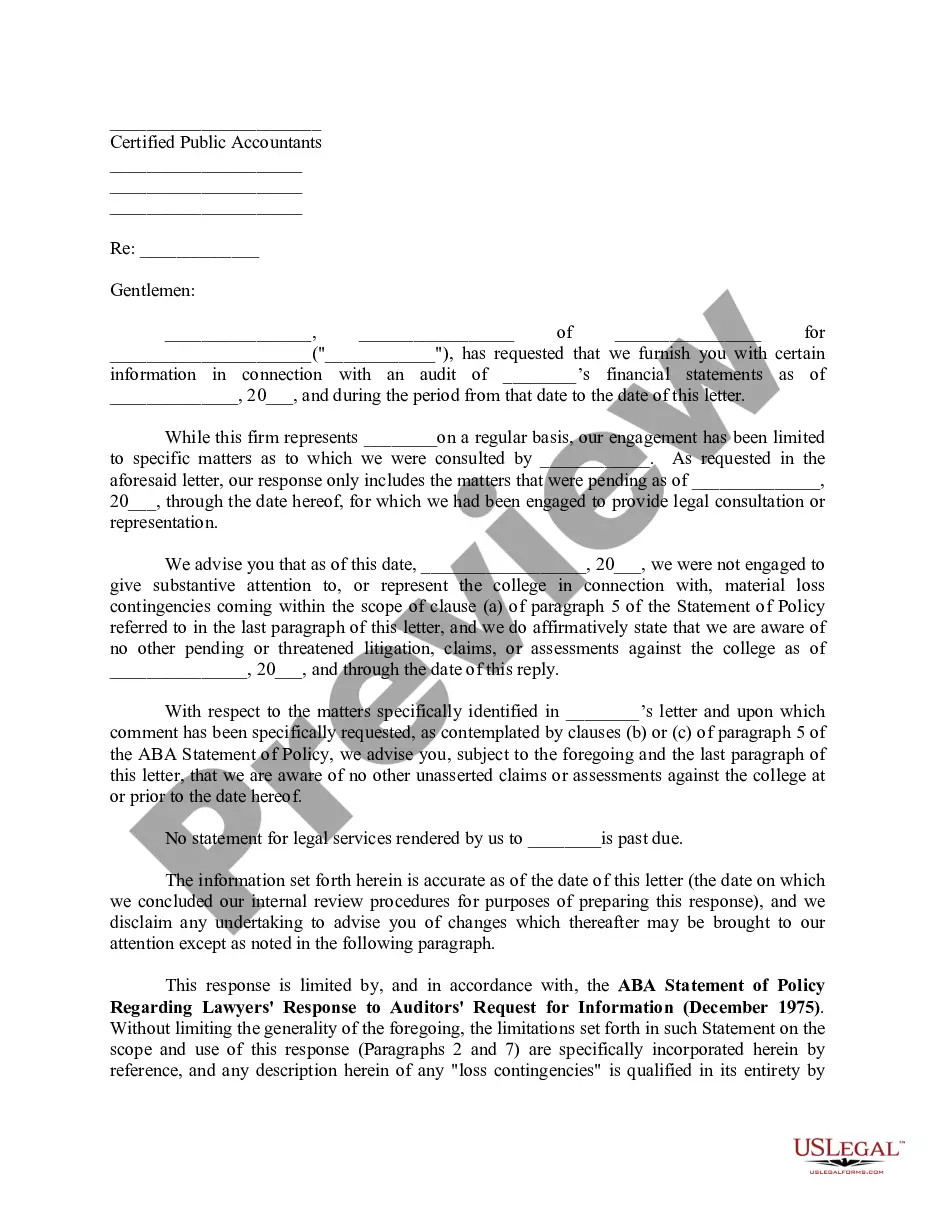

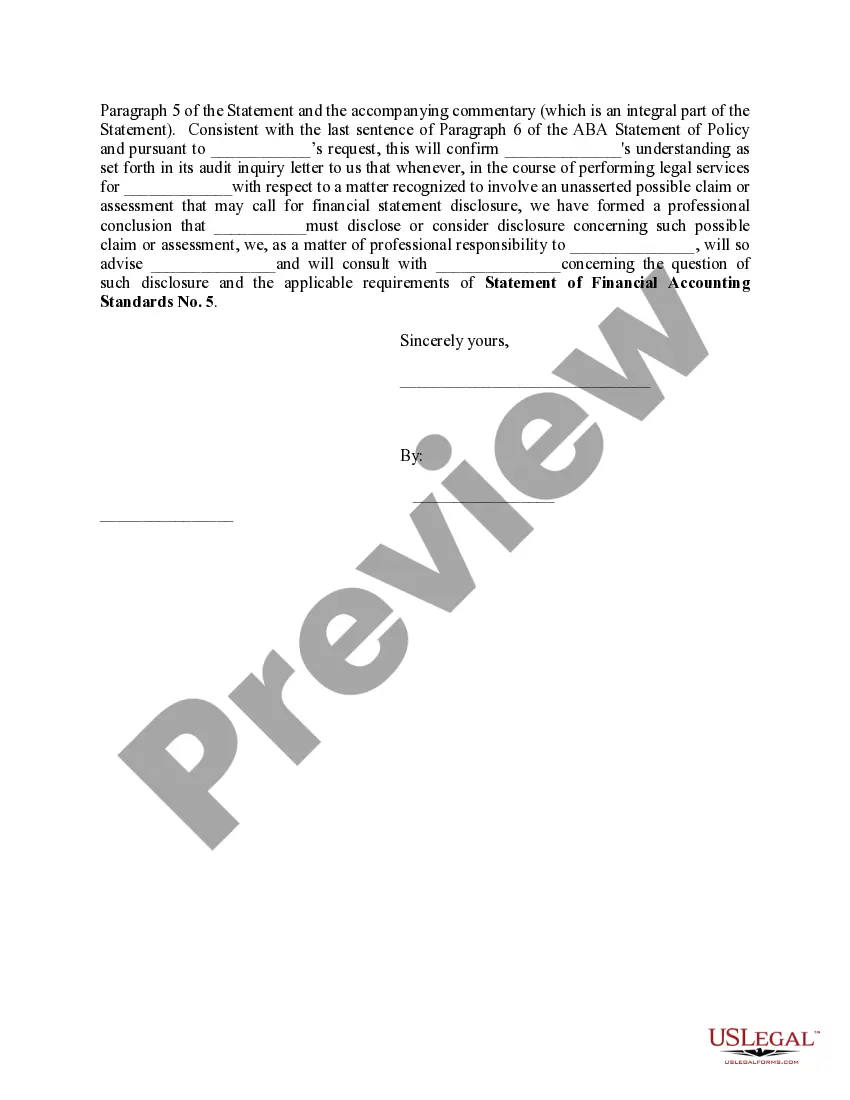

Title: North Carolina Model Letter Accountants To Auditors: An In-Depth Guide Introduction: North Carolina Model Letter Accountants To Auditors is a comprehensive set of templates designed to facilitate effective communication between accountants and auditors operating within the state of North Carolina. These model letters serve as a professional and standardized means for exchanging relevant information, requests, and recommendations in the audit process. They are particularly valuable in ensuring efficient cooperation, meeting regulatory requirements, and ensuring accurate financial reporting. Types of North Carolina Model Letter Accountants To Auditors: 1. Engagement Letter: The engagement letter is an integral part of the auditor-client relationship. It outlines the scope of work, responsibilities, and terms of engagement between the accountant and auditor. This letter establishes clear expectations, mitigates risks, and governs the professional relationship throughout the audit engagement. 2. Request for Information Letter: A request for information letter is an essential communication tool in the audit process. It enables accountants to request specific data, documents, or supporting evidence from auditors. The letter should be concise, clearly stating the requested information, its purpose, and a reasonable timeframe for response. 3. Management Representation Letter: The management representation letter is essential for gathering assurance from the entity's management regarding the completeness, accuracy, and integrity of financial statements. It emphasizes management's commitment and responsibility for overseeing the entity's financial affairs and the fairness of the presented financial information. 4. Inquiry Letter: An inquiry letter is employed by the accountants to request information or explanation about specific transactions, events, or controls from auditors. It seeks clarification on matters that may help to further understand the financial statements, identify anomalies, or address potential risks. 5. Accountant's Comment Letter: The accountant's comment letter is used to provide professional feedback, concerns, or observations regarding audit planning, procedures, or findings. This letter aims to foster collaboration between the accountant and auditor by addressing any areas of disagreement, suggesting improvements, or raising any significant issues that may impact the financial reporting. Conclusion: North Carolina Model Letter Accountants To Auditors play a crucial role in establishing open and transparent communication channels between accountants and auditors. These standardized templates ensure that exchanges are consistent, efficient, and compliant with North Carolina's regulatory framework. By utilizing these model letters, accountants and auditors can enhance their collaboration, guarantee the accuracy of financial reporting, and uphold the integrity of the auditing process.

North Carolina Model Letter Accountants To Auditors

Description

How to fill out North Carolina Model Letter Accountants To Auditors?

Have you been in the place in which you need files for sometimes organization or personal purposes just about every time? There are tons of legitimate document themes available on the net, but discovering types you can rely on isn`t effortless. US Legal Forms gives thousands of form themes, like the North Carolina Model Letter Accountants To Auditors, that happen to be created to satisfy state and federal requirements.

When you are presently knowledgeable about US Legal Forms site and also have a free account, just log in. Next, it is possible to acquire the North Carolina Model Letter Accountants To Auditors design.

If you do not provide an account and want to start using US Legal Forms, adopt these measures:

- Find the form you will need and make sure it is for your proper town/area.

- Utilize the Preview option to examine the form.

- Read the explanation to actually have chosen the appropriate form.

- If the form isn`t what you`re looking for, make use of the Search field to discover the form that fits your needs and requirements.

- When you find the proper form, click Purchase now.

- Pick the prices program you desire, fill out the required info to produce your account, and purchase your order making use of your PayPal or bank card.

- Select a convenient file file format and acquire your duplicate.

Get all the document themes you have purchased in the My Forms food selection. You can aquire a further duplicate of North Carolina Model Letter Accountants To Auditors whenever, if required. Just click the essential form to acquire or produce the document design.

Use US Legal Forms, the most comprehensive variety of legitimate varieties, to save lots of some time and steer clear of blunders. The assistance gives professionally manufactured legitimate document themes which you can use for a variety of purposes. Generate a free account on US Legal Forms and begin creating your life a little easier.