North Carolina Loan Agreement for Vehicle

Description

How to fill out Loan Agreement For Vehicle?

If you wish to complete, acquire, or print legal record templates, use US Legal Forms, the largest variety of legal varieties, which can be found online. Use the site`s basic and convenient lookup to discover the papers you require. Numerous templates for company and specific functions are categorized by classes and claims, or key phrases. Use US Legal Forms to discover the North Carolina Loan Agreement for Vehicle within a number of mouse clicks.

In case you are presently a US Legal Forms customer, log in for your account and then click the Obtain button to have the North Carolina Loan Agreement for Vehicle. You can also entry varieties you earlier downloaded inside the My Forms tab of your own account.

Should you use US Legal Forms for the first time, refer to the instructions below:

- Step 1. Ensure you have selected the shape for your appropriate metropolis/region.

- Step 2. Use the Preview method to look through the form`s content. Don`t neglect to learn the explanation.

- Step 3. In case you are unhappy with all the develop, use the Search discipline at the top of the display screen to locate other types from the legal develop design.

- Step 4. Once you have found the shape you require, select the Acquire now button. Choose the pricing plan you favor and add your credentials to sign up to have an account.

- Step 5. Approach the transaction. You should use your bank card or PayPal account to complete the transaction.

- Step 6. Select the format from the legal develop and acquire it on your own device.

- Step 7. Comprehensive, edit and print or indication the North Carolina Loan Agreement for Vehicle.

Each legal record design you buy is yours permanently. You might have acces to each develop you downloaded with your acccount. Go through the My Forms section and decide on a develop to print or acquire once again.

Contend and acquire, and print the North Carolina Loan Agreement for Vehicle with US Legal Forms. There are millions of skilled and status-certain varieties you can utilize for your company or specific requires.

Form popularity

FAQ

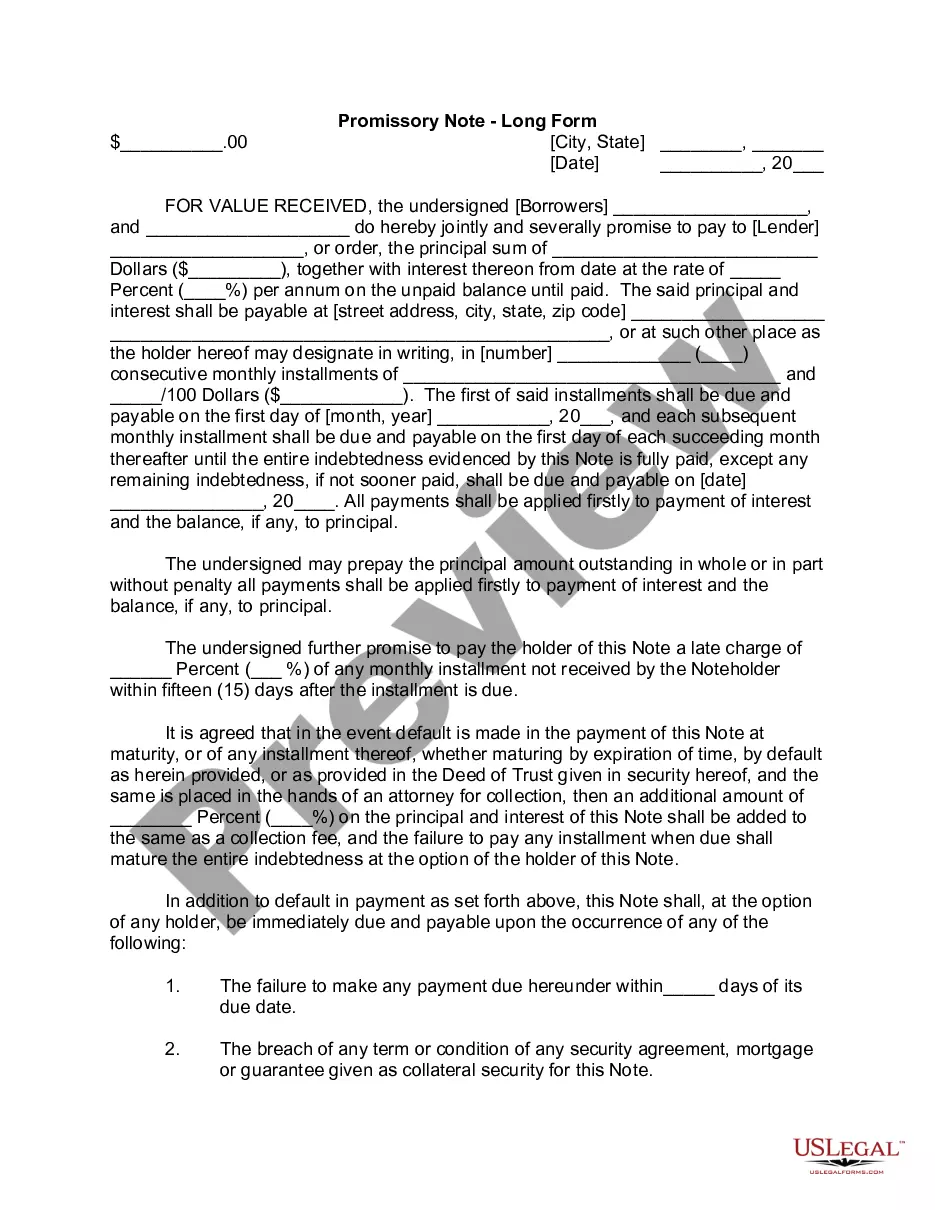

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

State what each side agrees to do. Clearly write out the terms of the loan. Include information about the date of the loan, the payment terms, interest, schedule of payments, late charges, default, and any other details in the agreement. Explain that the contract represents the entire agreement.

Car Promissory Note With a ca promissory note, a borrower promises to make payments on a car loan in exchange for a vehicle. The borrower typically makes even payments throughout the car loan term but often makes an initial lmp sum down payment.

A promissory note is a written agreement between a borrower and a lender saying that the borrower will pay back the amount borrowed plus interest. The promissory note is issued by the lender and is signed by the borrower (but not the lender).

Rejoice! You Can Get a Car Loan in North Carolina.

PROMISE TO PAY Definition & Legal Meaning An agreement between two parties, the lender and the borrower, in which the lender promises to pay a set amount of money on a set date. Usually made if the lender is behind in payments or payment is overdue.

To draft a Loan Agreement, you should include the following: The addresses and contact information of all parties involved. The conditions of use of the loan (what the money can be used for) Any repayment options. The payment schedule. The interest rates.

A promissory note is a written promise from one person or business to pay another. Also known as loan agreements or IOUs, these documents lay out the terms and conditions of a loan and ensure that the agreement is legally enforceable.