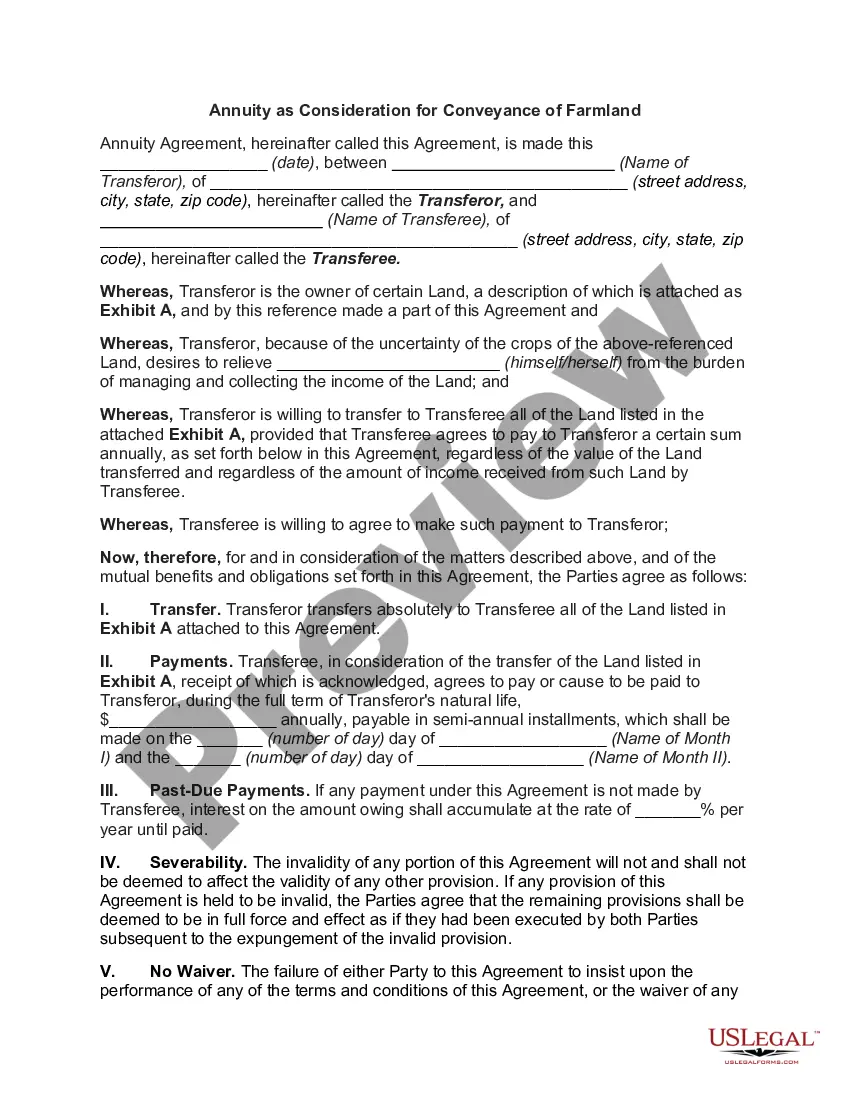

North Carolina Annuity as Consideration for Transfer of Securities

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Annuity As Consideration For Transfer Of Securities?

You can spend hours online searching for the legal documents template that meets the state and federal standards you require.

US Legal Forms provides thousands of legal documents that have been reviewed by professionals.

You can download or create the North Carolina Annuity as Consideration for Transfer of Securities from their service.

If available, utilize the Preview option to browse through the document template as well.

- If you already possess a US Legal Forms account, you can Log In and click the Download button.

- After that, you may complete, alter, create, or sign the North Carolina Annuity as Consideration for Transfer of Securities.

- Each legal document template you buy is yours indefinitely.

- To obtain another copy of the purchased form, navigate to the My documents section and click the respective option.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have chosen the correct document template for the area/city of your preference.

- Review the form description to confirm you have selected the correct template.

Form popularity

FAQ

A fixed annuity is an insurance product, not a security, because the insurance company must credit the annuity holder's account with the specified interest rate for the contractually-stipulated time period, regardless of market fluctuations in actual interest rates.

The main difference between this and owning stocks outright is that the portfolio is inside an annuity. Everything else is pretty much the same same asset class, same type of returns, same investment risk. But the annuity provides additional features that are not available through common stock ownership.

The new rule permits variable annuity and variable life insurance contracts to use a summary prospectus to provide disclosures to investors. A summary prospectus is a concise, reader-friendly summary of key facts about the contract.

The prospectus contains important information about the annuity contract, including fees and charges, invest- ment options, death benefits, and annuity payout options.

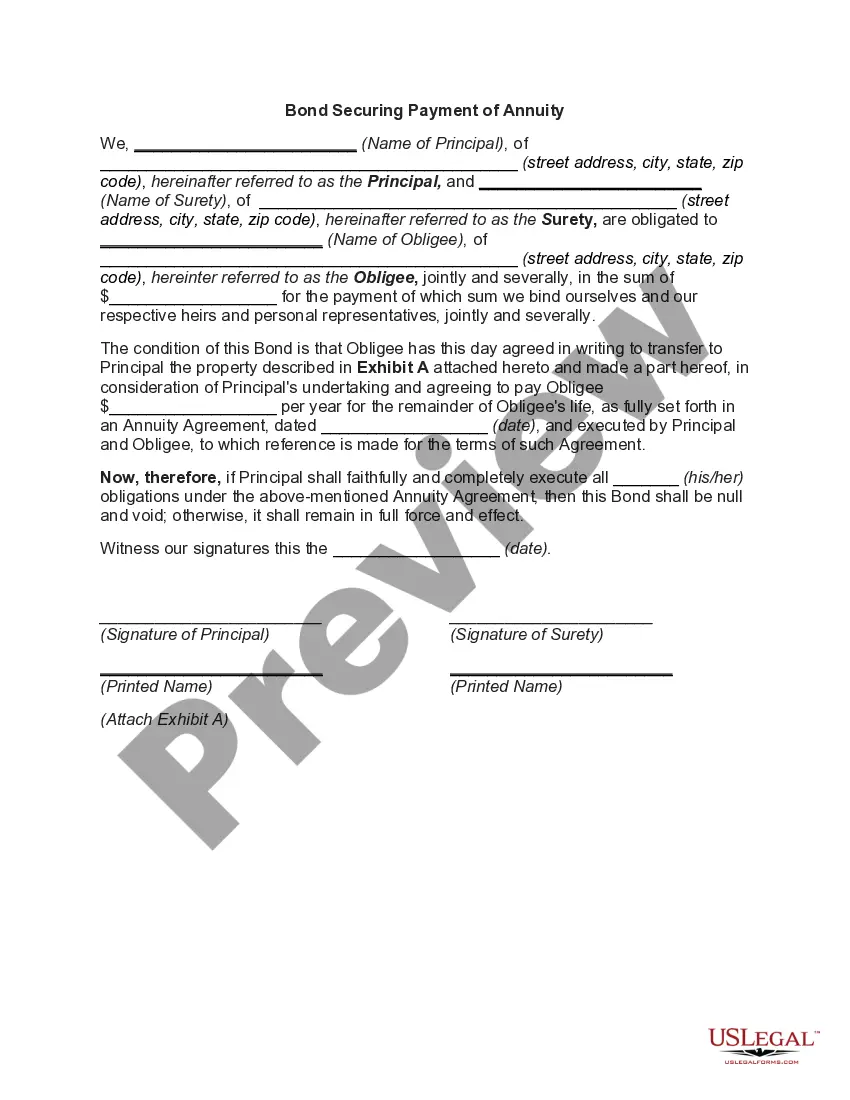

An annuity consideration or premium is the money an individual pays to an insurance company to fund an annuity or receive a stream of annuity payments. An annuity consideration may be made as a lump sum or as a series of payments, often referred to as contributions.

If you want to sell variable annuities or mutual funds, you will need a Series 6 and 63. If you simply want to offer fixed annuities and life insurance products for guaranteed income or asset protection needs, you will only need a life insurance license in the states you intend to do business.

To give the annuity away, you simply contact the insurance company and state that you want to gift the ownership of the annuity policy to someone else or a trust. There are some tax implications to consider with this, though. Before you give an annuity away, you need to look at its status.

An annuity is not a security; however, the money in an annuity account will most definitely be invested in some of the underlying financial securities mentioned above.

Variable annuities Unlike fixed and indexed annuities, a variable annuity is considered a security under federal law and is subject to regulation by the Securities and Exchange Commission (SEC) and FINRA. 3feff Potential investors must also receive a prospectus.

The new rule permits variable annuity and variable life insurance contracts to use a summary prospectus to provide disclosures to investors. A summary prospectus is a concise, reader-friendly summary of key facts about the contract.