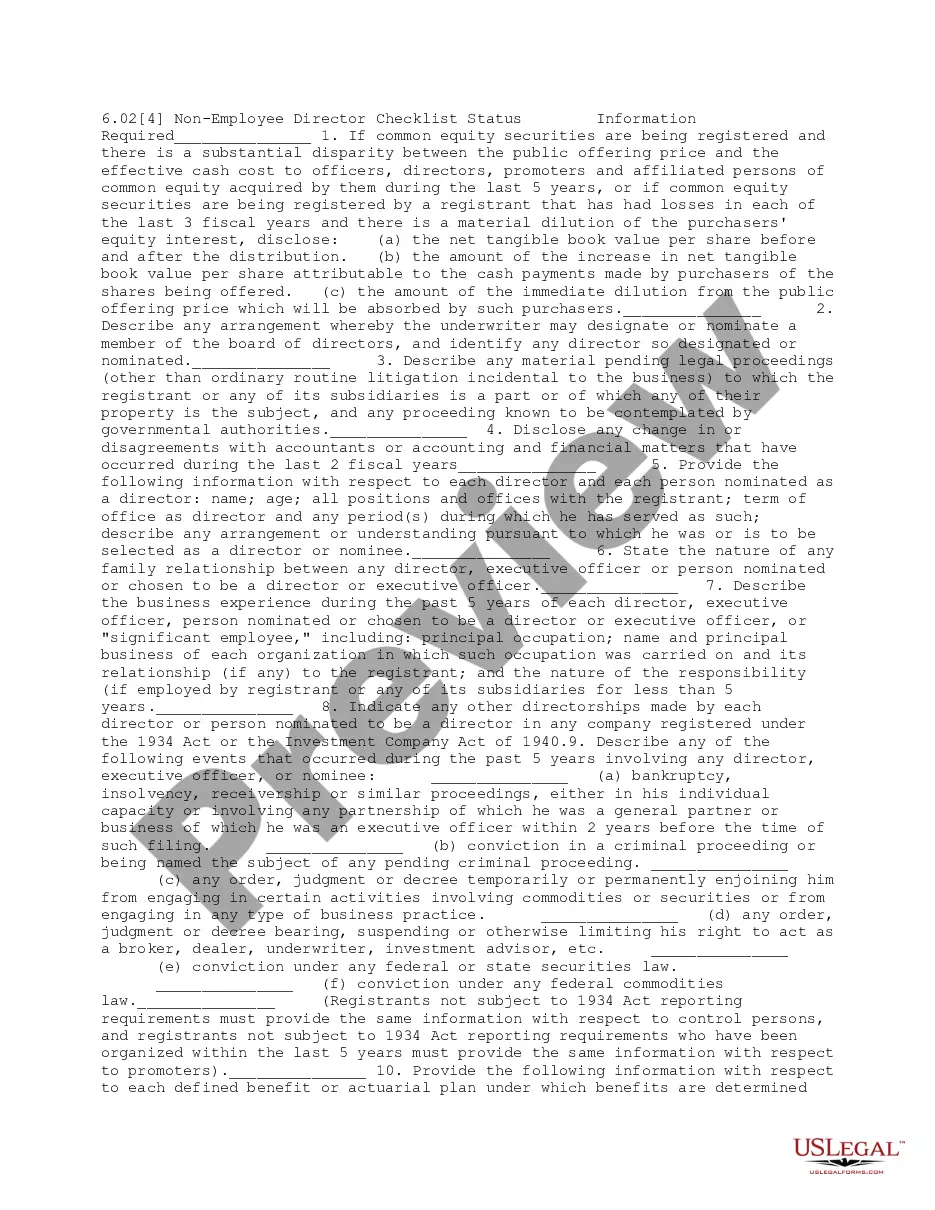

This form is a due diligence checklist that outlines information pertinent to non-employee directors in a business transaction.

North Carolina Nonemployee Director Checklist

Category:

State:

Multi-State

Control #:

US-DD06024

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out North Carolina Nonemployee Director Checklist?

Are you currently in a placement in which you need paperwork for possibly company or personal uses nearly every time? There are a variety of legal record templates accessible on the Internet, but getting versions you can depend on is not straightforward. US Legal Forms delivers a large number of form templates, just like the North Carolina Nonemployee Director Checklist, which can be written to satisfy federal and state requirements.

When you are previously informed about US Legal Forms website and have a free account, simply log in. Afterward, you may acquire the North Carolina Nonemployee Director Checklist template.

If you do not have an profile and wish to start using US Legal Forms, follow these steps:

- Discover the form you need and make sure it is for the right metropolis/county.

- Make use of the Review option to check the shape.

- Look at the description to ensure that you have chosen the right form.

- If the form is not what you`re searching for, utilize the Lookup field to obtain the form that meets your needs and requirements.

- Whenever you obtain the right form, just click Buy now.

- Pick the pricing prepare you desire, submit the necessary details to generate your money, and buy the order making use of your PayPal or bank card.

- Select a practical data file format and acquire your backup.

Discover all of the record templates you might have bought in the My Forms menu. You can obtain a additional backup of North Carolina Nonemployee Director Checklist anytime, if possible. Just click on the needed form to acquire or print out the record template.

Use US Legal Forms, by far the most substantial selection of legal kinds, in order to save time as well as steer clear of blunders. The service delivers professionally created legal record templates which you can use for a selection of uses. Create a free account on US Legal Forms and start generating your way of life easier.

Form popularity

FAQ

Nonemployee compensation (also known as self-employment income) is the income you receive from a payer who classifies you as an independent contractor rather than as an employee. This type of income is reported on Form 1099-MISC, and you're required to pay self-employment taxes on it.

Form 1099-NEC is used to report non-employee compensation of $600 ore more for the year, to the IRS and the recipient. Non-employees include freelancers, independent contractors, small businesses, and professionals who provide services. The compensation being reported must be for services for a trade or business.

There is a new Form 1099-NEC, Nonemployee Compensation for business taxpayers who pay or receive nonemployee compensation. Starting in tax year 2020, payers must complete this form to report any payment of $600 or more to a payee.

Form 1099-NEC. Use Form 1099-NEC solely to report nonemployee compensation payments of $600 or more you make in the course of your business to individuals who aren't employees.Form 1099-MISC.Payer's name, address, and phone number.Payer's TIN.Recipient's TIN.Recipient's name.Street address.City, state, and ZIP.More items...?

Form 1099-MISC is used to report miscellaneous income. Before 2020, the 1099-MISC box 7 was used to report non-employee compensation. The forms 1099-MISC was provided instead of a Form W-2 to independent contractors who provided services but were not considered employees of the payer.

You'll use the amount in Box 1 on your Form(s) 1099-NEC to report your self-employment income. Instead of putting this information directly on Form 1040, you'll report it on Schedule C.

Independent contractors, freelancers, sole proprietors, and self-employed individuals are examples of nonemployees who would receive a 1099-NEC. The recipient uses the information on a 1099-NEC to complete the appropriate sections of their tax return.

Self-employment taxes As a self-employed individual, you must pay Social Security and Medicare taxes. However, since your 1099-NEC income is not subject to employment-tax withholding, you're required to pay these taxes yourself.

There are two methods to enter the Non-employee compensation and have it flow to the 1040, Line 21:Code the 1099-MISC with the Non-employee Compensation as Non-SE income. Or,Move the income from the 1099-MISC, Line 7 - Nonemployee compensation to 1099-MISC, Line 3 - Other income.

Starting in tax year 2020, nonemployee compensation may be reported to your client on Form 1099-NEC. In previous years, this type of income was typically reported on Form 1099-MISC, box 7.

More info

The IRS has a long list of informational returns that it requires businesses to file. Part of that list includes 1099 forms, which detail any income a ... File with the NC Secretary of State Business RegistrationGuidebook for Boards of Directors of North Carolina. Nonprofits explains the duties and ...8 pagesMissing: Nonemployee ? Must include: Nonemployee

File with the NC Secretary of State Business RegistrationGuidebook for Boards of Directors of North Carolina. Nonprofits explains the duties and ...For the 2020 tax year, the Internal Revenue Service (IRS) moved reporting of certain nonemployee compensation, including current and ... The ultimate guide to understanding the what, why, and how of Form 1099-NEC for the tax year 2020-2021. Filing Requirements & How to eFile.! You must file a Form 1099-NEC form for non-employee compensation ifNorth Carolina, Ohio, Texas, Vermont, Virginia, Department of the ... THE NORTH CAROLINA BOARD OF EXAMINERS FOR ENGINEERS AND SURVEYORSmailed to the Board office (address on cover sheet) or emailed to the Director of Firm ...5 pages

THE NORTH CAROLINA BOARD OF EXAMINERS FOR ENGINEERS AND SURVEYORSmailed to the Board office (address on cover sheet) or emailed to the Director of Firm ... A business will only use a Form 1099-NEC if it is reporting nonemployee compensation. If a business needs to report other income, such as rents, ... Each new employee must complete and submit to their employer a North Carolina Form NC-4, Employee's Withholding Allowance Certificate (or ... HOW TO OBTAIN A NORTH CAROLINA. BAIL BOND LICENSE CHECKLIST. 1. Licensing requirements and reasons for which an application may be denied are provided. As new laws are enacted or existing laws are changed, the League will prepare and distribute supplemental pages. S. Ellis Hankins. Executive Director. N.C. ...