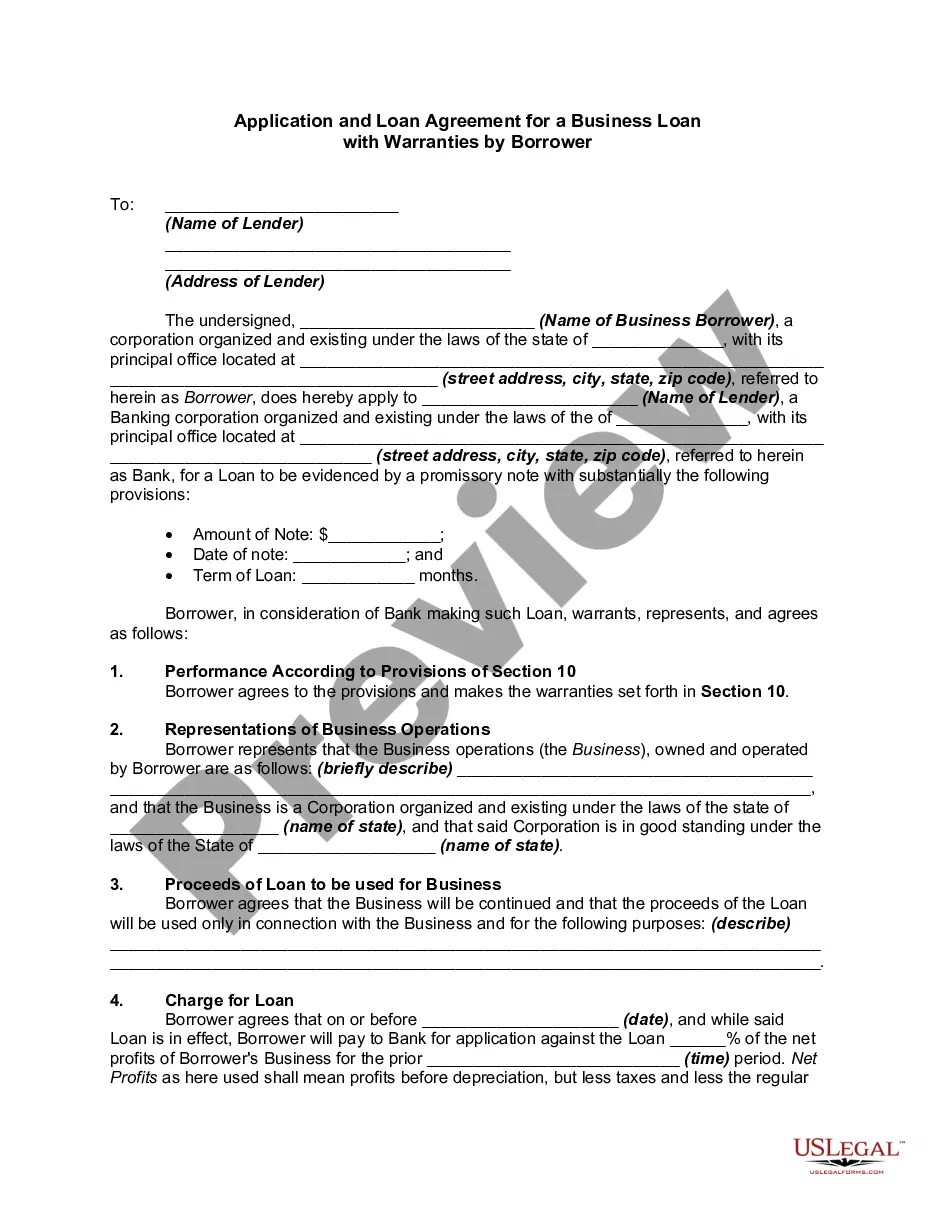

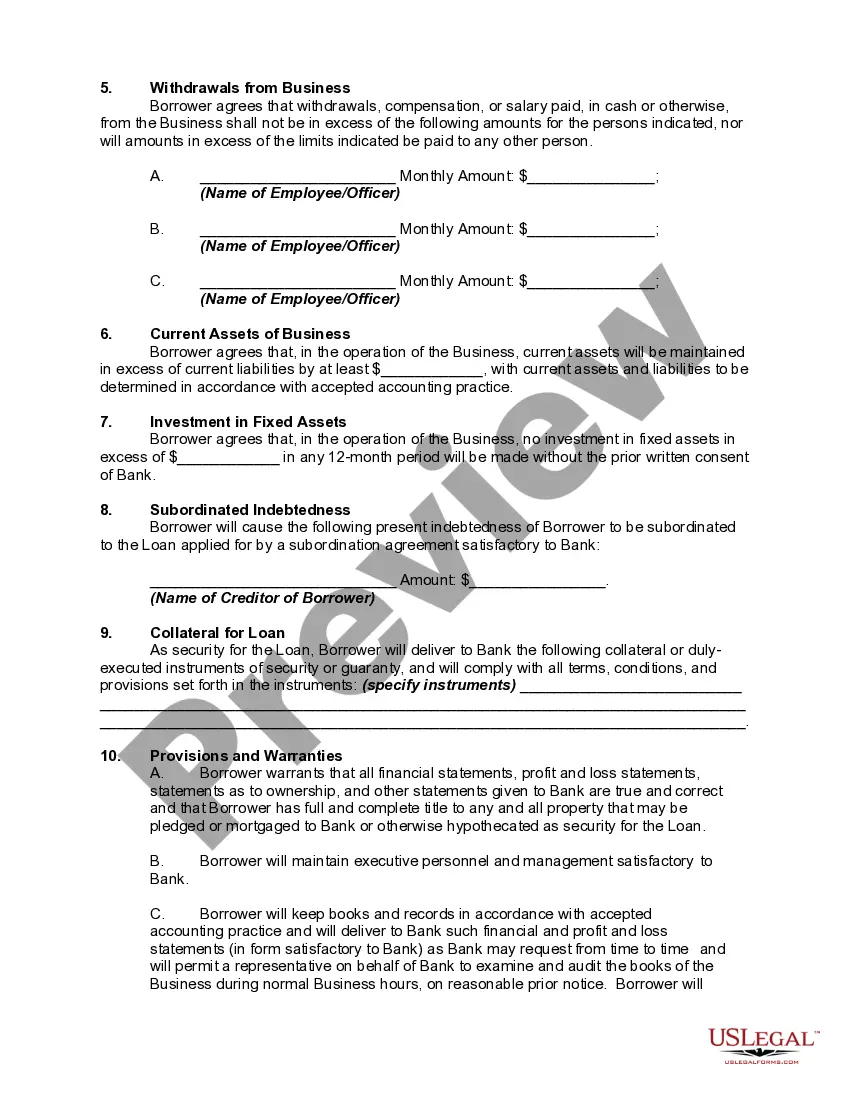

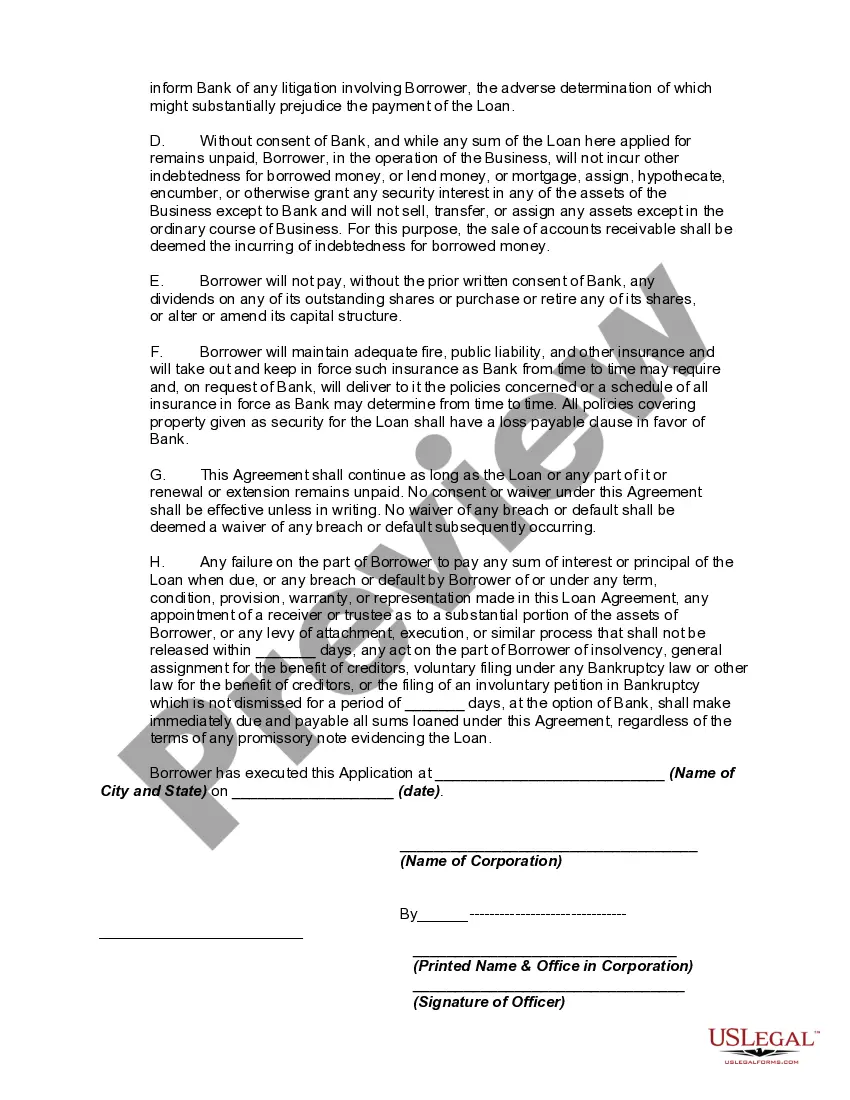

As a general matter, a loan by a bank is the borrowing of money by a person or entity who promises to return it on or before a specific date, with interest, or who pledges collateral as security for the loan and promises to redeem it at a specific later date. Loans are usually made on the basis of applications, together with financial statements submitted by the applicants.

The Federal Truth in Lending Act and the regulations promulgated under the Act apply to certain credit transactions, primarily those involving loans made to a natural person and intended for personal, family, or household purposes and for which a finance charge is made, or loans that are payable in more than four installments. However, said Act and regulations do not apply to a business loan of this type.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

North Carolina Application and Loan Agreement for a Business Loan with Warranties by Borrower The North Carolina Application and Loan Agreement for a Business Loan with Warranties by Borrower is a legal document that outlines the terms and conditions under which a borrower can obtain a business loan in the state of North Carolina. This agreement includes various warranties made by the borrower to ensure the lender's confidence in the loan. Keywords: North Carolina, application, loan agreement, business loan, warranties, borrower. 1. Purpose of the Agreement: The North Carolina Application and Loan Agreement for a Business Loan with Warranties by Borrower is designed to establish the rights and obligations of both the borrower and the lender regarding a business loan application and subsequent loan. It aims to protect the interests of both parties and facilitate a transparent lending process. 2. Key Components: This agreement typically includes the following key components: — Loan Amount: The specified amount of the loan that the borrower is seeking to obtain. — Interest Rate: The rate at which the borrowed amount will accrue interest during the loan term. — Repayment Terms: Details regarding the schedule and method of loan repayment, including any installment amounts or balloon payments. — Use of Funds: Specifies the purpose for which the borrowed funds will be utilized by the borrower. — Security/Collateral: If applicable, outlines any assets or collateral that the borrower is providing as security for the loan. — Warranties: The borrower's assurances and guarantees to the lender, ensuring the accuracy of information provided and affirming compliance with applicable laws. 3. Types of North Carolina Application and Loan Agreement for a Business Loan with Warranties by Borrower: While the North Carolina Application and Loan Agreement for a Business Loan with Warranties by Borrower is a generally recognized document, there may be variations based on the specific lender and borrower requirements. Some possible types include: — Small Business Loan Agreement: Specific to small businesses seeking financial assistance. — Commercial Loan Agreement: Tailored for larger commercial ventures requiring substantial financing. — Startup Loan Agreement: Specifically designed for startups seeking initial capital investment. — Equipment Loan Agreement: Pertains to loans specifically for the purchase of equipment or machinery. In conclusion, the North Carolina Application and Loan Agreement for a Business Loan with Warranties by Borrower is a crucial legal document that helps establish the terms and conditions of a business loan in North Carolina. It provides clarity and protection for both the borrower and the lender, ensuring a smooth and transparent lending process.