching for, utilize the Search section to find a form that meets your requirements.

Form popularity

FAQ

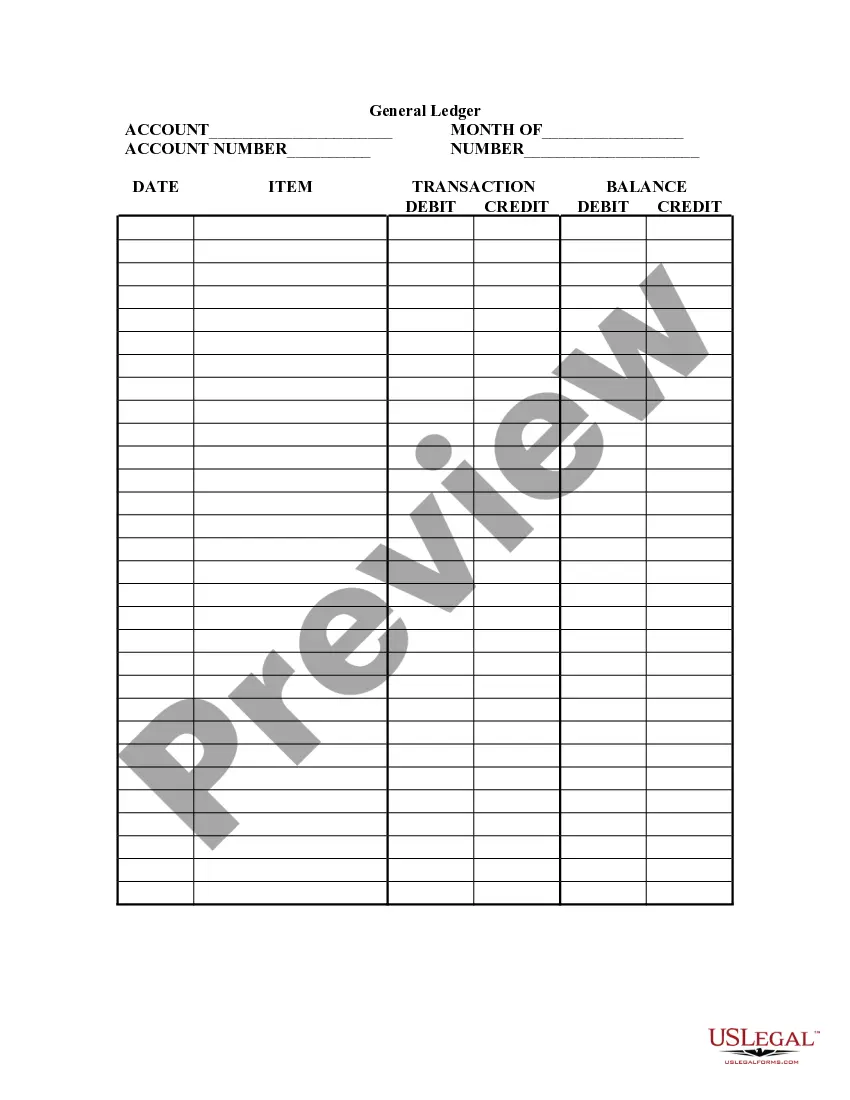

The North Carolina General Journal records all types of transactions that affect your business’s finances. These include sales, costs, expenses, and transfers, showcasing the complete financial activity of your organization. Each record includes critical information such as transaction dates, amounts, and descriptions, ensuring clarity in your financial reporting. This structured approach helps in generating accurate financial statements and analysis.

In the North Carolina General Journal, you will find a wide range of entries that detail the financial transactions of a business. These entries include sales, purchases, income, and expenses. Each transaction is documented with a date, amount, and description, allowing for a clear and organized record. This thorough documentation helps businesses track their financial health and makes it easier during audits.

Writing in a general journal involves documenting every financial transaction as it occurs. Begin with the date, followed by the details of the accounts affected, and the corresponding debits and credits. Regularly updating your North Carolina General Journal helps keep your accounts current and provides a clear financial picture.

To record a general journal entry, first, gather all necessary documentation supporting the transaction. Then, write the entry in your North Carolina General Journal, clearly indicating the date, accounts, and amounts involved. Ensure that you categorize transactions accurately to maintain clear records for future reference.

To make a general journal entry, start by identifying the accounts affected and determining whether they increase or decrease. Next, record the date, accounts involved, and the amounts debited and credited in your North Carolina General Journal. It's essential to ensure that the debits equal the credits to maintain balanced records.

The general journal records individual transactions in chronological order, while the general ledger organizes these transactions by account. In other words, the North Carolina General Journal captures the details of every transaction, whereas the general ledger summarizes them, allowing for easier tracking and reporting. Understanding this difference helps streamline your accounting process and improve financial reporting.

To do a general journal entry in the North Carolina General Journal, start by classifying the transaction into its respective accounts. Next, apply the debits and credits appropriately. Finally, record the entry in a clear and organized manner, including the date and a short description to help you or others understand the transaction later on.

To record a North Carolina General Journal, you will need to follow a structured approach. Identify the transaction type and determine the involved accounts. Ensure you write down the date, transaction details, and amounts debited and credited, keeping descriptions clear and concise for easy reference in the future.

Guidelines for using the North Carolina General Journal include ensuring that all entries are completed promptly and accurately. Use clear account titles and maintain order by entering transactions chronologically. Regularly review the journal to verify that it aligns with other financial records, helping to maintain accuracy across your bookkeeping.

To record an entry in the North Carolina General Journal, begin by analyzing the financial transaction. Next, decide on the debit and credit accounts. Write the entry in the specified format, making sure to include the date, the accounts involved, and a brief explanation of the transaction to enhance clarity and understanding.