North Carolina Promissory Note - Long Form

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Promissory Note - Long Form?

Are you currently in a situation where you frequently require documents for either business or specific uses? There are numerous legal document templates available online, but locating ones you can trust is challenging.

US Legal Forms offers thousands of form templates, such as the North Carolina Promissory Note - Long Form, that are designed to meet federal and state requirements.

If you are already familiar with the US Legal Forms website and possess an account, simply Log In. After that, you can download the North Carolina Promissory Note - Long Form template.

Locate all the document templates you have purchased in the My documents section. You can obtain an additional copy of the North Carolina Promissory Note - Long Form anytime, if needed. Click the desired form to download or print the document template.

Utilize US Legal Forms, the most extensive collection of legal forms, to save time and avoid mistakes. The service provides professionally crafted legal document templates that can be applied for various purposes. Create an account on US Legal Forms and start making your life a bit easier.

- Find the form you need and ensure it corresponds to your specific city/area.

- Utilize the Preview feature to take a look at the form.

- Review the description to confirm that you have chosen the right form.

- If the form does not meet your requirements, use the Search box to find the form that suits your needs.

- Once you find the correct form, click Purchase now.

- Select the pricing plan you wish, fill in the required information to create your account, and pay for your order using your PayPal or credit card.

- Choose a convenient file format and download your copy.

Form popularity

FAQ

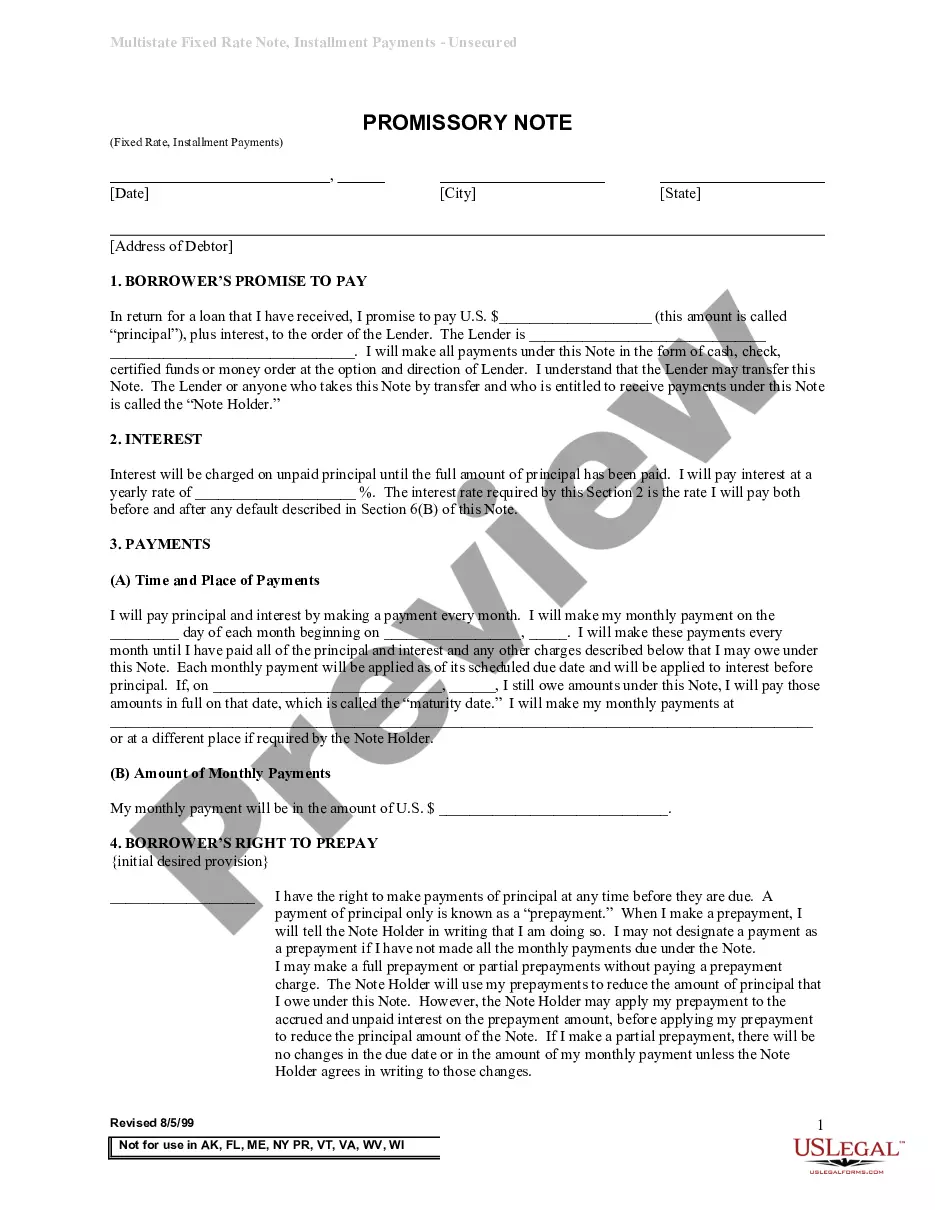

Filling out a promissory note requires specific steps to ensure clarity and legality. Begin by entering the full names and addresses of both the lender and borrower. Then, detail the payment amount, rate of interest, due date, and any default provisions. For a comprehensive approach, the North Carolina Promissory Note - Long Form template from US Legal Forms can provide structure.

The statute of limitations on a promissory note in North Carolina is three years. This means that if a creditor does not file a lawsuit to collect the debt within this time, they may lose the ability to enforce the promissory note. Understanding these time limits is essential when drafting a North Carolina Promissory Note - Long Form, ensuring that both parties adhere to the law.

The length of a promissory note can vary widely, particularly depending on the terms agreed upon by both parties. Generally, a North Carolina Promissory Note - Long Form can span from a few months to several years. This flexibility allows for tailored agreements that suit the unique circumstances of the borrower and lender.

In North Carolina, a debt becomes uncollectible typically after three years, according to the statute of limitations. This timeframe applies to many types of debts, including those represented by promissory notes. It is vital to be aware of these limits when dealing with a North Carolina Promissory Note - Long Form to ensure proper legal recourse.

Promissory notes can be either short-term or long-term depending on the agreement between the parties involved. Typically, a long-term promissory note spans several years, while short-term notes may be due within months. For creating a long-term commitment, consider using a North Carolina Promissory Note - Long Form, which clearly outlines the terms and durations.

Yes, there is a time limit on a promissory note enforced by the statute of limitations in North Carolina. Generally, the time limit is three years for most promissory notes, after which a creditor may lose the right to pursue collection. Being aware of these limits can help both parties make informed financial decisions when drafting a North Carolina Promissory Note - Long Form.

A promissory note in North Carolina does not have a stipulated expiration date; however, it is subject to the statute of limitations. This means that while the note itself can remain valid, specific legal actions to collect on it must be initiated within a certain timeframe. Thus, it is important for borrowers and lenders to understand their rights and responsibilities under the North Carolina Promissory Note - Long Form.

A North Carolina Promissory Note - Long Form does not necessarily require notarization to be valid. However, notarizing a promissory note can provide additional legal protection and clarity. It is best to check local laws and consult legal advice to ensure the note meets all necessary requirements. Remember, clarity and proper documentation benefit all parties involved.

You can easily obtain a promissory note through legal form platforms like uslegalforms. They provide the North Carolina Promissory Note - Long Form, which you can download, fill out, and customize to suit your needs. This approach saves time and helps ensure you include all necessary terms and conditions.

As previously mentioned, you typically do not need a lawyer to create a promissory note. The North Carolina Promissory Note - Long Form simplifies the process and is designed for easy use. Nevertheless, if you have unique circumstances or want peace of mind, seeking legal advice can be beneficial.