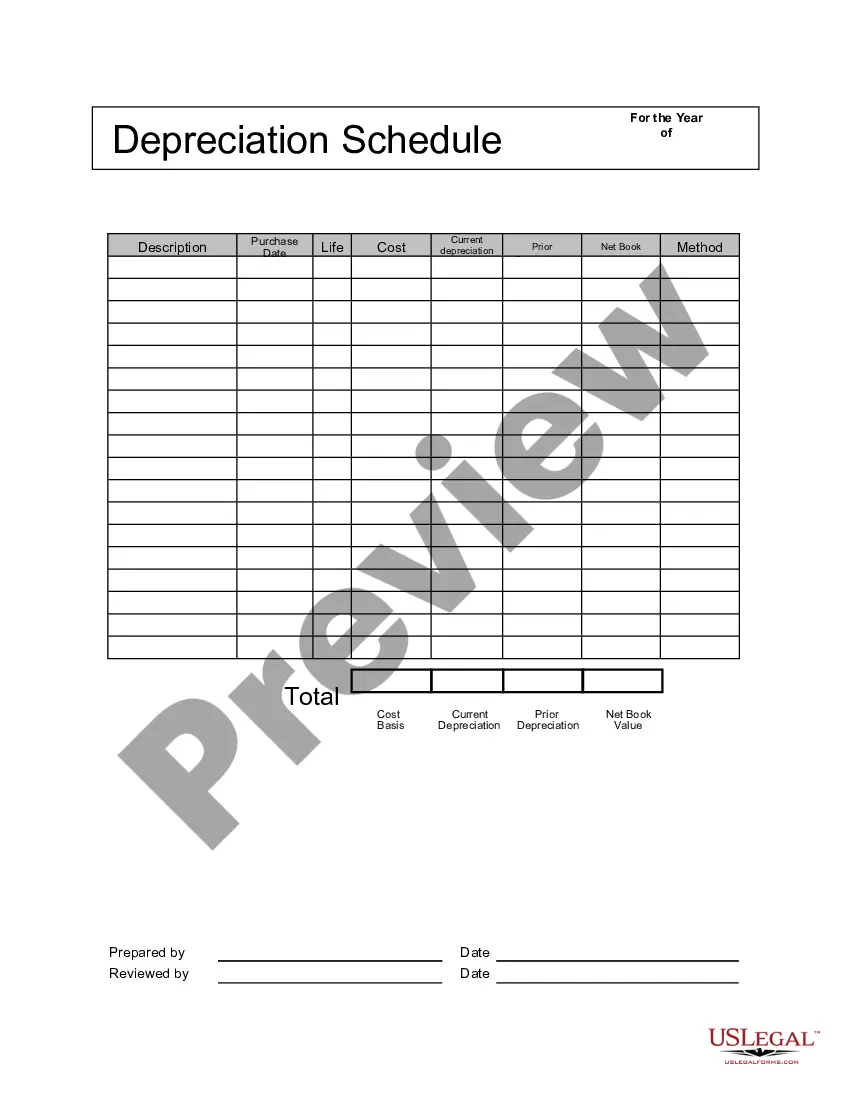

A North Carolina Depreciation Schedule refers to an essential financial document outlining the depreciation of assets in accordance with state laws. It serves as a tool for businesses, individuals, and tax professionals to accurately determine the value of depreciable assets over time for tax and accounting purposes. The North Carolina Depreciation Schedule follows the guidelines set by the North Carolina Department of Revenue (ACTOR) and is often used in conjunction with federal depreciation rules. It ensures compliance with state tax regulations while providing an accurate representation of the asset's decreasing value over its useful life. Various types of depreciation schedules are used within the North Carolina Depreciation Schedule framework. These types may include the following: 1. Straight-Line Depreciation: This is the most commonly used method, where the asset's value is depreciated evenly over its useful life. It spreads the depreciation expense evenly across each year. 2. Accelerated Depreciation: This method allows for a larger depreciation deduction in the early years of an asset's life, reflecting the concept that assets typically lose value more rapidly in the beginning. Examples of accelerated depreciation methods include the Modified Accelerated Cost Recovery System (MARS) and the 150% declining balance method. 3. Section 179 Expense Deduction: North Carolina also adheres to the federal Section 179 provision, which allows businesses to deduct upfront the cost of certain qualifying assets, rather than depreciating them over time. When preparing a North Carolina Depreciation Schedule, taxpayers must consider factors such as the asset's acquisition cost, salvage value, useful life, and applicable depreciation method. The depreciation schedule is pivotal for accurately calculating annual depreciation expenses, tracking asset values, and complying with state tax reporting requirements. In conclusion, the North Carolina Depreciation Schedule is a comprehensive financial tool used to determine the depreciation of assets in accordance with state regulations. By carefully considering the different types of depreciation methods available, businesses and individuals can accurately calculate asset values, reduce taxable income, and ensure adherence to North Carolina tax laws.

North Carolina Depreciation Schedule

Description

How to fill out North Carolina Depreciation Schedule?

If you have to total, down load, or produce legal document themes, use US Legal Forms, the greatest selection of legal forms, that can be found on the web. Use the site`s simple and easy hassle-free research to find the papers you want. Various themes for enterprise and specific purposes are categorized by classes and claims, or keywords. Use US Legal Forms to find the North Carolina Depreciation Schedule within a few click throughs.

When you are previously a US Legal Forms client, log in in your profile and click the Download key to have the North Carolina Depreciation Schedule. You can also entry forms you in the past downloaded in the My Forms tab of your own profile.

If you use US Legal Forms the first time, follow the instructions below:

- Step 1. Ensure you have chosen the form for that appropriate city/region.

- Step 2. Use the Review solution to examine the form`s information. Never neglect to learn the outline.

- Step 3. When you are not happy with all the develop, utilize the Lookup industry towards the top of the display screen to discover other models of your legal develop design.

- Step 4. After you have located the form you want, click on the Acquire now key. Choose the prices plan you like and add your accreditations to sign up on an profile.

- Step 5. Procedure the transaction. You should use your credit card or PayPal profile to perform the transaction.

- Step 6. Select the formatting of your legal develop and down load it on the gadget.

- Step 7. Total, revise and produce or sign the North Carolina Depreciation Schedule.

Each and every legal document design you get is the one you have for a long time. You have acces to each develop you downloaded inside your acccount. Click on the My Forms area and select a develop to produce or down load again.

Remain competitive and down load, and produce the North Carolina Depreciation Schedule with US Legal Forms. There are millions of professional and state-particular forms you may use for your enterprise or specific needs.