North Carolina Loan Guaranty Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Guaranty Agreement?

Discovering the right authorized document web template might be a have difficulties. Obviously, there are a variety of web templates available on the Internet, but how will you get the authorized develop you want? Use the US Legal Forms web site. The support delivers a huge number of web templates, for example the North Carolina Loan Guaranty Agreement, which can be used for enterprise and private needs. Each of the kinds are checked by pros and fulfill state and federal needs.

If you are currently authorized, log in to your accounts and then click the Obtain button to have the North Carolina Loan Guaranty Agreement. Make use of your accounts to search from the authorized kinds you might have purchased in the past. Go to the My Forms tab of your accounts and have one more copy from the document you want.

If you are a fresh customer of US Legal Forms, here are straightforward guidelines for you to stick to:

- Initial, make certain you have selected the correct develop for your personal city/region. It is possible to look through the form utilizing the Preview button and read the form information to ensure this is basically the best for you.

- If the develop is not going to fulfill your expectations, take advantage of the Seach discipline to obtain the appropriate develop.

- Once you are certain the form is suitable, select the Acquire now button to have the develop.

- Choose the costs program you want and enter the essential information. Build your accounts and purchase the order making use of your PayPal accounts or bank card.

- Choose the document file format and download the authorized document web template to your product.

- Total, modify and produce and indicator the received North Carolina Loan Guaranty Agreement.

US Legal Forms will be the greatest library of authorized kinds in which you will find a variety of document web templates. Use the service to download appropriately-manufactured paperwork that stick to state needs.

Form popularity

FAQ

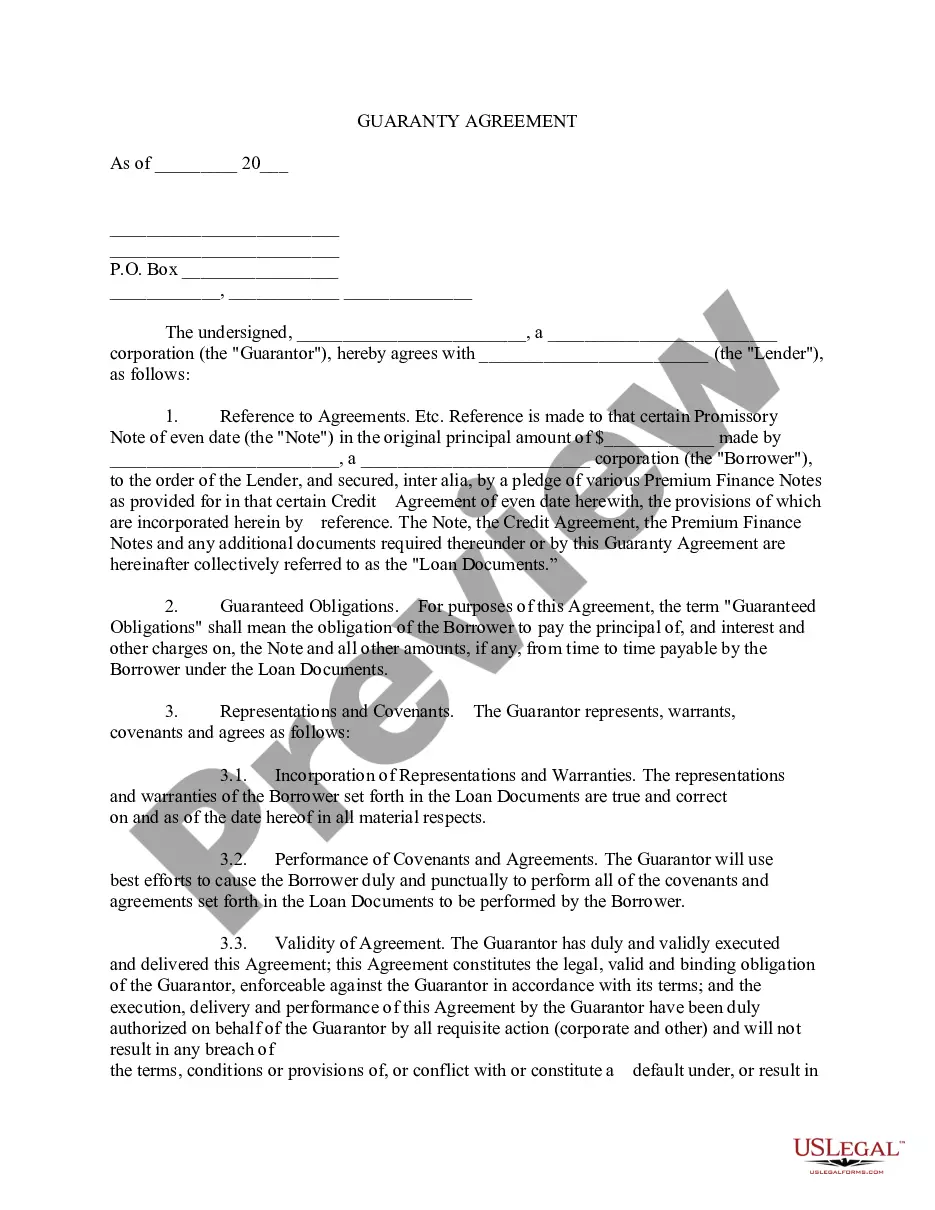

A guarantor contracts to pay if, by the use of due diligence, the debt cannot be paid by the principal debtor. The surety undertakes directly for the payment. The surety is responsible at once if the principal debtor defaults. In other words, a guaranty is an undertaking that the debtor shall pay.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

A promissory note is a written promise to pay back money. These legally binding agreements typically include debt repayment terms?like payment schedules and interest rates.

Although it is legally enforceable, a promissory note is less formal than a loan agreement and is suitable where smaller sums of money are involved. However, its terms - which can include a specific date of repayment, interest rate and repayment schedule - are more certain than those of an IOU.

It is a legally binding personal promise to step into the shoes of the original party to the contract. For example, an individual may personally agree to pay off the debts of a company they are acquiring as part of the acquisition.

In a finance or lending context, a guarantor would be forced to answer for the debt or default of the debtor to the creditor, if a debtor does not fulfill an obligation on their part to repay their debt.

A promissory note entails an individual's commitment to the business to make payments on a specific date. On the other hand, a personal guarantee entails a contract an individual signs up for to stand in for the company's debt if they fail to repay the loans within a given period.

A loan guarantee is a legally binding commitment to pay a debt in the event the borrower defaults. This most often occurs between family members, where the borrower can't obtain a loan because of a lack of income or down payment, or due to a poor credit rating.