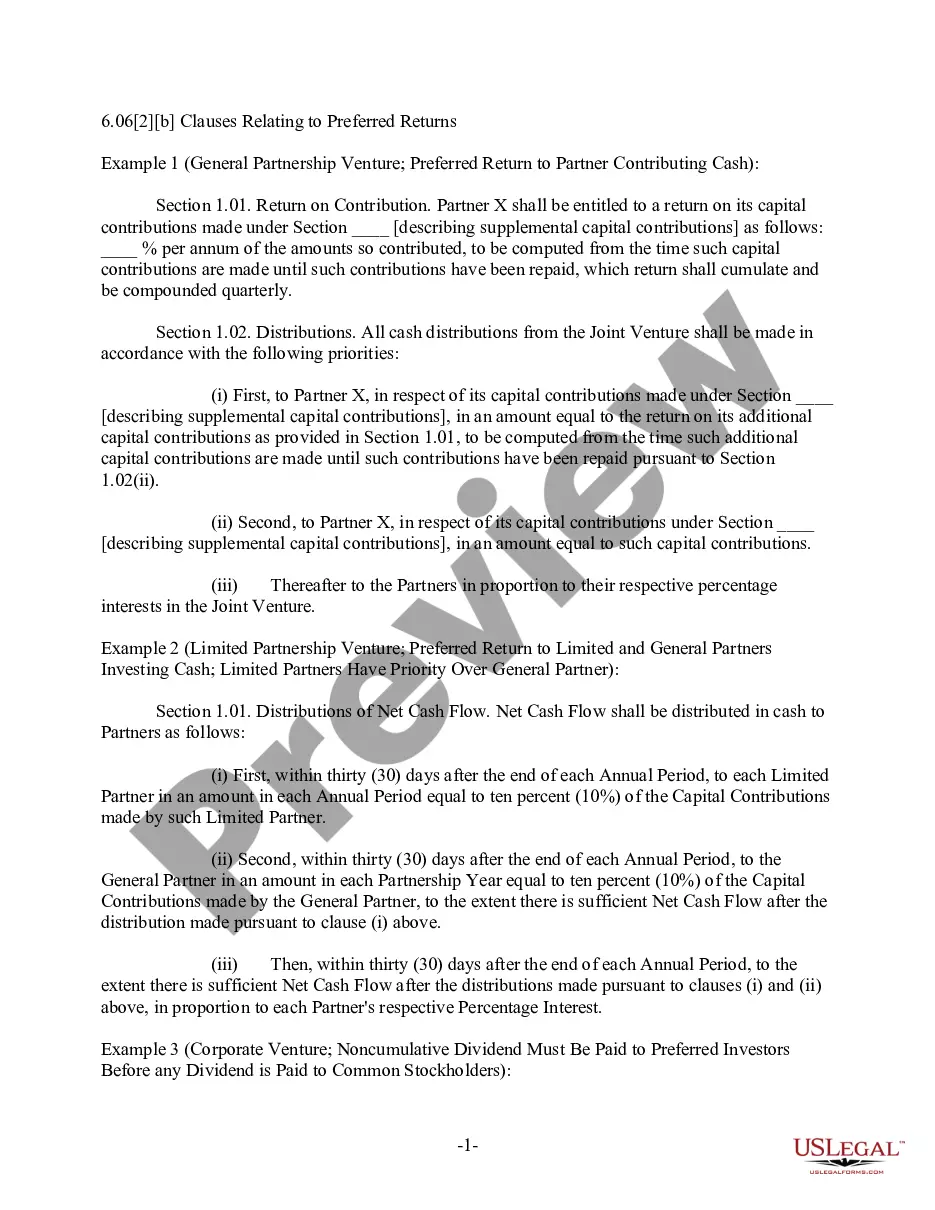

North Carolina Sample Proposed Amendment to Partnership Agreement to provide for issuance of preferred partnership interests

Description

How to fill out Sample Proposed Amendment To Partnership Agreement To Provide For Issuance Of Preferred Partnership Interests?

US Legal Forms - among the most significant libraries of authorized forms in America - delivers a wide range of authorized record web templates it is possible to acquire or printing. Utilizing the web site, you can get a large number of forms for business and personal functions, categorized by groups, claims, or keywords and phrases.You can get the most up-to-date models of forms such as the North Carolina Sample Proposed Amendment to Partnership Agreement to provide for issuance of preferred partnership interests within minutes.

If you have a membership, log in and acquire North Carolina Sample Proposed Amendment to Partnership Agreement to provide for issuance of preferred partnership interests in the US Legal Forms library. The Acquire key will appear on each and every develop you view. You gain access to all earlier delivered electronically forms within the My Forms tab of your respective profile.

If you want to use US Legal Forms for the first time, allow me to share simple recommendations to get you began:

- Ensure you have picked the correct develop for your area/region. Go through the Preview key to review the form`s information. Browse the develop description to actually have selected the proper develop.

- In the event the develop doesn`t suit your specifications, utilize the Search discipline towards the top of the display to find the one that does.

- When you are happy with the form, affirm your option by simply clicking the Acquire now key. Then, choose the rates prepare you favor and offer your accreditations to sign up on an profile.

- Procedure the purchase. Use your bank card or PayPal profile to complete the purchase.

- Choose the format and acquire the form on the system.

- Make adjustments. Complete, modify and printing and signal the delivered electronically North Carolina Sample Proposed Amendment to Partnership Agreement to provide for issuance of preferred partnership interests.

Each and every format you put into your bank account lacks an expiration day which is your own property forever. So, if you would like acquire or printing yet another backup, just visit the My Forms section and click on about the develop you will need.

Get access to the North Carolina Sample Proposed Amendment to Partnership Agreement to provide for issuance of preferred partnership interests with US Legal Forms, the most comprehensive library of authorized record web templates. Use a large number of professional and status-particular web templates that fulfill your small business or personal requirements and specifications.

Form popularity

FAQ

Normally an agreement can only be changed by unanimous agreement among the shareholders or partners. A deed of variation, or an entirely new agreement, will need to be drawn up and signed by all the shareholders or partners.

If one of the partners retires, dies, or enters bankruptcy, the partnership may be dissolved automatically under the terms of its governing agreement. Alternatively, the objectives of the partnership may have been met and the parties' official relationship may no longer be necessary.

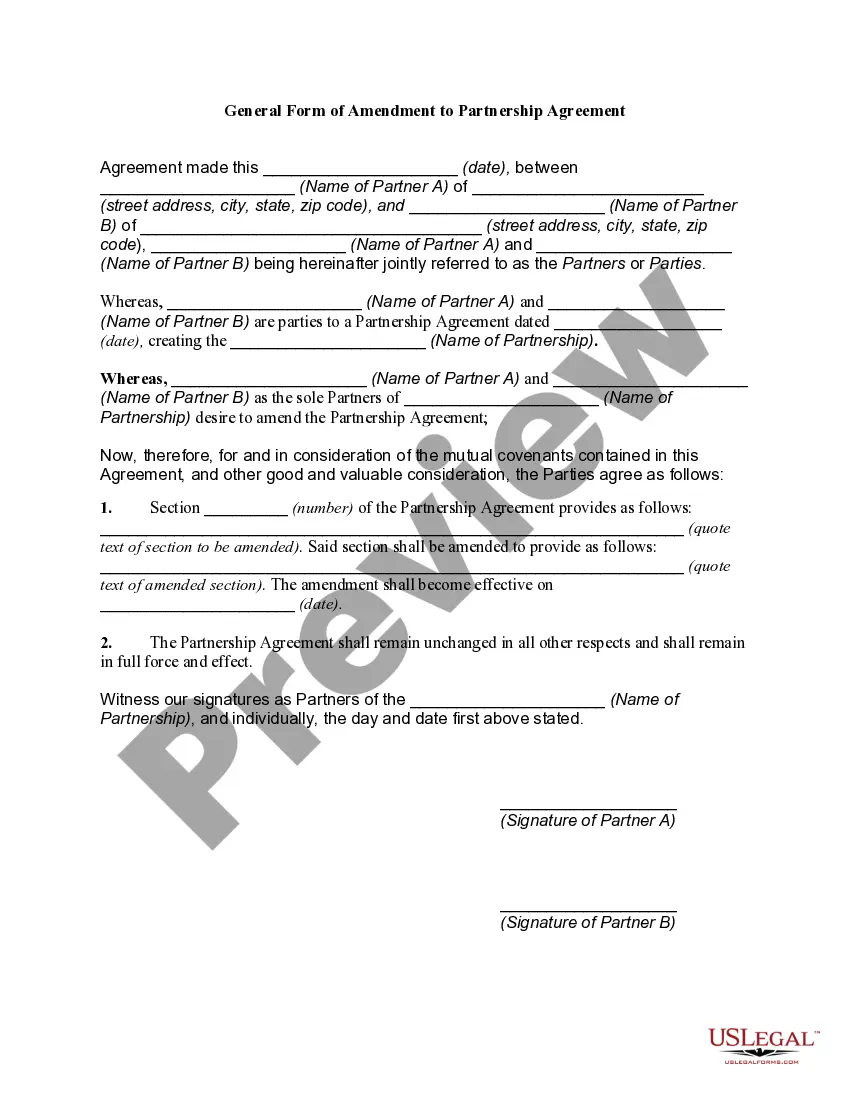

A Partnership Amendment, also called a Partnership Addendum, is used to modify, add, or remove terms in a Partnership Agreement. A Partnership Amendment is usually attached to an existing Partnership Agreement to reflect any changes.

The Court noted that a partnership is, by statutory definition, ?an association of two or more persons to carry on as co-owners a business for profit?.? Thus, the Court concluded that withdrawal of one partner automatically resulted in dissolution of the partnership, because it left only one ?partner.? This meant that ...

Any change in the existing agreement is known as reconstitution of the partnership firm. Thus, the existing agreement ends and a new agreement is formed with the changed relationship among the members of the partnership firm and its composition.

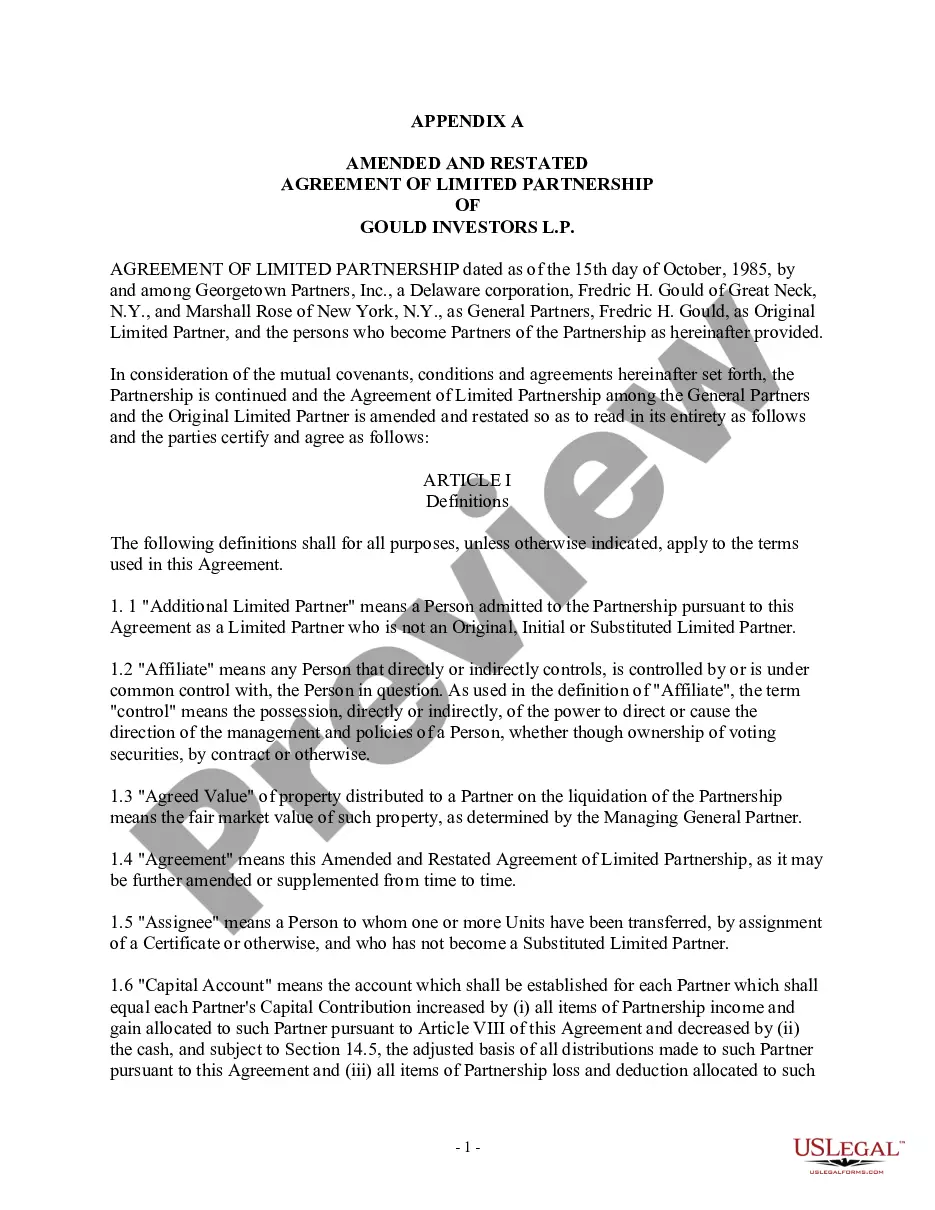

LP COMMON UNITS means common units representing limited partnership interests in the common equity of the Operating Partnership. LP COMMON UNITS means Units held by a Limited Partner, other than Preferred Units.

Types of Withdrawal from a Partnership Firm The partner is guilty of a breach of trust or is in breach of the partnership agreement. The partner has been declared as a person of unsound mind by a competent court. The partner is permanently incapacitated.

Any slight changes made in the relationship between partners in a partnership firm would result in the reconstitution of the firm itself. Thus, whenever a new partner is introduced or when an existing partner is being removed, a partnership firm is bound to be reconstituted.