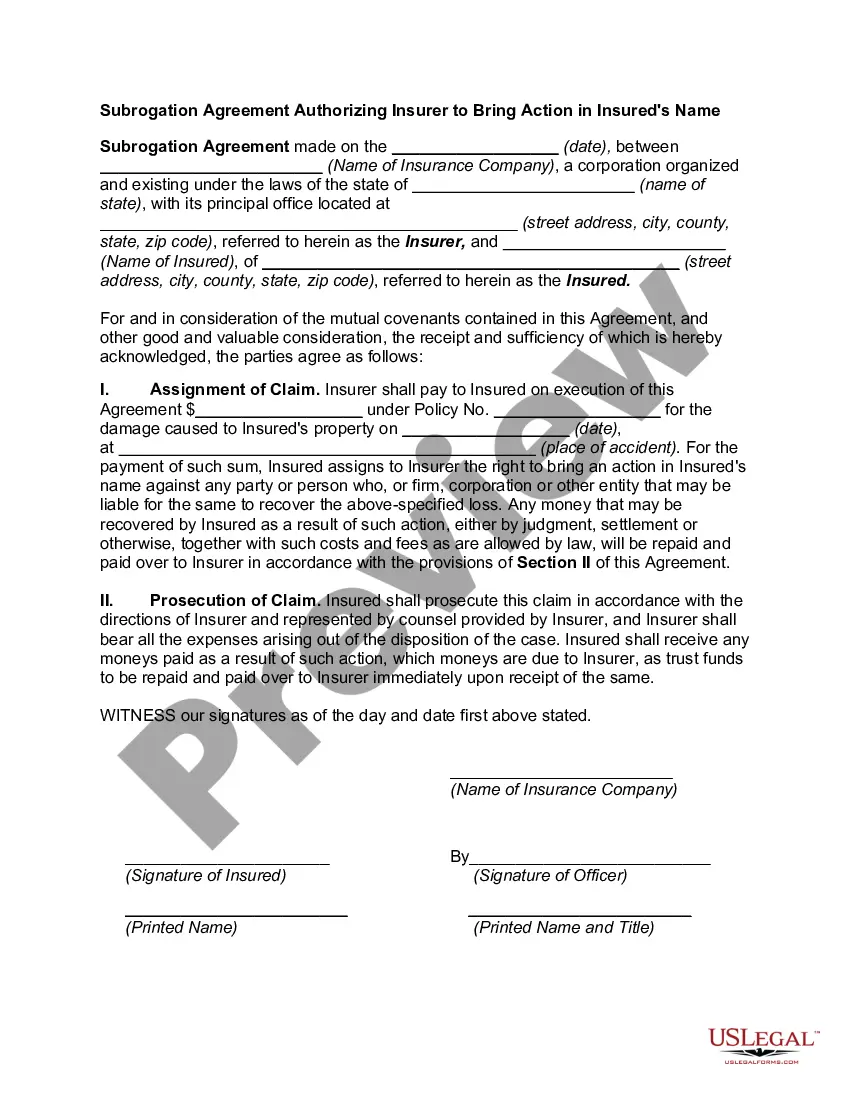

Title: Understanding the North Carolina Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name Introduction: In North Carolina, subrogation agreements are legal contracts that give insurers the right to step into their insured's shoes and pursue legal action against a third party who may be responsible for an accident or damage. This detailed description will provide insights into the purpose, types, and requirements of the North Carolina Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name. 1. Definition of a Subrogation Agreement: A subrogation agreement is a contractual provision that allows an insurance company to seek compensation on behalf of its insured, ultimately safeguarding the interests of the insurer and ensuring fairness for the policyholder. 2. Purpose and Benefits: The primary objective of the North Carolina Subrogation Agreement is to hold the responsible party accountable for their actions or negligence, helping to recover damages from the other party's insurance or personal assets. By pursuing subrogation, insurers can minimize their claim expenses and potentially reduce the overall cost of insurance for policyholders. 3. Types of North Carolina Subrogation Agreements: a. Auto Insurance Subrogation Agreement: Specifically designed for auto insurance, this type of subrogation agreement allows insurers to pursue claims against individuals responsible for causing an accident, property damage, or bodily injury related to motor vehicle incidents. b. Property Insurance Subrogation Agreement: Unique to property insurance policies, this agreement enables insurers to recover damages from third parties responsible for property loss or damage, such as fires, natural disasters, or vandalism. c. Medical Insurance Subrogation Agreement: In cases involving medical insurance, this type of subrogation agreement empowers insurers to recover costs associated with medical accidents or injuries caused by another party's negligence or liability. 4. Key Elements of a Subrogation Agreement: To be legally valid and enforceable in North Carolina, a Subrogation Agreement Authorizing Insurer to Bring Action in the Insured's Name must include the following essential elements: a. Parties Involved: Clearly identify and state the names and addresses of the insurer, insured, and any potential third parties. b. Legal Basis: Specify the grounds on which the insurer is seeking subrogation, such as fault, breach of contract, or negligence. c. Policy Details: Provide comprehensive information regarding the insurance policy, including policy number, effective date, coverage details, and limits. d. Authorization Scope: Clearly define the authority granted to the insurer to initiate legal proceedings, settle claims, or negotiate on behalf of the insured. e. Rights and Responsibilities: Outline the responsibilities of both the insurer and the insured throughout the subrogation process, including the cooperation and notification requirements. f. Reimbursement and Recovery: Describe the mechanism for reimbursement of the insurer's expenses and the distribution of recovered funds, ensuring clarity on any cost-sharing arrangements. Conclusion: The North Carolina Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name is a powerful tool that allows insurers to protect their interests by stepping in on behalf of their insured to pursue claims against responsible parties. By understanding the different types and requirements of these agreements, insurers and policyholders can navigate the subrogation process with confidence, ensuring fair treatment and potential cost reduction for all parties involved.

North Carolina Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name

Description

How to fill out North Carolina Subrogation Agreement Authorizing Insurer To Bring Action In Insured's Name?

Choosing the best authorized document format can be quite a battle. Of course, there are tons of layouts available on the net, but how can you get the authorized kind you require? Use the US Legal Forms website. The support offers thousands of layouts, including the North Carolina Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name, that can be used for business and private requires. Every one of the kinds are inspected by pros and meet state and federal requirements.

If you are currently listed, log in for your account and then click the Down load key to obtain the North Carolina Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name. Make use of account to look with the authorized kinds you possess purchased in the past. Visit the My Forms tab of the account and acquire yet another duplicate of your document you require.

If you are a whole new customer of US Legal Forms, allow me to share easy guidelines for you to adhere to:

- First, make certain you have selected the proper kind to your area/area. You may check out the form using the Review key and study the form outline to make sure it will be the best for you.

- In the event the kind will not meet your expectations, use the Seach industry to obtain the appropriate kind.

- Once you are positive that the form is acceptable, select the Buy now key to obtain the kind.

- Choose the costs plan you want and type in the needed details. Create your account and purchase the transaction with your PayPal account or bank card.

- Pick the submit format and acquire the authorized document format for your gadget.

- Full, revise and printing and signal the obtained North Carolina Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name.

US Legal Forms is the biggest library of authorized kinds that you can discover different document layouts. Use the service to acquire expertly-produced documents that adhere to state requirements.

Form popularity

FAQ

North Carolina is unique, as the state strictly prohibits subrogation language or clauses in privately funded health insurance policies. This means that North Carolina insurance companies are not able to receive a subrogation interest in your personal injury recovery.

Subrogation allows your insurer to recoup costs (medical payments, repairs, etc.), including your deductible, from the at-fault driver's insurance company, if the accident wasn't your fault. A successful subrogation means a refund for you and your insurer.

While liens involve a claim against a third-party recovery, subrogation is a distinct concept. In subrogation, the entity that covered the loss has the right to go directly against the responsible third party. This benefit provider "steps into the shoes" of the injured party for purposes of pursuing reimbursement.

Essentially, the principle of subrogation permits one (i.e., the insurer) who is legally obligated to pay the debt of another to "stand in the shoes" of the person owed payment (i.e., the insured) and enforce that person's right against the actual wrongdoer.

A subrogation receipt transferring the insured's entire causes of action to the insurer allows the insurer to recover in the insured's name for the entire loss, not just to the extent of its payment.

North Carolina is unique, as the state strictly prohibits subrogation language or clauses in privately funded health insurance policies. This means that North Carolina insurance companies are not able to receive a subrogation interest in your personal injury recovery.

North Carolina General Statute § 97-10.2 even creates a right for the workers' compensation carrier to seek subrogation against the third party independently. ing to the statute, the injured employee has the exclusive right to file a suit against the third-party for twelve (12) months.

North Carolina's ?anti-subrogation rule? means that privately funded health insurance policies in North Carolina will not be able to seek and receive reimbursement (also known as ?subrogation?) from your personal injury recovery.