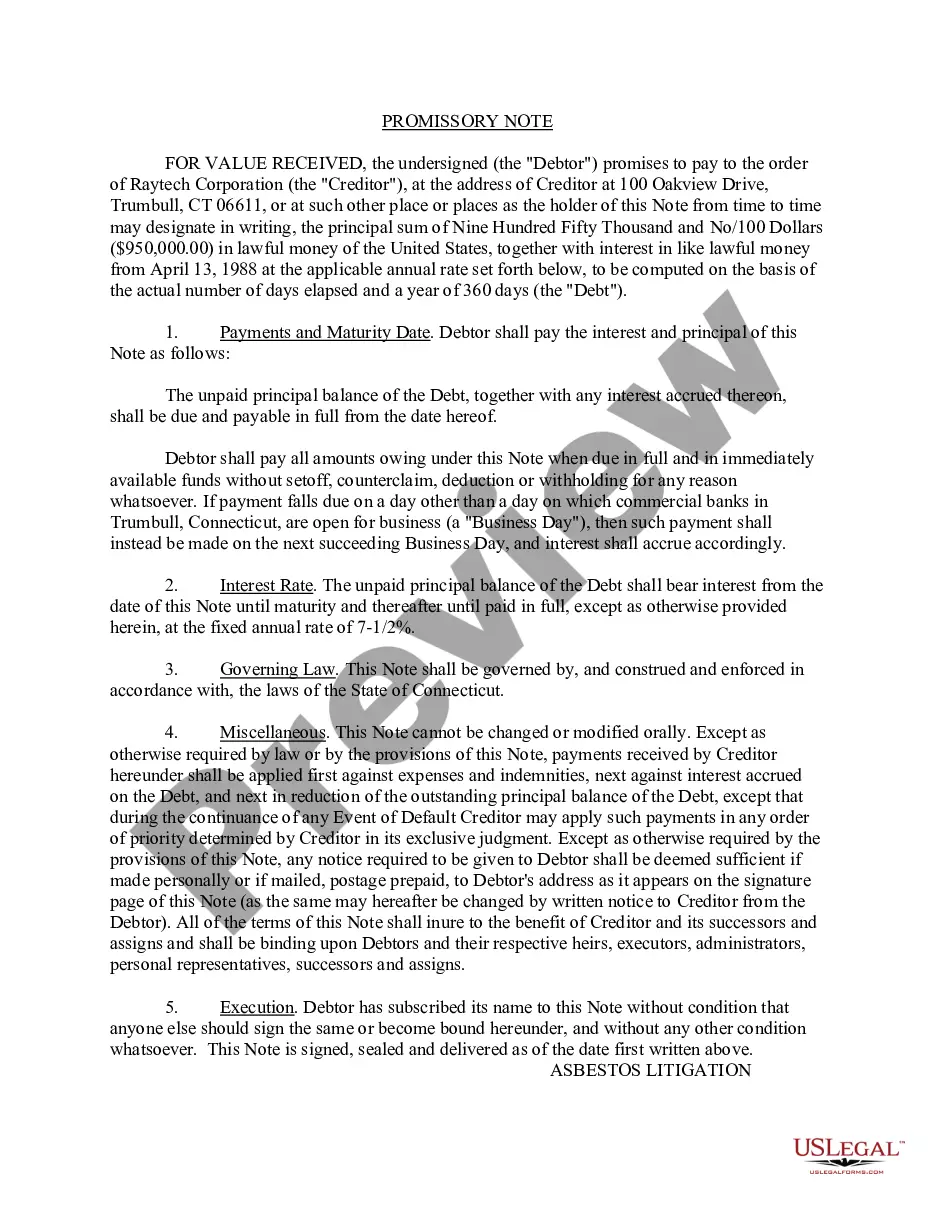

North Carolina Form of Note

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Form Of Note?

If you have to total, download, or printing legitimate file themes, use US Legal Forms, the biggest selection of legitimate types, which can be found on the Internet. Make use of the site`s simple and practical research to obtain the files you need. Numerous themes for business and specific uses are sorted by categories and claims, or key phrases. Use US Legal Forms to obtain the North Carolina Form of Note with a number of clicks.

If you are already a US Legal Forms buyer, log in for your accounts and then click the Obtain button to find the North Carolina Form of Note. Also you can gain access to types you in the past downloaded in the My Forms tab of your respective accounts.

If you work with US Legal Forms initially, follow the instructions below:

- Step 1. Make sure you have chosen the form for the right city/region.

- Step 2. Use the Review method to check out the form`s articles. Do not neglect to read the explanation.

- Step 3. If you are not satisfied with the kind, utilize the Research area on top of the display screen to locate other versions from the legitimate kind format.

- Step 4. Once you have discovered the form you need, select the Acquire now button. Pick the prices program you choose and add your accreditations to register to have an accounts.

- Step 5. Method the financial transaction. You may use your charge card or PayPal accounts to perform the financial transaction.

- Step 6. Select the structure from the legitimate kind and download it on your own system.

- Step 7. Comprehensive, revise and printing or sign the North Carolina Form of Note.

Each and every legitimate file format you acquire is your own forever. You might have acces to every kind you downloaded in your acccount. Click the My Forms area and decide on a kind to printing or download again.

Contend and download, and printing the North Carolina Form of Note with US Legal Forms. There are many expert and status-particular types you can use for your personal business or specific requirements.

Form popularity

FAQ

To be legally enforceable, a promissory note must meet multiple legal conditions. Moreover, it must contain both an offer of agreement and an acceptance of agreement. All contracts state the type of services or goods rendered and indicate how much they cost.

A promissory note could become invalid if: It isn't signed by both parties. The note violates laws. One party tries to change the terms of the agreement without notifying the other party.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

You don't need a witness to sign a North Carolina promissory note. Obtaining a witness or signature from a notary public, for example, would strengthen the note's validity if you were to use this document in court.

3 Year Statute of Limitations on Most Debts in North Carolina. In North Carolina, Section 1-52.1 of the North Carolina Rules of Civil Procedure explains the statute of limitations for debts is 3 years for auto and installment loans, promissory notes, and credit cards.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

Signatures. Generally, promissory notes do not need to be notarized. Typically, legally enforceable promissory notes must be signed by individuals and contain unconditional promises to pay specific amounts of money.

Promissory notes don't have to be notarized in most cases. You can typically sign a legally binding promissory note that contains unconditional pledges to pay a certain sum of money. However, you can strengthen the legality of a valid promissory note by having it notarized.