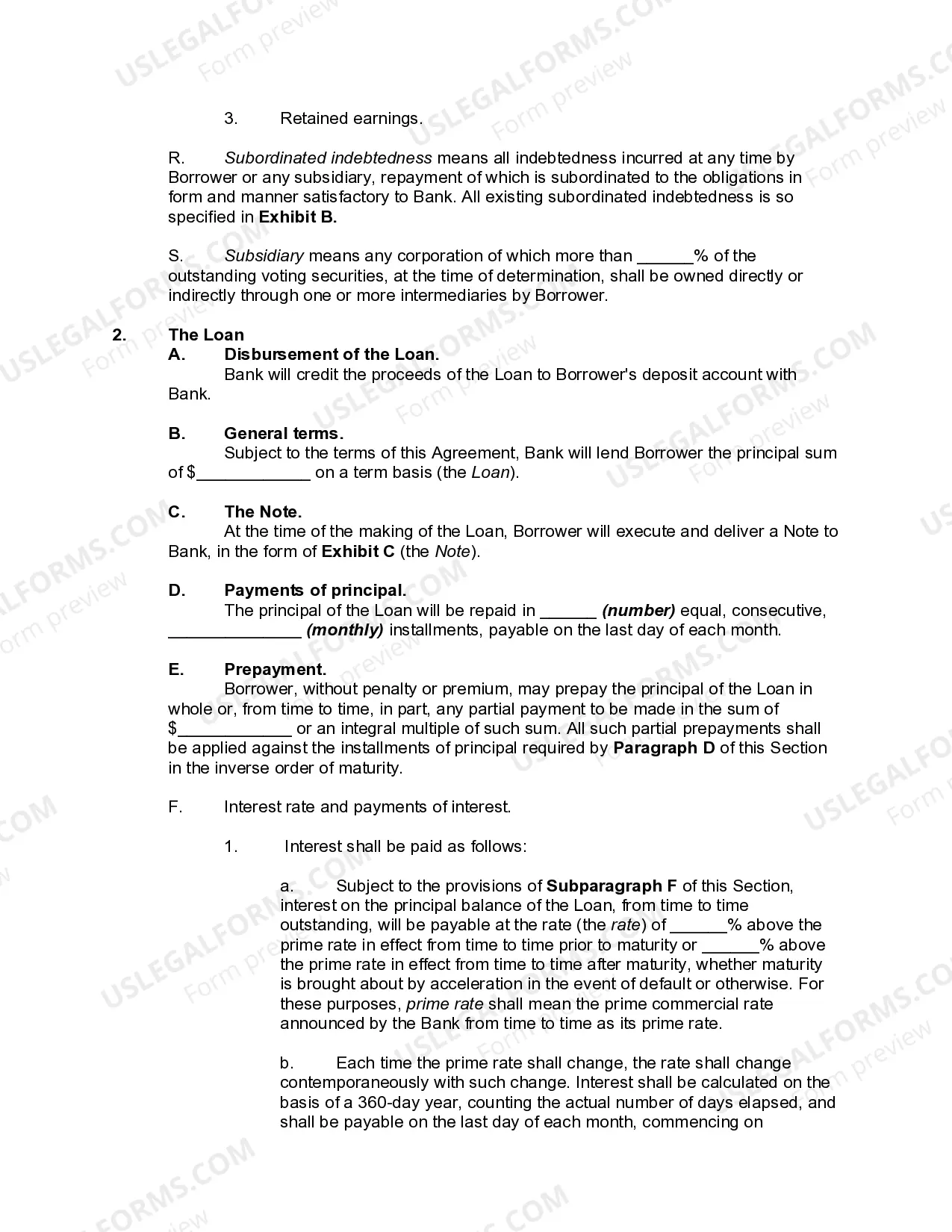

Title: Exploring North Carolina Term Loan Agreements between Business or Corporate Borrowers and Banks Introduction: When a business or corporate entity in North Carolina seeks financial assistance from a bank, a Term Loan Agreement becomes a crucial document defining the terms and conditions of the loan. This article will provide a comprehensive overview of North Carolina Term Loan Agreements between Business or Corporate Borrowers and Banks, shedding light on various types prevalent within the state. 1. Structuring North Carolina Term Loan Agreements: Term Loan Agreements in North Carolina can vary in structure to accommodate specific borrowing needs. These may include: — Fixed-rate Term Loans: These loans feature a defined interest rate that remains constant throughout the loan term, providing borrowers with stable repayment terms. — Variable-rate Term Loans: In contrast to fixed-rate loans, variable-rate Term Loans have interest rates that fluctuate based on market conditions, allowing borrowers to benefit from potential decreases but also posing risks if rates increase. 2. Key Elements within North Carolina Term Loan Agreements: To establish a solid framework, North Carolina Term Loan Agreements typically include the following essential elements: — Loan Amount and Purpose: Clearly states the amount borrowed and describes the intended utilization of funds. — Interest Rates and Fees: Highlights the applicable interest rates, charges, and fees associated with the loan. — Repayment Terms: Specifies the repayment schedule, including the frequency and duration of installments. — Collateral and Guarantees: Outlines the assets or guarantees pledged by the borrower to secure the loan. — Default and Remedies: Defines the consequences and remedies in case of non-payment or default by the borrower. — Events of Default: Lists the circumstances where the agreement may be considered in default, such as bankruptcy or breach of loan covenants. — Prepayment Options: Informs the borrower about provisions allowing early repayment or penalties associated with it. — Dispute Resolution Mechanism: Outlines the process for resolving disputes should they arise during the agreement's term. — Governing Law: Specifies the governing law as North Carolina to maintain consistency with state regulations. 3. Types of North Carolina Term Loan Agreements: a) North Carolina Small Business Term Loan Agreement: Tailored for small businesses, these term loans offer favorable interest rates and flexible repayment terms, providing capital for various purposes such as expansion, inventory management, or working capital needs. b) North Carolina Commercial Term Loan Agreement: Designed for larger corporations or commercial entities, these agreements facilitate significant capital investments, acquisitions, or long-term expansion plans. They often involve higher loan amounts and require more extensive financial documentation. c) North Carolina Equipment Term Loan Agreement: Such agreements focus on providing financing specifically for equipment purchases. Borrowers can procure essential machinery, vehicles, or technologies necessary for their business operations. Conclusion: North Carolina Term Loan Agreements between Business or Corporate Borrowers and Banks play a pivotal role in establishing a mutually beneficial relationship. By understanding the various types of agreements available and the key elements encompassed within them, businesses can make informed decisions to secure the necessary financial support for their growth and development.

North Carolina Term Loan Agreement between Business or Corporate Borrower and Bank

Description

How to fill out North Carolina Term Loan Agreement Between Business Or Corporate Borrower And Bank?

If you want to complete, obtain, or print out legal document web templates, use US Legal Forms, the greatest collection of legal forms, that can be found online. Use the site`s basic and practical search to find the documents you require. Different web templates for organization and individual uses are sorted by types and states, or keywords and phrases. Use US Legal Forms to find the North Carolina Term Loan Agreement between Business or Corporate Borrower and Bank within a handful of mouse clicks.

When you are already a US Legal Forms buyer, log in in your bank account and click the Down load button to get the North Carolina Term Loan Agreement between Business or Corporate Borrower and Bank. You may also entry forms you formerly delivered electronically from the My Forms tab of the bank account.

If you use US Legal Forms the very first time, follow the instructions below:

- Step 1. Be sure you have selected the shape for that right city/region.

- Step 2. Use the Preview option to examine the form`s information. Do not overlook to read through the explanation.

- Step 3. When you are unhappy together with the type, use the Search field near the top of the monitor to find other versions of your legal type format.

- Step 4. When you have discovered the shape you require, click on the Acquire now button. Select the pricing plan you favor and put your accreditations to register on an bank account.

- Step 5. Process the transaction. You can use your bank card or PayPal bank account to complete the transaction.

- Step 6. Select the formatting of your legal type and obtain it on your own product.

- Step 7. Full, revise and print out or indicator the North Carolina Term Loan Agreement between Business or Corporate Borrower and Bank.

Each and every legal document format you purchase is your own eternally. You have acces to every single type you delivered electronically within your acccount. Select the My Forms portion and pick a type to print out or obtain once again.

Compete and obtain, and print out the North Carolina Term Loan Agreement between Business or Corporate Borrower and Bank with US Legal Forms. There are many specialist and condition-distinct forms you can utilize for the organization or individual requires.