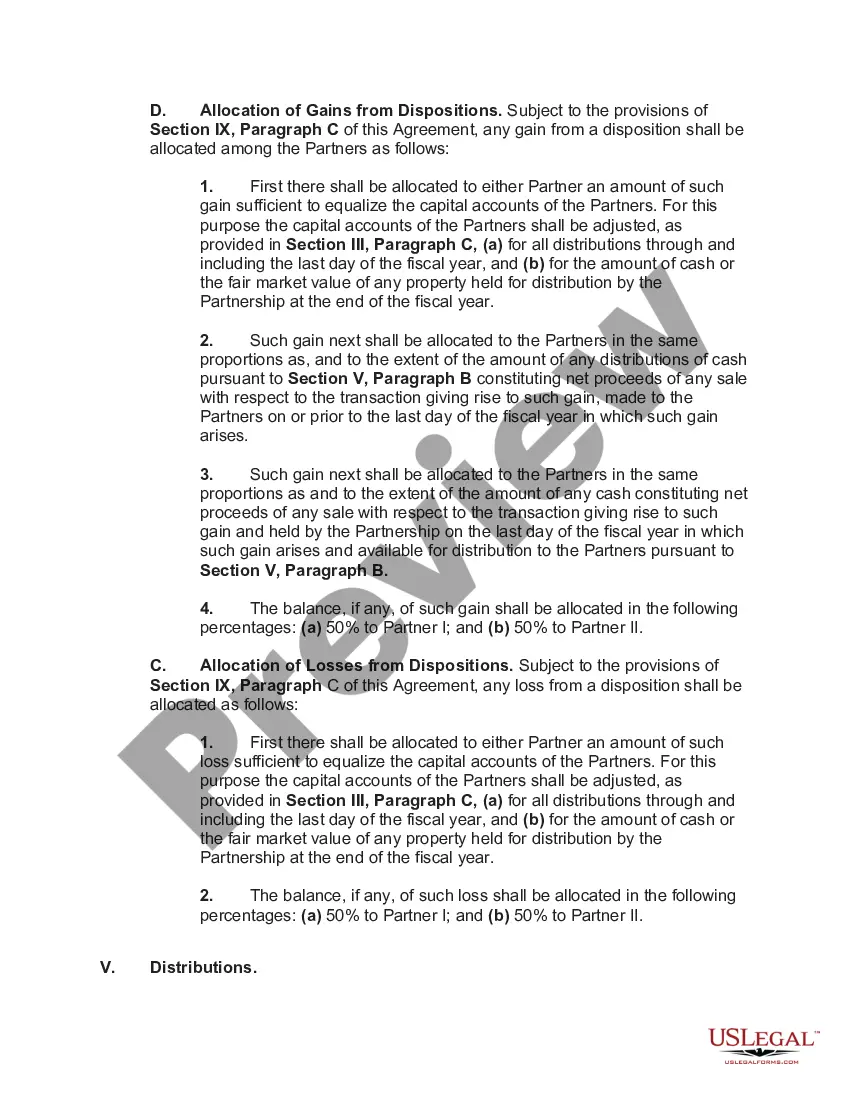

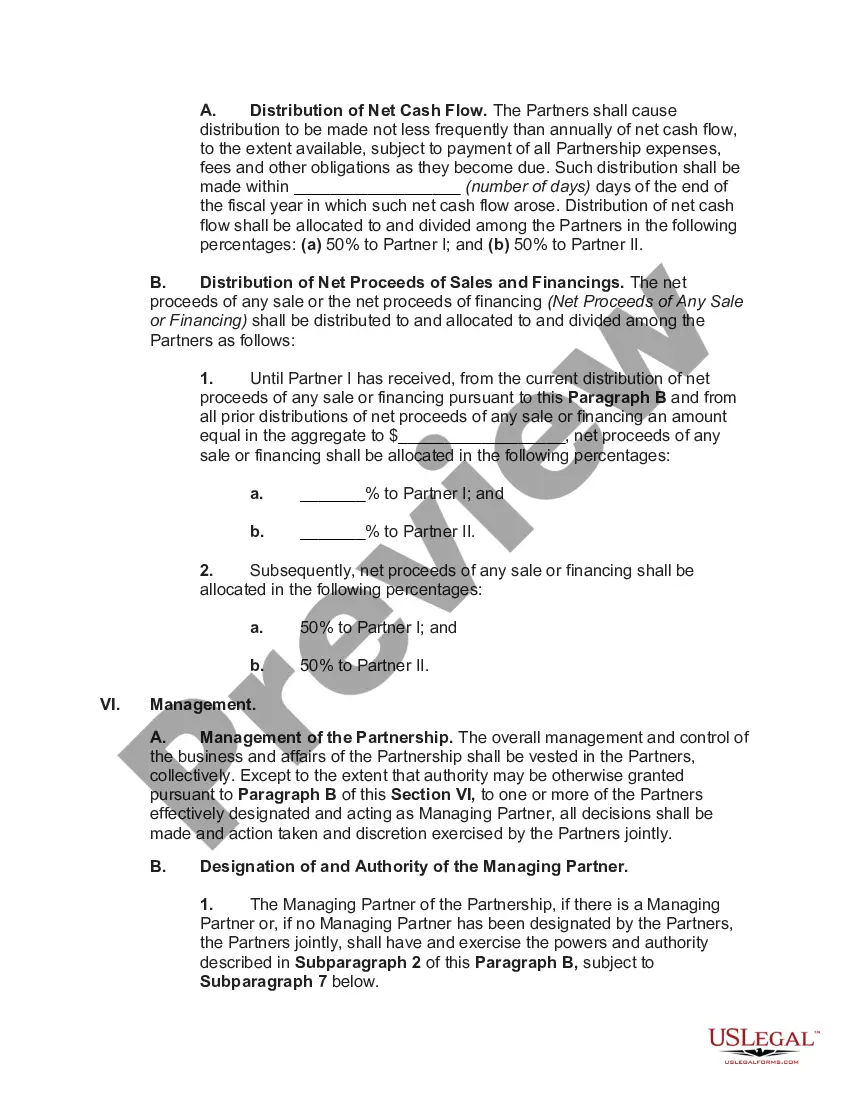

The North Carolina Partnership Agreement for a Real Estate Development is a legally binding contract that outlines the terms and conditions between multiple parties involved in the development of a real estate project in the state of North Carolina. This agreement serves as a framework to govern the collaboration, responsibilities, and sharing of profits and losses among the partners. The partnership agreement typically includes several key provisions, such as the names and roles of all partners involved, the purpose and objectives of the partnership, the financial contributions and liabilities of each partner, the profit distribution method, and the decision-making processes. There are different types of partnership agreements that can be tailored to suit the specific needs and requirements of the real estate development. Some common types include: 1. General Partnership Agreement: This type of agreement is established when two or more partners join together to form a partnership, assuming equal levels of responsibilities and liabilities. Each partner has the authority to participate in the management and decision-making processes of the project. 2. Limited Partnership Agreement: In this agreement, there are two types of partners: general partners and limited partners. General partners have unlimited liability and are directly involved in the day-to-day operations and management of the real estate development. Limited partners, on the other hand, have limited liability and contribute financially to the project but do not participate in management decisions. 3. Limited Liability Partnership Agreement: This partnership agreement provides liability protection to all partners involved, meaning that they are not personally responsible for the debts or obligations of the partnership. It allows partners to have limited liability while still being actively involved in managing the real estate development. 4. Joint Venture Agreement: This type of partnership agreement is typically used when two or more parties collaborate for a specific real estate development project. Each party contributes assets, expertise, or both, and shares in the profits or losses in accordance with their respective contributions. It is essential for all parties involved in a real estate development project in North Carolina to carefully draft and review the partnership agreement. Seeking legal counsel is highly recommended ensuring compliance with state laws and regulations and to protect the rights and interests of all partners involved.

North Carolina Partnership Agreement for a Real Estate Development

Description

How to fill out North Carolina Partnership Agreement For A Real Estate Development?

It is possible to invest several hours on-line searching for the legal file format which fits the federal and state demands you will need. US Legal Forms supplies a huge number of legal kinds that happen to be evaluated by professionals. It is possible to down load or print the North Carolina Partnership Agreement for a Real Estate Development from your assistance.

If you currently have a US Legal Forms account, you may log in and click on the Down load switch. Afterward, you may complete, change, print, or indication the North Carolina Partnership Agreement for a Real Estate Development. Each and every legal file format you purchase is the one you have for a long time. To obtain another version associated with a purchased type, go to the My Forms tab and click on the related switch.

Should you use the US Legal Forms website initially, keep to the easy recommendations under:

- First, make sure that you have selected the correct file format for the county/metropolis that you pick. Read the type description to make sure you have picked the proper type. If available, use the Review switch to look with the file format as well.

- If you wish to get another variation of your type, use the Lookup area to get the format that meets your requirements and demands.

- Upon having located the format you want, click Get now to move forward.

- Select the pricing program you want, type your credentials, and sign up for an account on US Legal Forms.

- Full the purchase. You can utilize your charge card or PayPal account to fund the legal type.

- Select the formatting of your file and down load it for your product.

- Make adjustments for your file if necessary. It is possible to complete, change and indication and print North Carolina Partnership Agreement for a Real Estate Development.

Down load and print a huge number of file themes using the US Legal Forms website, which offers the most important collection of legal kinds. Use specialist and express-specific themes to tackle your small business or person needs.