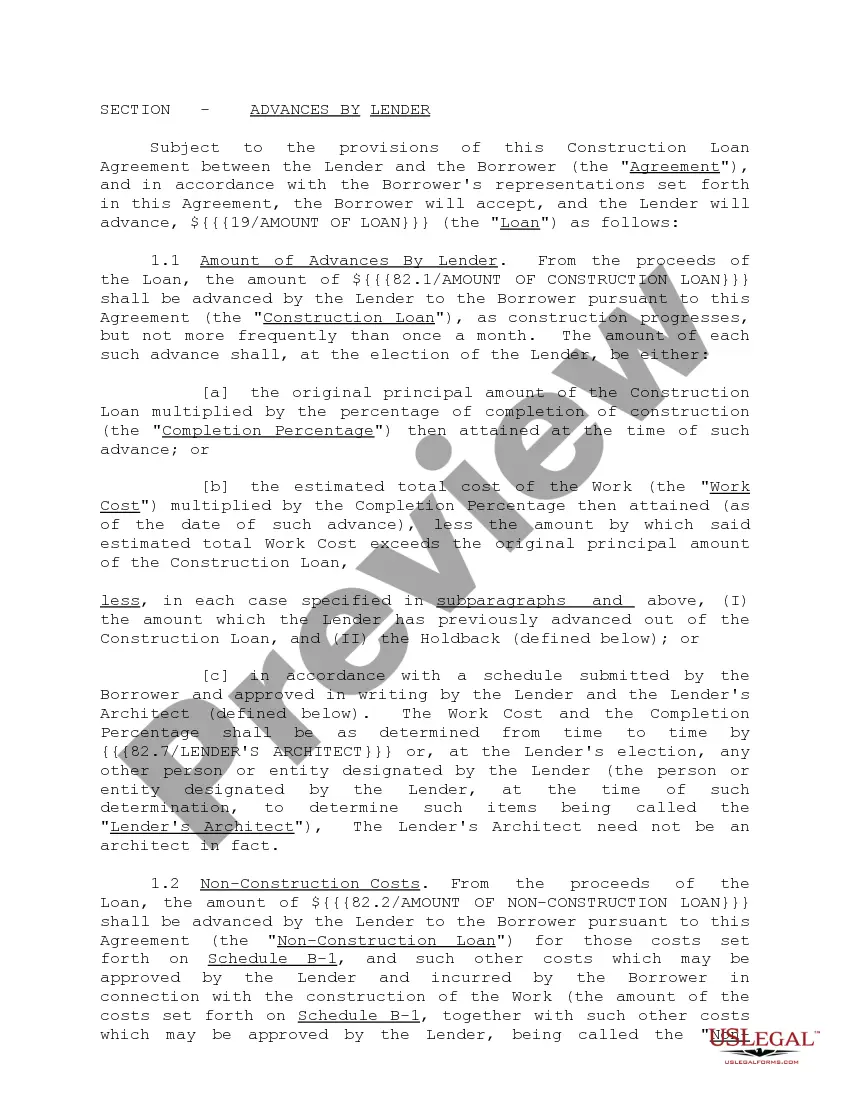

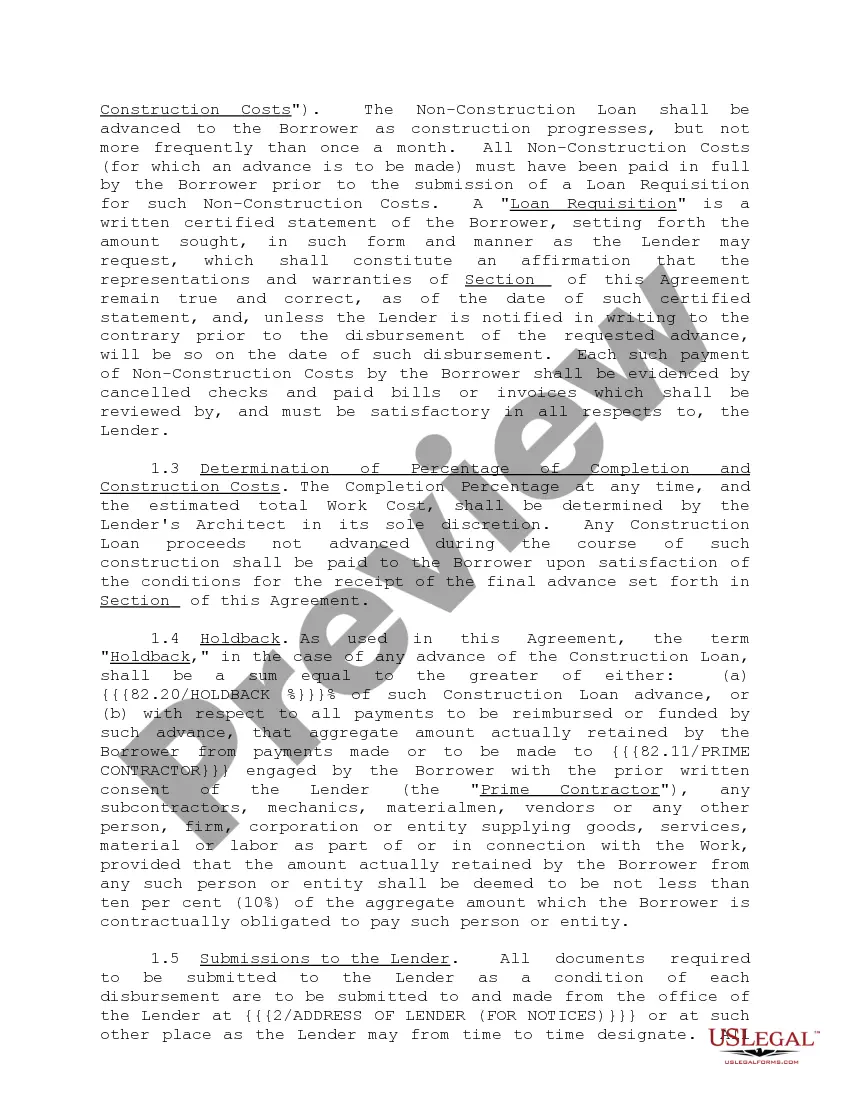

"Construction Loan Agreements and Variations" is a American Lawyer Media form. This form is to be used as a construction loan agreement.

North Carolina Construction Loan Agreements and Variations: A Comprehensive Guide Introduction: North Carolina offers various types of construction loan agreements and variations to facilitate the financing of real estate development and construction projects within the state. These agreements serve as legal documentation between lenders and borrowers, outlining the terms, conditions, and repayment structure of the loan. This article aims to provide a detailed description of North Carolina construction loan agreements, highlighting their various types and variations. 1. Traditional Construction Loan Agreement: The traditional construction loan agreement in North Carolina offers a standard framework for financing construction projects. It encompasses terms related to loan disbursement, interest rates, repayment schedules, and required collateral. This agreement typically includes provisions regarding the verification of budget and construction plans, as well as requirements for inspections, permits, and other necessary documentation. 2. Construction-to-Permanent Loan Agreement: In North Carolina, borrowers may choose a construction-to-permanent loan agreement, which combines the financing for both construction and permanent mortgage into a single loan. This agreement streamlines the loan process and eliminates the need for separate agreements to cover the construction phase and long-term financing. It provides flexibility by allowing borrowers to lock in the mortgage rate during the construction period, thereby avoiding potential interest rate fluctuations. 3. Owner-Builder Construction Loan Agreement: For individuals intending to act as both the owner and builder of a construction project, the owner-builder construction loan agreement may be an appropriate choice. This agreement caters to borrowers who have experience in construction and wish to oversee the building process themselves. It includes provisions related to the borrower's responsibilities, insurance requirements, lien waivers, and warranties. Additionally, the owner-builder may be required to provide evidence of qualification and demonstrate their ability to manage the construction project effectively. 4. Renovation Construction Loan Agreement: In cases where existing properties require substantial renovations or improvements, borrowers can opt for a renovation construction loan agreement. This type of loan provides financing for the renovation costs, including materials, labor, and other associated expenses. The agreement covers terms specific to renovation, such as project timelines, permitted work, and the release of funds upon meeting pre-established milestones. 5. Single-Close vs. Two-Close Construction Loan Agreements: North Carolina borrowers can choose between single-close and two-close construction loan agreements based on their preferences and project requirements. A single-close construction loan agreement combines the construction and permanent mortgage into one loan, minimizing the paperwork and potential costs associated with separate agreements. Conversely, a two-close construction loan agreement involves separate loans for construction and permanent mortgage, which may be preferred in certain situations. Conclusion: North Carolina offers a range of construction loan agreements and variations to suit the unique needs of borrowers involved in real estate development and construction projects. These agreements, such as the traditional loan agreement, construction-to-permanent agreement, owner-builder agreement, renovation agreement, and single-close/two-close agreements, enable borrowers to secure financing while adhering to specific terms and conditions. It is crucial for borrowers to understand the intricacies of each agreement and consult with legal and financial professionals to ensure compliance with North Carolina laws and regulations.North Carolina Construction Loan Agreements and Variations: A Comprehensive Guide Introduction: North Carolina offers various types of construction loan agreements and variations to facilitate the financing of real estate development and construction projects within the state. These agreements serve as legal documentation between lenders and borrowers, outlining the terms, conditions, and repayment structure of the loan. This article aims to provide a detailed description of North Carolina construction loan agreements, highlighting their various types and variations. 1. Traditional Construction Loan Agreement: The traditional construction loan agreement in North Carolina offers a standard framework for financing construction projects. It encompasses terms related to loan disbursement, interest rates, repayment schedules, and required collateral. This agreement typically includes provisions regarding the verification of budget and construction plans, as well as requirements for inspections, permits, and other necessary documentation. 2. Construction-to-Permanent Loan Agreement: In North Carolina, borrowers may choose a construction-to-permanent loan agreement, which combines the financing for both construction and permanent mortgage into a single loan. This agreement streamlines the loan process and eliminates the need for separate agreements to cover the construction phase and long-term financing. It provides flexibility by allowing borrowers to lock in the mortgage rate during the construction period, thereby avoiding potential interest rate fluctuations. 3. Owner-Builder Construction Loan Agreement: For individuals intending to act as both the owner and builder of a construction project, the owner-builder construction loan agreement may be an appropriate choice. This agreement caters to borrowers who have experience in construction and wish to oversee the building process themselves. It includes provisions related to the borrower's responsibilities, insurance requirements, lien waivers, and warranties. Additionally, the owner-builder may be required to provide evidence of qualification and demonstrate their ability to manage the construction project effectively. 4. Renovation Construction Loan Agreement: In cases where existing properties require substantial renovations or improvements, borrowers can opt for a renovation construction loan agreement. This type of loan provides financing for the renovation costs, including materials, labor, and other associated expenses. The agreement covers terms specific to renovation, such as project timelines, permitted work, and the release of funds upon meeting pre-established milestones. 5. Single-Close vs. Two-Close Construction Loan Agreements: North Carolina borrowers can choose between single-close and two-close construction loan agreements based on their preferences and project requirements. A single-close construction loan agreement combines the construction and permanent mortgage into one loan, minimizing the paperwork and potential costs associated with separate agreements. Conversely, a two-close construction loan agreement involves separate loans for construction and permanent mortgage, which may be preferred in certain situations. Conclusion: North Carolina offers a range of construction loan agreements and variations to suit the unique needs of borrowers involved in real estate development and construction projects. These agreements, such as the traditional loan agreement, construction-to-permanent agreement, owner-builder agreement, renovation agreement, and single-close/two-close agreements, enable borrowers to secure financing while adhering to specific terms and conditions. It is crucial for borrowers to understand the intricacies of each agreement and consult with legal and financial professionals to ensure compliance with North Carolina laws and regulations.