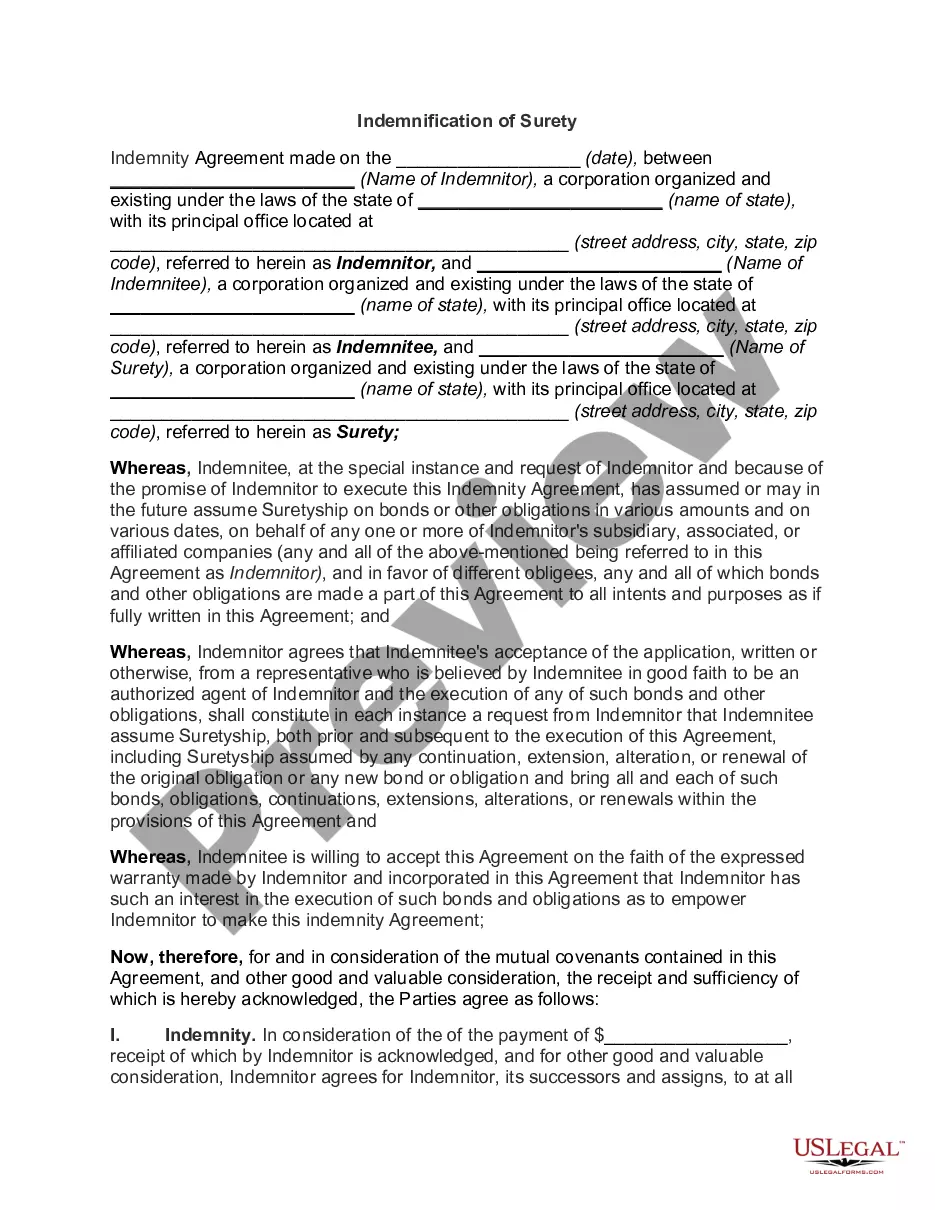

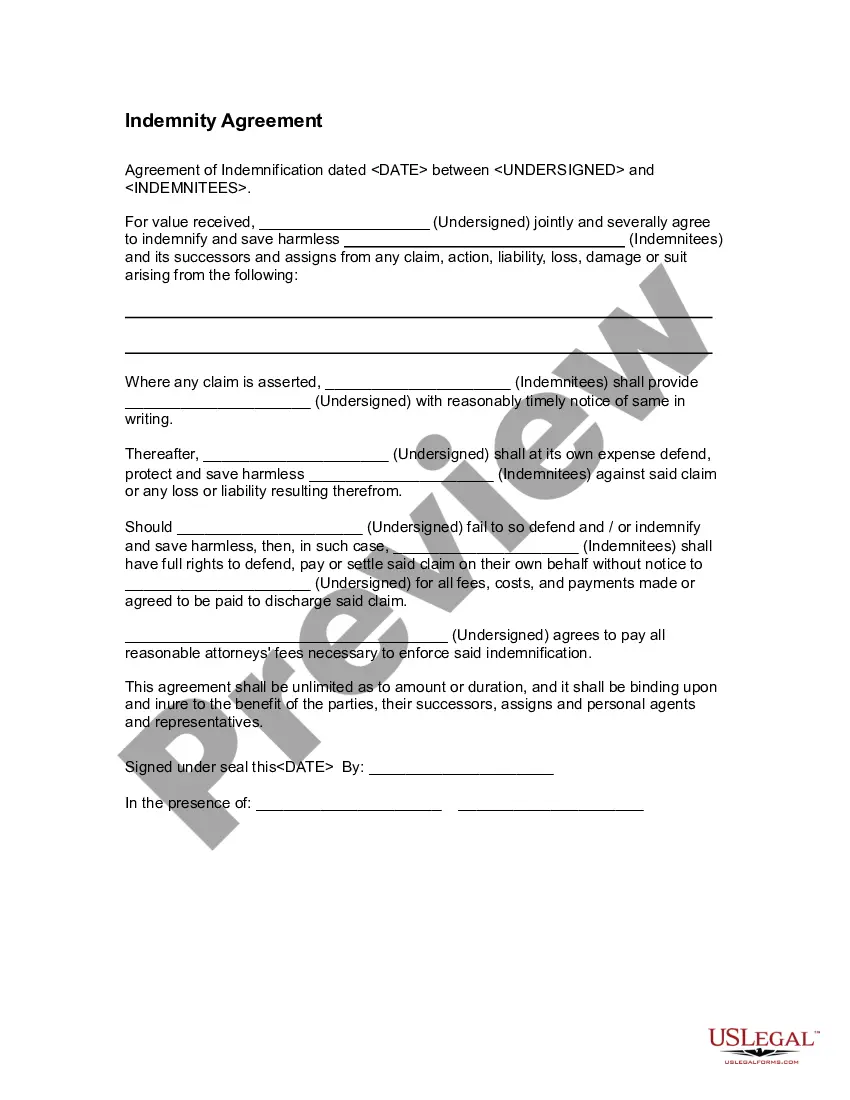

North Carolina Surety Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Surety Agreement?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a variety of legal template formats that you can download or print. By using the site, you'll find thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can quickly access the most recent versions of forms like the North Carolina Surety Agreement in just seconds.

If you have a subscription, Log In and download the North Carolina Surety Agreement from the US Legal Forms library. The Download button will appear on every form you view. You can access all previously downloaded forms in the My documents section of your account.

Choose the format and download the form to your device.

Edit. Complete, modify, print, and sign the downloaded North Carolina Surety Agreement. All templates you added to your account do not expire and are yours indefinitely. Therefore, if you wish to download or print another copy, just go to the My documents section and click on the form you desire.

- Ensure you have selected the correct form for your region/county. Click the Preview button to review the content of the form.

- Check the form details to make sure you have chosen the right document.

- If the form does not meet your criteria, use the Search field at the top of the screen to find one that does.

- When you are satisfied with the form, confirm your choice by clicking on the Get Now button.

- Then, select the pricing plan you prefer and provide your details to sign up for an account.

- Process the payment. Use your credit card or PayPal account to complete the transaction.

Form popularity

FAQ

To complete a surety form, first gather all necessary documents that may be required, such as identification and proof of financial capability. Next, methodically fill out the form, ensuring to provide accurate details regarding all parties involved in the North Carolina Surety Agreement. If you're uncertain about any aspect, US Legal Forms offers resources that simplify the completion process, making it more accessible for you.

Surety Bonds are contracts guaranteeing that specific obligations will be fulfilled. The obligation may involve meeting a contractual commitment, paying a debt or performing certain duties. Under the terms of a bond, one party becomes answerable to a third party for the acts or non-performance of a second party.

You can now apply for a surety online or via the phone. What you will need is information about yourself and your business, the type of bond that you require, and your financial information. The surety company will then review your application and determine your eligibility for a bond.

North Carolina contractors are often required to post a surety bond as a condition of a license or permit by local municipalities, counties, or the state government. Bond amounts are based on the type and volume of work performed.

Someone who assumes direct liability for another's obligation. Financial creditors may require the debtor to find a surety, who then signs the loan agreement along with the debtor.

These bond types are also referred to as commercial bonds" or business bonds." Examples of license and permit surety bonds include auto dealer bonds, mortgage broker bonds, and collection agency bonds.

Lottery bonds lottery retailers in North Carolina are typically required to be bonded when carrying out their services. The bond ensures that retailers will properly remit payments from the sale of lottery tickets to the required parties, and as specified in the contract.

Surety Explained in Detail A surety bond is a legal binding agreement signed between three partiesthe lender, the trustee, and the guarantor. The obligee, generally a government agency, allows the principal to receive a security bond as a protection against future work output, normally a business owner or contractor.

Bonds up to $5,000 are issued instantly and cost $100. Bonds up to $25,000 are also issued instantly, but the cost is calculated at a rate of $20 per $1,000 of coverage. If you need a bond larger than $25,000, your premium will be determined by an underwriter.

The surety is the guarantee of the debts of one party by another. A surety is an organization or person that assumes the responsibility of paying the debt in case the debtor policy defaults or is unable to make the payments. The party that guarantees the debt is referred to as the surety, or as the guarantor.