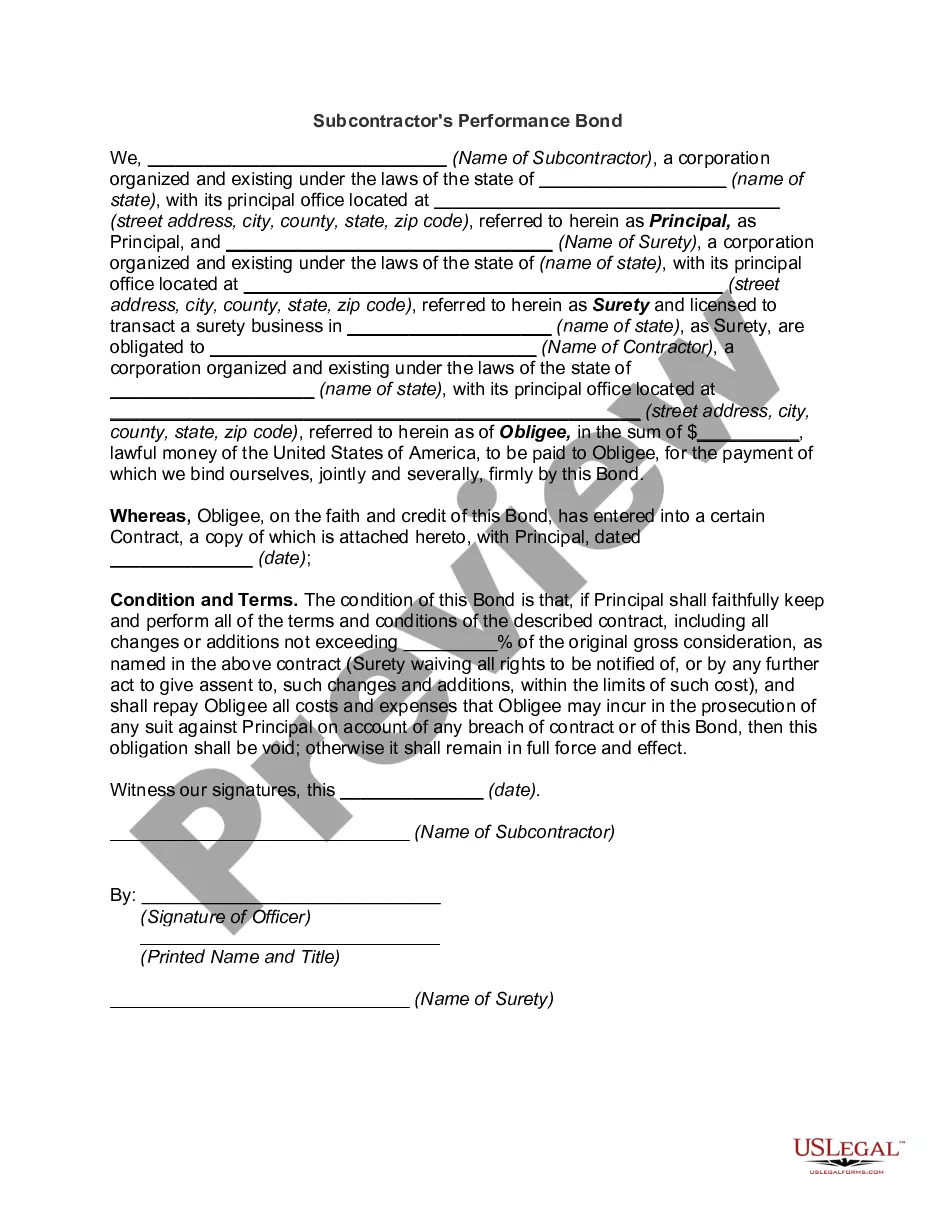

A North Carolina Subcontractor's Performance Bond is a type of surety bond required by the state of North Carolina for subcontractors engaged in construction projects. It acts as a guarantee that the subcontractor will fulfill their contractual obligations and complete the project according to the terms specified in the contract. Performance bonds are essential to protect the project owner or general contractor from any potential losses or damages that may arise due to default or inadequate performance by the subcontractor. The bond ensures that the project will be completed as planned, even if the subcontractor fails to meet their responsibilities. In North Carolina, there are two main types of Subcontractor's Performance Bonds: 1. Bid Bond: A bid bond is typically requested during the bidding process for a construction project. It assures the project owner that the subcontractor has the financial capability and expertise to perform the work if they are awarded the contract. If the subcontractor fails to honor their bid or withdraws it, the bond provides compensation to the project owner for any additional costs incurred in re-bidding the project. 2. Performance Bond: Once the subcontractor has been awarded the contract, a performance bond is required to ensure the completion of the project in accordance with the agreed-upon terms. If the subcontractor fails to perform their obligations, such as delays, defective work, or non-compliance with specifications, the bond provides financial protection to the project owner. It covers any additional expenses the owner incurs to complete the project or rectify any deficiencies. Both the bid bond and performance bond are typically issued by a surety company that specializes in providing bonds. The subcontractor is responsible for the premium associated with obtaining the bond, which is usually a percentage of the total bond amount. In summary, a North Carolina Subcontractor's Performance Bond is a vital component of construction projects, providing assurance to project owners that subcontractors will adhere to their contractual obligations. The bid bond secures the bidding process, while the performance bond guarantees the completion of the project as per the contract. By requiring these bonds, North Carolina aims to safeguard both project owners and subcontractors, ensuring the successful execution of construction projects.

North Carolina Subcontractor's Performance Bond

Description

How to fill out North Carolina Subcontractor's Performance Bond?

You can spend several hours on the Internet trying to find the legal document format which fits the state and federal requirements you need. US Legal Forms offers a huge number of legal types which can be evaluated by professionals. It is simple to download or printing the North Carolina Subcontractor's Performance Bond from our assistance.

If you have a US Legal Forms account, it is possible to log in and click the Down load option. Afterward, it is possible to complete, revise, printing, or indication the North Carolina Subcontractor's Performance Bond. Every single legal document format you buy is your own eternally. To obtain one more backup for any acquired type, go to the My Forms tab and click the related option.

If you work with the US Legal Forms internet site for the first time, stick to the easy instructions beneath:

- Initially, make certain you have chosen the proper document format for the state/town of your choice. Look at the type outline to ensure you have picked the appropriate type. If available, make use of the Review option to look throughout the document format at the same time.

- If you would like discover one more model of your type, make use of the Research field to obtain the format that meets your requirements and requirements.

- Once you have found the format you want, click Get now to proceed.

- Choose the prices program you want, key in your credentials, and sign up for a free account on US Legal Forms.

- Complete the purchase. You may use your bank card or PayPal account to pay for the legal type.

- Choose the format of your document and download it in your gadget.

- Make modifications in your document if necessary. You can complete, revise and indication and printing North Carolina Subcontractor's Performance Bond.

Down load and printing a huge number of document themes using the US Legal Forms Internet site, which provides the biggest assortment of legal types. Use specialist and condition-certain themes to tackle your small business or specific demands.